By: Daphne Lye, CFP

Senior Lead, Solutions, Research & Investment, MoneyOwl

The recent restructuring of Integrated Shield Plan (IP) riders has prompted a lot of commentary about savings and affordability.

Much of it has focused on the headline figure: lower rider premiums. But to make sound decisions about health insurance, consumers and advisers alike need to understand the full picture.

Why rider premiums have come down, and what that actually means

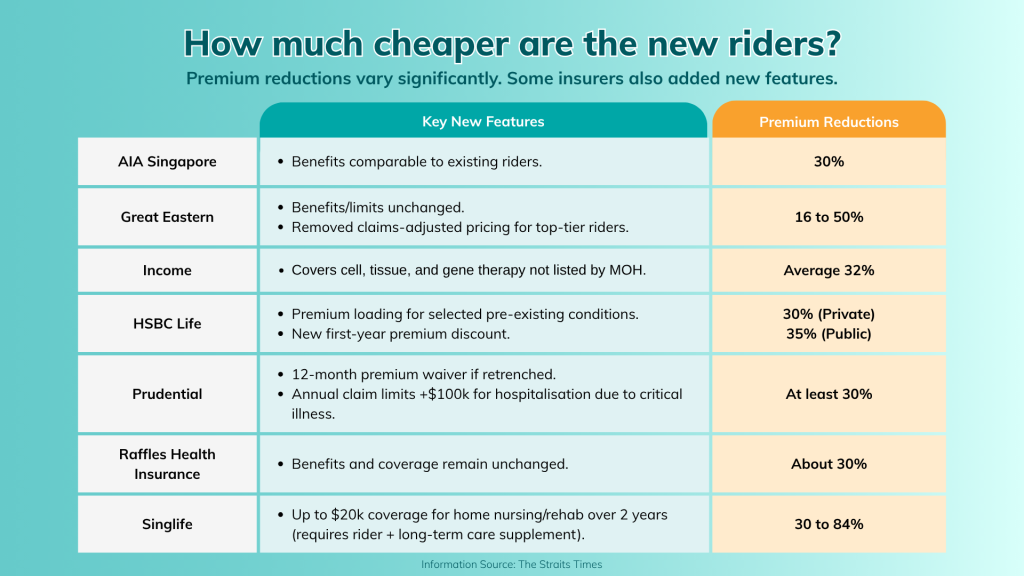

The degree of premium reduction varies considerably across insurers, which is accompanied by a material reduction in coverage.

Since 1 April 2026, new riders are no longer permitted to cover the initial deductible on a hospital bill, which typically ranges from S$1,500 to S$3,500 depending on ward class. The cap on what a policyholder must pay out of pocket has also been raised from S$3,000 to S$6,000.

Lower premiums, in this case, correspond directly to lower protection.

The reason for these changes is structural: old IP riders covered almost everything, making healthcare feel effectively free at the point of consumption. That created a cycle of over-consumption that drove up costs for everyone in the system.

The base premium increase for IPs adds another layer

Alongside the reduction in new rider premiums, five out of seven insurers have raised their base IP premiums. Only AIA and Great Eastern did not increase base plan premiums in this round.

Reasons cited for the premium increase include:

- Rising healthcare costs

- Increasing prices of advanced treatments and drugs

- Higher healthcare utilisation

- The need to ensure products remain financially sustainable.

These are structural, persistent pressures, not one-off events.

Growth in private healthcare insurance claims is projected to reach 16.9% in 2026[1], which gives some context to why these adjustments continue year after year.

But what matters for consumers is the combined effect. A policyholder’s total annual outlay is the sum of the base IP premium and the rider premium.

Even where new rider premiums are lower, an increase in the base plan can dilute or offset those savings.

At present, we observe that rider savings are meaningfully larger than the base premium increases, particularly at younger ages.

But this balance should not be assumed to hold indefinitely, especially given that both components are subject to ongoing upward pressure.

For certain age groups, the net result may be a squeeze on two fronts: higher annual premiums at the base level, and higher potential out-of-pocket costs at the point of hospitalisation.

How much can you save over the long term with the new riders?

Estimates of lifetime savings exceeding S$100,000 from switching to new riders have been cited.

Keep in mind that these projections are based on current premium rates and, importantly, do not account for future adjustments.

Given the persistence of medical inflation and annual health insurance premium reviews, it is reasonable to expect that both base IP and rider premiums will continue to rise.

The actual long-term savings from switching are therefore likely to be lower than these initial figures suggest.

There is a second source of uncertainty that is harder to quantify: the future cost of higher out-of-pocket expenses under reduced coverage.

Medical inflation does not only affect premiums, but also the cost of every hospitalisation and specialist visit. How quickly those costs grow depends on an individual’s healthcare usage, which is difficult to predict.

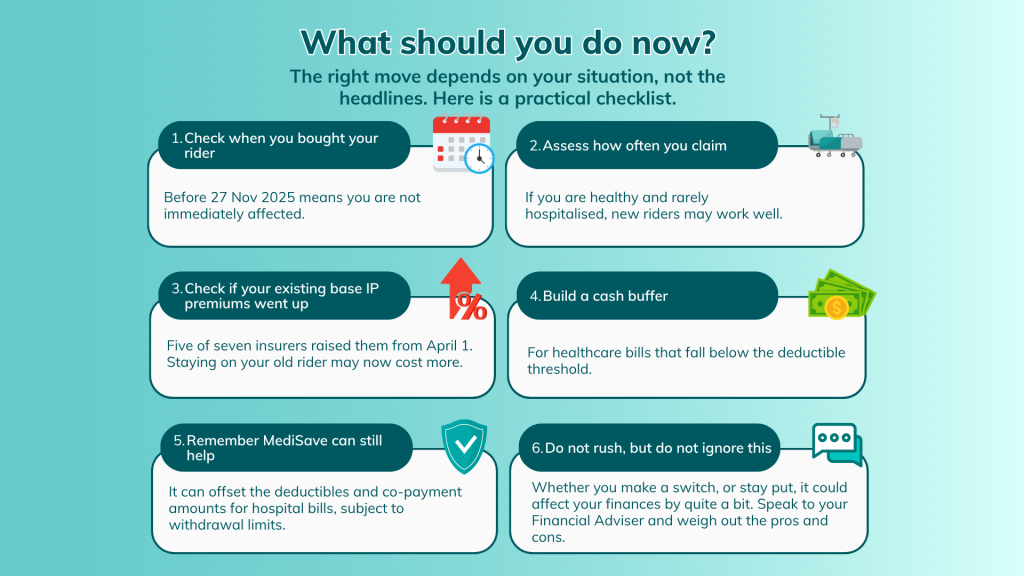

A more practical framework than projecting lifetime figures is to assess affordability and risk tolerance at the present.

- Can you comfortably manage the new rider premium? And if hospitalised, can you absorb the higher co-payment without material financial strain?

- If yes to both, switching may make sense for you today.

- If you can equally afford to maintain the existing rider, there is little urgency to change.

The structural reality: policyholders have limited mobility

One aspect of this conversation that deserves more attention is the limited ability of policyholders to respond to premium changes by simply moving to another insurer. Unlike most consumer products, health insurance becomes harder to switch as you age.

Medical conditions, sometimes unknown even to the policyholder, may be classified as pre-existing under a new insurer’s terms, creating gaps in coverage at precisely the point when protection matters most.

This structural reality places a genuine obligation on insurers to exercise fairness in how they set and adjust premiums.

The IP is often the first policy a person purchases for themselves or their child.

It is the entry point into an insurer’s customer base, and it underpins a commercial relationship that extends across many products over many years.

Decisions to adjust premiums by insurers should reflect the whole of that relationship, not only the profitability of the IP business line in isolation.

Practical guidance for policyholders considering a change

A growing number of consumers are likely to consider downgrading their plans or riders.

One insurer survey indicated that 81% of their customers intended to make changes to their insurance portfolios in light of the new rider structure.

Affordability pressures, particularly for retirees and those on fixed incomes, are real and will intensify as premiums continue to rise.

The right decision depends on your personal situation.

- For those who are generally healthy and rarely hospitalised: lower premiums under the new rider structure translate into genuine annual savings, with out-of-pocket costs only arising on the relatively infrequent occasions hospitalisation is required.

- For those with pre-existing conditions, regular specialist visits, or a strong preference for comprehensive protection: staying with the existing rider may be the more financially prudent choice, particularly if the premiums remain manageable as a proportion of your income.

If you are thinking about switching your Integrated Plan (IP) or rider, one important rule of thumb is to stay with your current insurer rather than moving to a new one. Here’s why.

First, even if you feel perfectly healthy, you may have unknowingly developed a health condition since you first took out your policy. If you switch insurers, that condition, however minor or undetected, could be flagged as a pre-existing condition by the new insurer. This can result in exclusions, meaning the new policy will not cover treatments related to that condition. For example, a growth can be asymptomatic until a diagnostic test, but its size may cause it to be regarded as a pre-existing condition by the new insurer in any case.

Second, new policies typically come with waiting periods (usually 30 to 90 days) during which certain claims cannot be made. If you require medical treatment shortly after switching, you may find yourself unprotected at exactly the wrong moment.

Third, a lower premium is not always the bargain it appears to be. IP premiums are not guaranteed, and insurers can and do raise them over time. A plan that looks attractively priced today may become significantly more expensive in a few years – by which point switching again carries all the same risks outlined above.

With all of this information – what should you do now?

MoneyOwl’s position

Our overarching recommendation is this: buy the highest level of IP and rider coverage you need and can genuinely afford while you are healthy.

You can always downgrade your ward class later as circumstances change.

What you cannot always do is upgrade or switch once your health profile has shifted.

IP and rider premiums are not guaranteed, and the rates you see today will not stay fixed. Plan accordingly, avoid overpaying, and make decisions based on your own situation rather than the headlines.

The changes to IP riders and premiums are significant, and they will continue to evolve.

Navigating them well requires looking beyond the headline numbers, understanding what has actually changed in terms of coverage, and grounding every decision in your individual health profile, financial position, and long-term planning.

Note: MAS recommends spending no more than 15% of income on insurance protection overall, of which health insurance is just one component.

If you require assistance from an adviser, we can refer you to our insurance partner via this link:

[1] Source: 2026 Global Medical Trends report by WTW (published Nov 2026)

Disclaimer:

Whilst we have taken all reasonable care to ensure that the information contained in this article is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or completeness. You should not act on it without first independently verifying its contents. Any opinion or estimate contained in this presentation is subject to change without notice. Buying insurance is a long-term commitment and should be bought according to your needs, and products’ suitability. The information contained herein does not have any regard to the specific financial objective(s), financial situation or the particular needs of any person. It is advisable to seek advice from a qualified financial adviser to assess your needs and understand the features, risks, and costs of any financial product before making a decision.

This publication has not been reviewed by the Monetary Authority of Singapore