By Ernest Tham, Financial Planning Solutions Specialist

Singapore Department of Statistics (SingStat) released its Complete Life Tables 2024-2025 on 3 June 2026.

Most headlines will focus on life expectancy at birth, now 83.9 years. That number is worth knowing. But it is not the number that should be shaping your retirement plan.

Here is the one that should.

By the time someone reaches 65, they have already survived infant mortality, accidents, and premature illness.

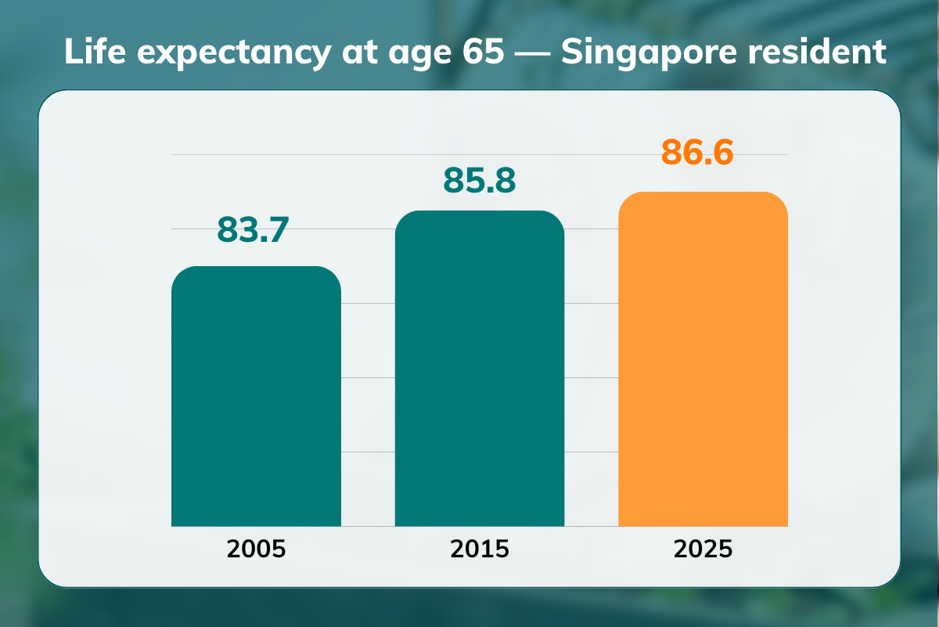

Hence, for a 65-year-old, the relevant benchmark is not the birth life expectancy figure, but the conditional figure: 86.6 years for a 65-year-old today, or 84.9 years for males and 88.1 for females.

In 2005, a 65-year-old Singapore resident could expect to live to 83.7. In 2015, that figure had risen to 85.8. In 2025, it is now 86.6.

That’s nearly three additional years of expected life gained at age 65, in two decades.

This is a persistent trend that has moved in one direction for as long as the Complete Life Tables have been published. It has direct consequences for how every Singaporean should think about retirement income.

Beyond the average

The life expectancy figures above are averages. They tell you where the middle of the population lands, but it is more important to realise that half may land well beyond it.

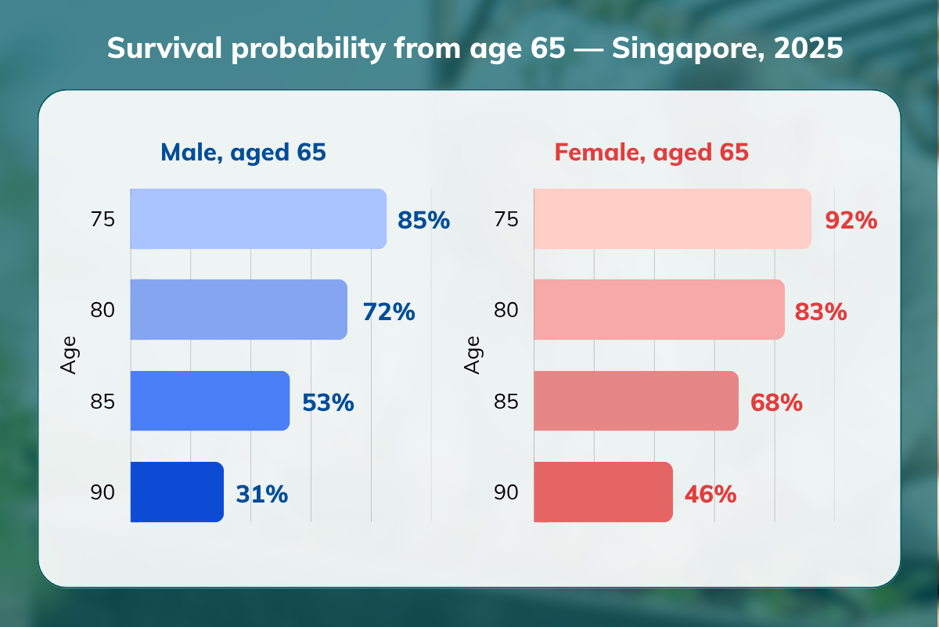

Using the full life tables published by SingStat, we can work out the probability that a 65-year-old today survives to each subsequent age.

For a 65-year-old male in 2025:

- 85% chance of reaching 75

- 72% chance of reaching 80

- 53% chance of reaching 85

- 31% chance of reaching 90

For a 65-year-old female in 2025:

- 92% chance of reaching 75

- 83% chance of reaching 80

- 68% chance of reaching 85

- 46% chance of reaching 90

More than half of all 65-year-old men will reach 85. Nearly half of all 65-year-old women will reach 90. For a couple where both are 65 today, there is a 62% probability that at least one of them will reach 90, and a 31% probability that at least one will reach 95.

The trend behind the numbers

What makes this a planning concern rather than just a statistical observation is how consistently these survival probabilities have shifted over time.

Each decade, the survival curve shifts further out. Future gains may be more gradual as Singapore approaches the upper limits of what healthcare and lifestyle improvements can achieve.

The prudent approach is to plan beyond the current average, not to it.

What this means for retirement planning

The specific risk that rising longevity creates is longevity risk: the risk of outliving your money. The longer you live, the more years your income needs to cover. What you need is income that does not run out, regardless of how long you live.

CPF LIFE was designed for precisely this.

- It is an annuity, or insurance policy, that pays for as long as you live, with no upper age limit and no dependency on market returns.

- It is backed by the AAA-rated Singapore Government, with no additional fees or charges, and pools the savings nationally. This makes CPF LIFE different from market-based drawdown portfolios, including portfolios held through investment-linked policies.

A drawdown pool, however well-invested, can be depleted because of market risk and sequence of returns risk. [1]

As for comparable commercial retirement income or annuity-like insurance products, it has been well established that CPF LIFE is the superior annuity in terms of stable payout quantum and length of payout you get for each dollar of premium.

CPF LIFE is not meant to be the complete retirement solution, but it is the most important part of it. It anchors the safe retirement income floor that no market-based product can replicate. At a minimum, aim for the Full Retirement Sum (FRS) of $220,400 in 2026, as it provides a modest payout of $1,780 per month [2] 10 years later from age 65.

Any other income streams should be built around that foundation, not in place of it.

The goal of those other streams is straightforward – to supplement CPF LIFE for lifestyle spending as needed, not to chase returns or leave a legacy at the expense of income security.

Seeing the full picture

Understanding how these layers fit together, when CPF LIFE kicks in, and how your drawdown portfolio contributes across a retirement that may last longer than you expect, is not always straightforward.

Furthermore, an investment portfolio drawn down too aggressively in the early years of retirement may deplete the portfolio earlier than planned.

MoneyOwl’s Retirement Income Builder (launching soon) helps you visualise your retirement income streams over time, with CPF LIFE as the foundation. See how your different sources of income work together and whether your plan can support the lifestyle you want throughout retirement.

Sign up for our newsletter to be notified when the RIB Tool launches: https://bit.ly/moml

Data source: Department of Statistics Singapore, Complete Life Tables for Singapore Resident Population 2024-2025 (published 3 June 2026). Survival probability figures are derived from the lx column of the complete life tables for 2005, 2015, and 2025 (preliminary). All figures refer to Singapore residents (citizens and permanent residents). Joint couple survival probabilities are calculated from male and female conditional survival probabilities independently, assuming both partners are aged 65.

Disclaimer: While every reasonable care is taken to ensure the accuracy of information provided, no responsibility can be accepted for any loss or inconvenience caused by any error or omission. The information and opinions expressed herein are made in good faith and are based on sources believed to be reliable but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Neither the creator of the article nor MoneyOwl shall be liable for any loss or expense whatsoever relating to investment decisions made by the reader.

This article has not been reviewed by the Monetary Authority of Singapore.

[1] Sequence of returns risk is the danger that poor market returns early in retirement can permanently damage a drawdown portfolio even if markets later recover. A retiree forced to sell investments during a downturn locks in losses before any recovery can take hold.

[2] Standard Plan for Males