Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Let’s take a look at the mythical crystal ball and wonder, what will 2023 bring? As we know, 2020 and 2021 went by in a blur because of the pandemic, while exciting happenings marked 2022 with headline inflation rates, returning to the office, resuming of live events, an exhilarating World Cup, and life finally returning to a norm with masks off in Singapore.

As we approach the year’s end, which brings about introspection and reflection, it’s timely to take stock and celebrate the breakthroughs, if not small wins, achieved this year and decide on your course for 2023. Setting financial goals can seem daunting, but it doesn’t have to be.

Here is a quick guide on how you can make your financial bucket list so that you’re well on your way to achieving those dreams for the year ahead:

#1 Save for Emergencies

2023 may be the year for revenge travel, but before you jump on the bandwagon and book that air ticket, think again. With economic uncertainty on the horizon, cash may well become king. Emergencies come in all shapes and sizes — from major ones like a sudden loss of income due to job cuts or an appliance breaking down that needs urgent replacement. Yet, according to the OCBC Financial Wellness Index 2022, 47% of Singaporeans don’t have six months of salary set aside to tide them through a crisis, which can lead to financial strain if an emergency does happen.

#2 Optimise your Finances for a High Interest Rate Environment

Interest rates may continue to stay high in 2023, so try to reduce your debt, especially high-interest debt. High-interest debt such as your mortgage and credit card debt can be more costly than other types of debt because the longer it takes to pay off, the more money you end up spending in total.

#3 Reduce Taxable Income by Understanding the Tax Reliefs Available

As you plan for 2023, reducing your taxable income is an excellent place to start. There are several different ways of doing this:

Save for Retirement

For dollar-to-dollar tax relief, you can top up your CPF – Special or Medisave accounts to a maximum of $8,000. For additional tax relief, you can make an additional $8,000 top-up to your parents’ Special / Retirement or MediSave accounts.

The Supplementary Retirement Scheme (SRS) also provides dollar-to-dollar tax relief, with an annual contribution cap of $15,300 for Singapore Citizens and Permanent Residents and $35,700 for foreigners. By contributing and investing your SRS Funds, you can multiply your retirement savings, save on taxes and beat inflation. Check out our handy visual guide on why you should invest your SRS Funds with MoneyOwl.

Make use of Family Reliefs/Rebates

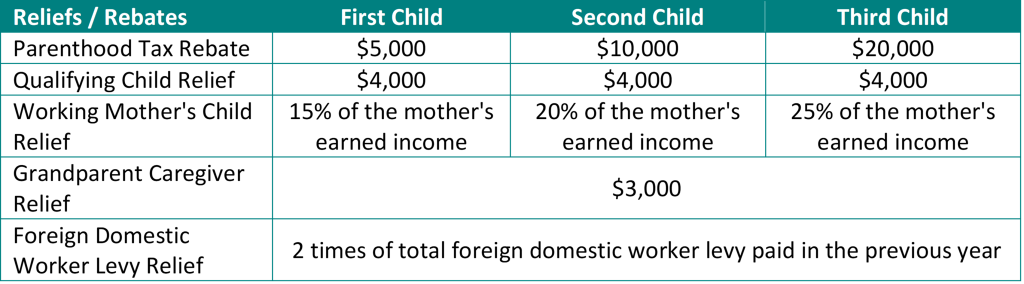

Did you know about the myriad of reliefs available to families? For new parents, check out the set of reliefs and rebates that you’re entitled to when you welcome your bundle of joy. It includes a parenthood tax rebate of $5,000 for your first child, $4,000 in tax relief for each qualifying child, 15 to 25% of your income for working mums, and extends to caregivers such as the Grandparent Caregiver Relief and a Foreign Domestic Worker Levy Relief when you engage domestic help. It truly takes a village to raise a child, and any financial support goes a long way!

For those with a dependant spouse earning less than an annual income of $4,000, you may also be eligible to claim a Spouse Relief of $2,000.

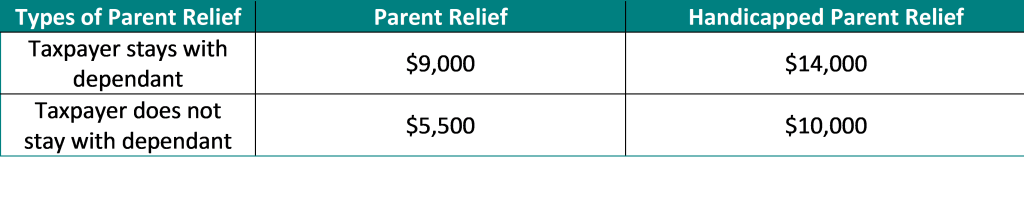

Adult children that choose to stay with their parents/grandparents/parents-in-law/grandparents-in-law may also claim $9,000 per dependant for up to 2 dependents. The caveat is that the dependant has to earn an annual income of less than $4,000 to be eligible. Siblings working to support their loved ones jointly may also choose to share the Parent Relief by agreeing on the share of their individual claim amounts and declaring it to IRAS.

Donate

Tis’ the season to do good, and no good deed ever goes wasted. Although 2022 may be coming to an end, you can always get started on your charitable deeds for 2023. For every $1 that you donate to an approved Institution of Public Character, you get $2.50 back in tax savings. Donations must be completed within the year of assessment to be computed for the year’s taxable income.

While deciding which charity to contribute to is primarily a personal choice, you can narrow it down to your pet cause, whether it’s for the elderly, cancer awareness, special needs, animals, children or the environment. We recommend you hit search here to get started!

Enhance Your Skills

In the spirit of lifelong learning, you can enjoy tax relief if you take a course that enhances your skillsets in your chosen industry, vocation or trade. The reliefs apply to course fees and include registration, exam fees and professional certification fees. You can claim a maximum of $5,500 per year in course fees.

#4 Invest For The Long-Term

Investing your money in a diversified portfolio of low-cost funds is the best way to invest. This means you don’t buy individual stocks, bonds, or commodities. It’s tempting to think you can beat the market by selecting individual stocks and bonds. However, by actively trading, you may be potentially missing out on the market’s expected return— not to mention being stressed out and constantly worrying whether you should react to any market news.

When economist Michael Jensen published his paper in 1968 demonstrating that active stock pickers could not add consistent value, other academics quickly confirmed his findings. The theory still holds up after more than five decades and 50 years of data. Of course, some stock pickers are successful, but we don’t know if this is due to skill or luck.

#5 Make A Financial Bucket List And Get Started Today!

To help you get started, make a list of your financial goals. What do you want to accomplish by 2023? For example, do you want to increase your savings and emergency fund, pay off debt, or save up to buy a home? Write down what’s important to you and then prioritise those goals so that they’re easy for you to manage. Every little bit makes a difference, and it’ll eventually help you reach your goals in the long run.

Disclaimer:

While every reasonable care is taken to ensure the accuracy of information provided, no responsibility can be accepted for any loss or inconvenience caused by any error or omission. The information and opinions expressed herein are made in good faith and are based on sources believed to be reliable but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Expressions of opinions or estimates should neither be relied upon nor used in any way as indication of the future performance of any financial products, as prices of assets and currencies may go down as well as up. All investments carry risk. Past performance should not be taken as indication of future performance. The author and publisher shall have no liability for any loss or expense whatsoever relating to investment decisions made by the reader.