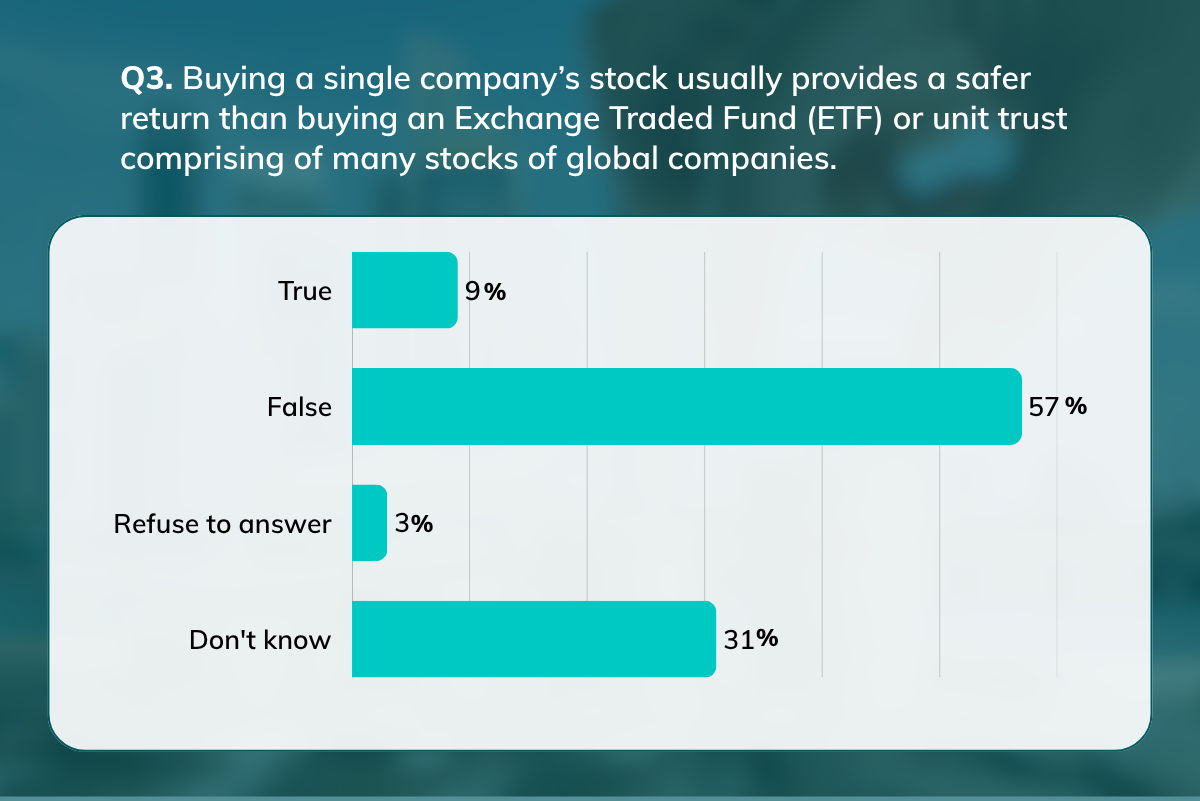

Picture two ways to invest $10,000. The first goes entirely into a single company’s shares; the second spreads across hundreds of companies through an exchange-traded fund (ETF). Which is safer? If you chose the single stock, you are not alone, but the answer is wrong.

According to the MoneyOwl Financial Literacy Assessment 2026, investment risk is the one money concept that trips up most Singaporeans, even as half the population scores well on the fundamentals.

Across the three core questions that define financial literacy, 51% of Singaporeans answered every one correctly. That is a respectable result – but it leaves nearly half of us short, and the gaps are unevenly spread.

How financial literacy is measured

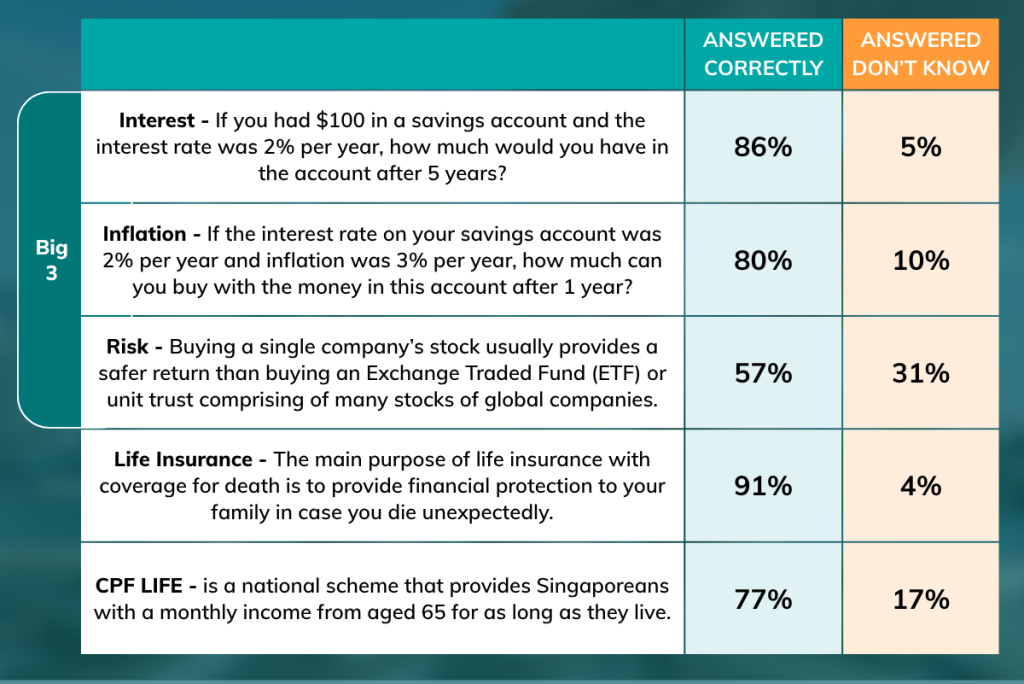

The assessment is built on the “Big Three” – a set of questions on interest, inflation and risk first developed by Professor Annamaria Lusardi and Professor Olivia Mitchell1 used to benchmark financial knowledge around the world. It has been shown that its concise design captures core knowledge as well as longer assessments and accurately predicts critical behaviour such as retirement savings and debt management across different demographic groups.2

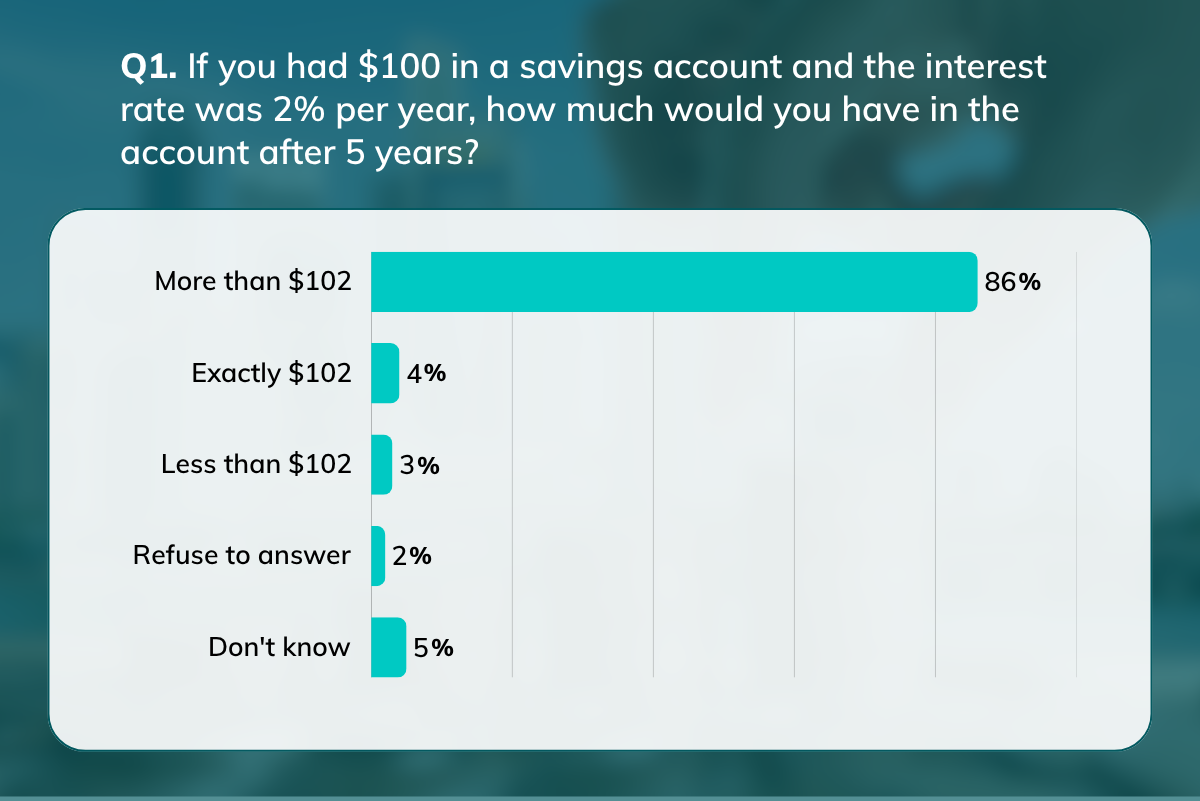

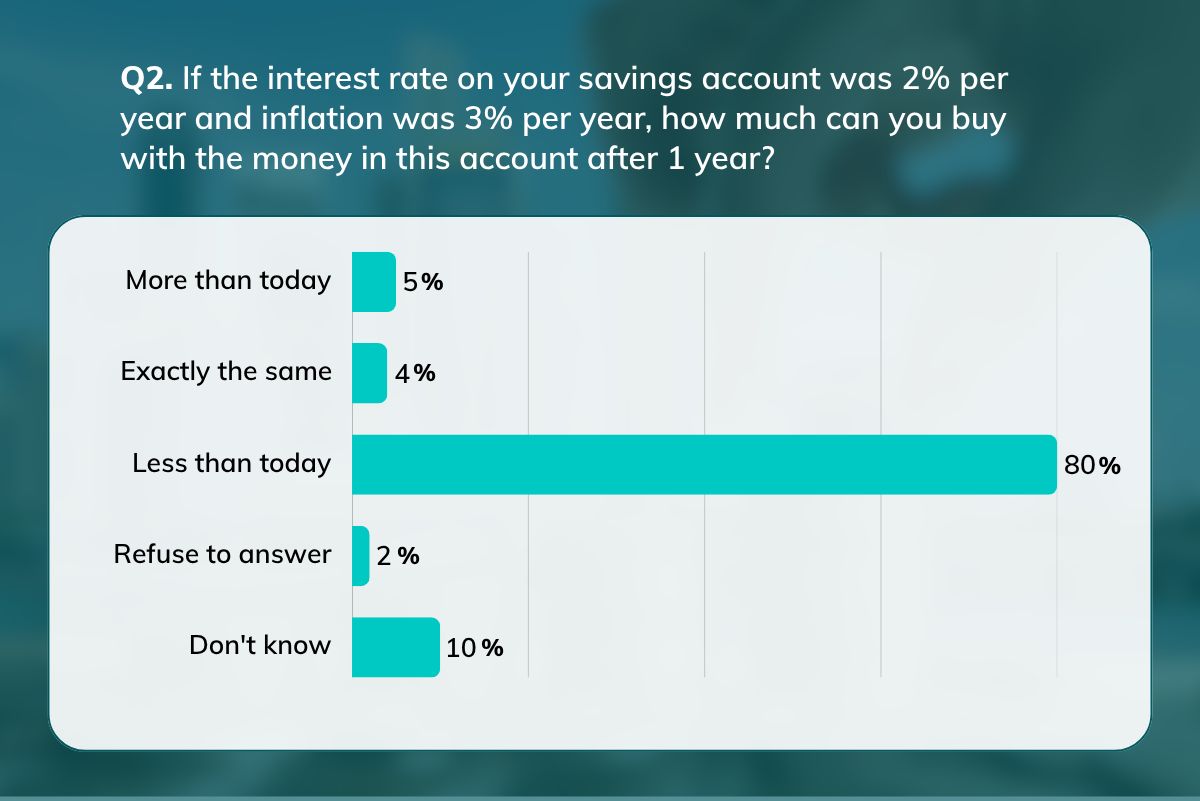

Interest tests whether you understand how savings grow over time. Inflation tests whether you grasp how rising prices erode what your money can buy. Risk tests whether you know that spreading your money across many investments is safer than betting on one.

To these, MoneyOwl’s study adds two questions tailored to Singapore: one on life insurance, and one on CPF LIFE, the national scheme that pays a monthly income for life in retirement. Someone is considered “financially literate” only if they answer every question correctly. By these standards, 51% pass on the Big Three, and 41% pass across all five questions.

Topic by topic: where understanding holds, and where it breaks

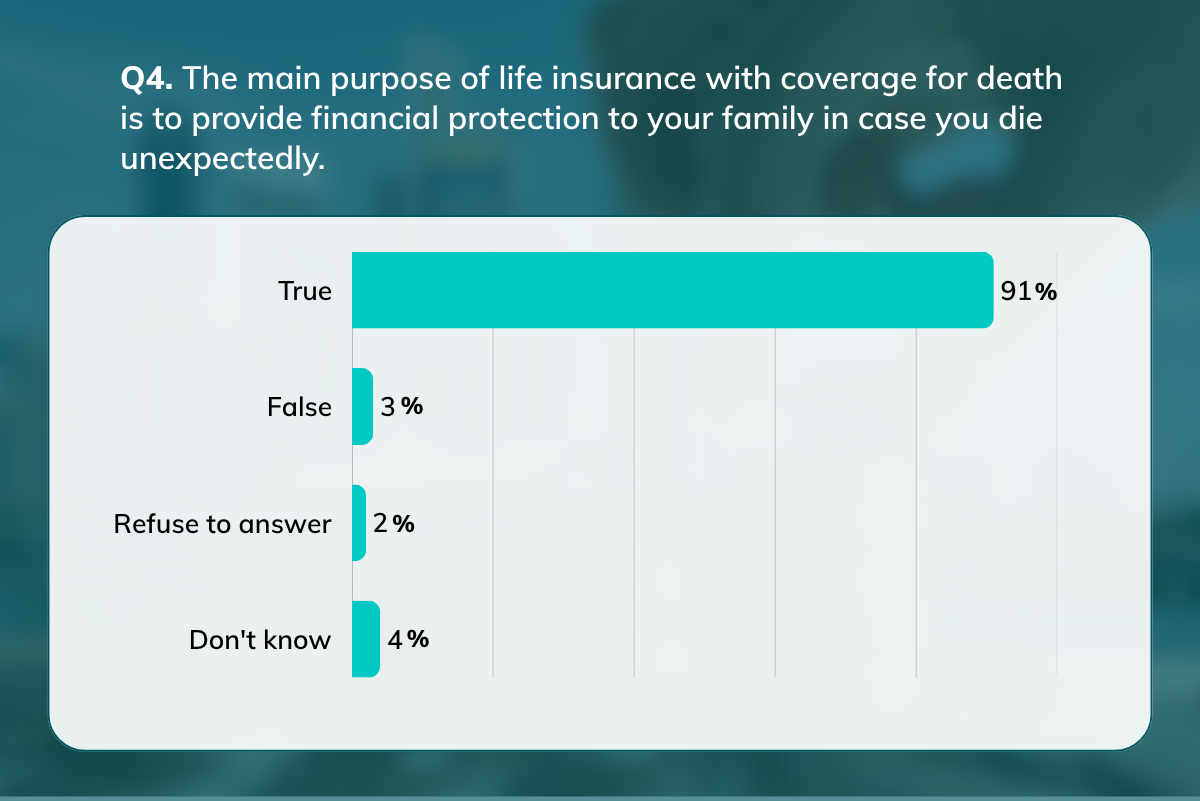

Ranked by the share who answered correctly, life insurance is best understood – 91% knew its core purpose is to provide financial protection for a family if the policyholder dies.

This is followed by interest (86%) and inflation (80%). Roughly eight in ten answered these questions correctly, showing that most people understand how savings accumulate and how inflation quietly chips away at spending power.

The picture changes sharply on investment risk. Only 57% recognised that a single company’s stock is generally riskier than a diversified fund holding many companies. This is the principle of diversification: by spreading money across many investments, a loss in any one is cushioned by the others, so the overall ride is smoother. It is one of the most powerful ideas in personal finance – and the one Singaporeans are least likely to grasp.

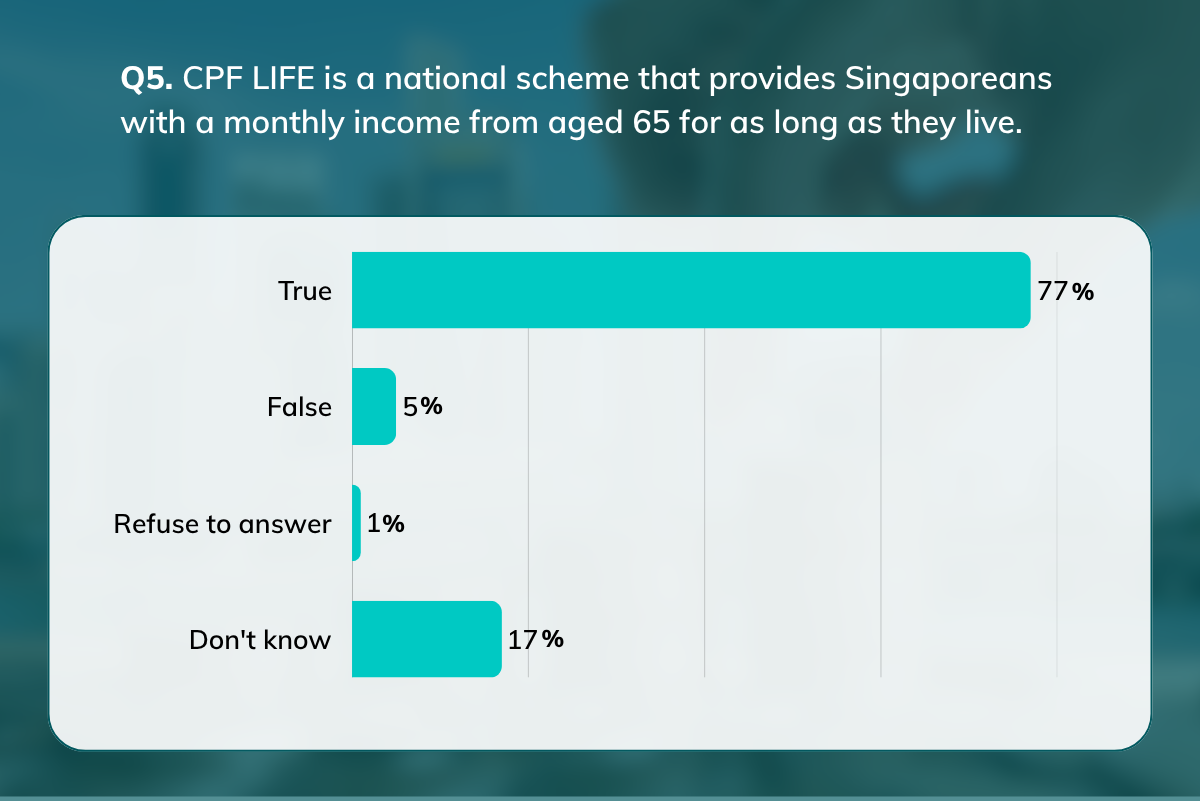

CPF LIFE is in a quieter blind spot. Although it underpins retirement income for most Singaporeans, nearly a quarter either answered incorrectly or were unsure (77% correct, 17% “don’t know”) – a notable gap for a scheme that touches almost everyone in later life.

A second signal is just as telling: how often people simply said “don’t know.” Across the five questions, 43% chose “don’t know” at least once, and risk drew by far the most uncertainty, with 31% admitting they were unsure. Taken together, risk is not only the topic Singaporeans get wrong most often — it is also the one they feel least confident about.

The literacy divide: who knows what

The headline numbers hide wide differences between groups. The sharpest divide is income: Singaporeans earning above the median household income outscored everyone else on interest, inflation and risk. Education tracks closely behind – degree holders led on four of the five topics, as does housing, with private property residents scoring higher (a pattern that largely mirrors income).

Age shapes knowledge in a different way. Those aged 55 and above scored the best on CPF LIFE and life insurance, the topics closest to their stage of life, while the youngest group (15 to 24) were the most likely to answer “don’t know.” There were also differences by gender – men outscored women on inflation and risk. One myth worth busting: employment status made no significant difference at all.

The costs of not understanding investment risk

Misunderstanding risk has real consequences. People who do not grasp diversification are more likely to pour money into a single “hot” stock, to sit out of investing altogether for fear of losing it all, or to misjudge how much risk they are taking with their investment.

Each of these can quietly cost years of long-term growth. And because uncertainty about CPF LIFE feeds straight into how confident people feel about retirement, closing these two gaps – investment risk and CPF LIFE – would significantly improve the general financial well-being and confidence of Singaporeans.

What you can do

Wherever you sit on the literacy scale, a few habits go a long way:

- Understand investment risks and diversification before you buy. If you are tempted by a single stock, ask how that bet would look spread over the long-term across a low-cost diversified fund instead.

- Respect inflation. Money sitting in a low-interest account lose real value over time – factor rising prices into your savings plan.

- Know your CPF basics. Check your CPF balances, how they grow, consider whether to make top-ups to grow your retirement nest egg, when lifelong monthly payouts begin, and what they will mean for your retirement income.

- If you answered “don’t know” to any of the questions, take it as a sign to read and find out more. The topics you are least sure about are the ones worth ten minutes of reading.

Disclaimer: This material is provided for general information only and does not constitute financial advice, a recommendation, or an offer to buy or sell any financial product. While reasonable care has been taken to ensure accuracy, no representation or warranty is made as to the completeness or reliability of the information, and no responsibility can be accepted for any loss or inconvenience caused by any error or omission. Any opinions or estimates are subject to change and should not be relied upon as an indication of future performance. The value of investments may rise or fall, and insurance benefits are subject to policy terms, conditions, and exclusions. You should consider your own financial objectives, financial situation, and needs before making any financial decision. It is advisable to seek advice from a qualified financial adviser to assess your needs and understand the features, risks, and costs of any financial product before making a decision.

This publication has not been reviewed by the Monetary Authority of Singapore

About the study

This study, the MoneyOwl Financial Literacy Assessment 2026, is commissioned by MoneyOwl, and is conducted by HappyDot.sg, an online survey platform owned by RySense. The sample size is 1,049 Singapore Citizens and Permanent Residents aged 15 and above, conducted between 20 and 27 April 2026. Quotas for age, gender and race were set to match Department of Statistics population data, and results are weighted to be nationally representative.

Financial literacy is assessed using the “Big Three” framework (Lusardi & Mitchell, 2011) covering interest, inflation and risk, plus two supplementary questions on life insurance and CPF LIFE. Figures are rounded and may not sum to exactly 100%.

Annex: Questions and Answers