Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Why we should understand more about the purpose of insurance and the importance of insuring ourselves sufficiently.

It strikes me hard that the majority people of the people whom I know, are paying a significant amount from their hard-earned income for their insurance but yet, are still severely underinsured.

Amount of Premiums We Pay =/= Enough Insurance Coverage for Ourselves

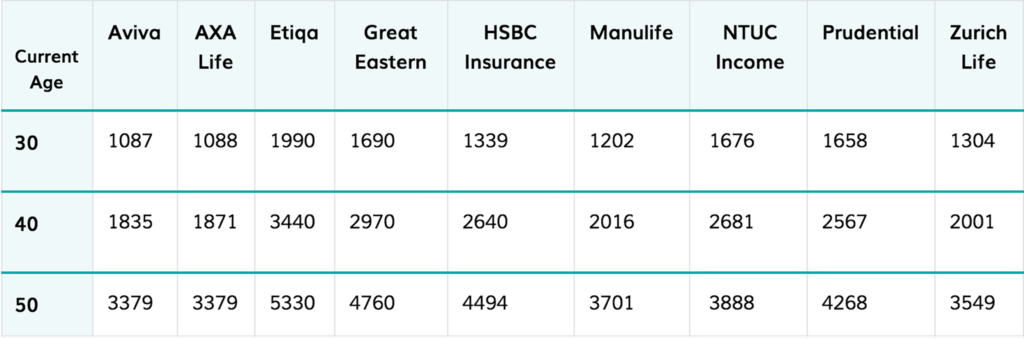

We consider the following example of a Male, Non-Smoker

- Policy coverage till 65 years old (when children are independent)

- S$1million Death and Total Permanent Disability Coverage

This is the annual premium from various insurers in Singapore (S$):This is the annual premium from various insurers in Singapore (S$):

*With information from MoneyOwl and comparefirst. Figures are compiled on 14th September 2015 and includes existing promotions and discounts which are in the knowledge of.

**You are advised to approach a financial advisor for his/her opinion on the features, details and current quotes of the products or if you are considering to purchase, if you should surrender or restructure your existing insurance policies.

You may wish to compare what you are currently paying for your insurance policy against what is currently offered by the different insurers.

For us to be covered by life insurance for our entire life, it is very expensive with whole life insurance. We will find that we are not able to sufficiently insure ourselves if we use whole life insurance. For a 30 year-old male, $500,000 whole life coverage could cost S$7,000 annually* to be paid annually for 49 years!

Are you overpaying for the amount of insurance coverage you have? Are you sufficiently insured for your loved ones?

Purchasing term insurance is the only way to provide sufficient coverage. Read this write up by Christopher Tan to understand about the Case of Term Life Insurance.

The Purpose of Insurance

The purpose of insurance is to transfer our risk of a loss to another party in exchange for money. It is important that we adequately transfer our risk (sufficiently insure ourselves) and keep the cost that we are paying for insurance low. However, there are many misconceptions when it comes to insurance and these are the common ones that I have come across:

- I need life insurance coverage for my whole life

Our financial obligations tend to decrease as we age due to the fact that, as our dependents grow older, they are dependent on us for a fewer number of years. We should have also built up sufficient assets such that if an unexpected event were to occur, we would have sufficient assets to leave behind for our dependents to live on. There comes a point of time in our life when we do not need any life insurance coverage to provide for our loved ones as they are no longer dependent on us financially.

- Whole life insurance is always better because I may only have to pay for a limited number of years and I can save as well

For insurance companies to craft a policy where it is possible for one to pay only for a limited number of years, it means that a lot more has to be paid for the initial years to compensate for the other remaining years. If we are using whole life insurance for savings, for the low liquidity and returns it provides, we could use many other investment tools which allow us the flexibility to draw our money when we need to without any penalties and possibly achieve greater returns with them.

- More coverage is always better

This only holds true if we do not have other financial commitments. Accumulating enough funds to retire is not easy to achieve. In a study done by AIA in 2014, 55% of Singaporean respondents were worried they would not be able to save enough as compared to a regional average of 44%. More worryingly, 35% of Singaporean respondents ranked saving for retirement as the most difficult goal to achieve in life. If we decide to spend more on insurance, something else has to be forgone. This could mean prolonging our working years and pushing back our retirement age.

I hope that more of us will understand and spread the word about the purpose of insurance and the importance of insuring ourselves sufficiently. We do not have to overpay when we purchase the right type of insurance and it does not cost us an arm and a leg for us to be adequately insured for our loved ones.I hope that more of us will understand and spread the word about the purpose of insurance and the importance of insuring ourselves sufficiently. We do not have to overpay when we purchase the right type of insurance and it does not cost us an arm and a leg for us to be adequately insured for our loved ones.

Announcement: With effect from 1 June 2022, MoneyOwl is a 100% NTUC Enterprise (NE)-owned company.