Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Find out strategies that many bond managers have engaged to generate higher returns which is known as riding the yield curve.

What is a bond?

Bond is a debt security or I.O.U. issued by a government or corporation to raise funds. By investing in a bond, investors (aka. bondholders) are essentially lending money to the bond issuers. If you take up a bank loan today, you know that you will need to make regular interest payments to the bank and repay the principal according to the agreed payment schedule. These interest payments then become a steady stream of income to the bank. A similar structure applies to bonds. Investors who invest in bonds expect to receive a stream of interest payments, known as coupons, together with the repayment of their principal when it matures.

Bonds provide a predictable stream of income and play an important role in diversifying an investment portfolio as their prices are less volatile than equities. However, investing in a bond is not just about holding it till maturity.

This is because there are three sources of returns for bonds:

- Yield (i.e. coupon rate)

- Bond price changes as it moves down the yield curve

- Future changes in the yield curve

Both (1) and (2) are known and observable information that can be derived from current yield curves, while (3) requires forecasting about the unknown.

At MoneyOwl, we do not forecast. We believe in the collective wisdom of the millions of investors in the world such that bond prices already reflect all publicly available information in the market. In addition, there is a lack of evidence supporting that forecasting can deliver consistently higher returns. So, without depending on (3) and in current market conditions where some bonds give very low or even negative yields, can we still earn from investing in bonds? The answer is yes.

In this article, we explain one of the strategies that many bond managers have engaged to generate higher returns which is known as riding the yield curve.

Rolling down the yield curve / Riding the yield curve strategy explained.

This strategy involves buying a bond and selling it before its maturity to realise the price appreciation, instead of holding the bonds until maturity. It is one of the most straightforward strategies that is built around two principles:

Principle 1: Investors demand higher coupons for holding longer-term bonds, creating an upward sloping yield curve.

Longer-term bonds are usually associated with greater risk and uncertainties. We won’t know what the future may hold, and the longer the time, the greater the uncertainty. Hence, investors would usually demand higher returns for holding a longer-term bond.

Principle 2: Bond investors, like any other rational investor, will seek the best risk-adjusted return available.

What this means is that all else being equal, we will prefer a bond that pays a higher coupon to one with a lower coupon rate. It is just like how we will look for the bank that offers the most attractive interest rates when we want to place a fixed deposit in bank for a year.

With both principles in mind, let’s dive further:

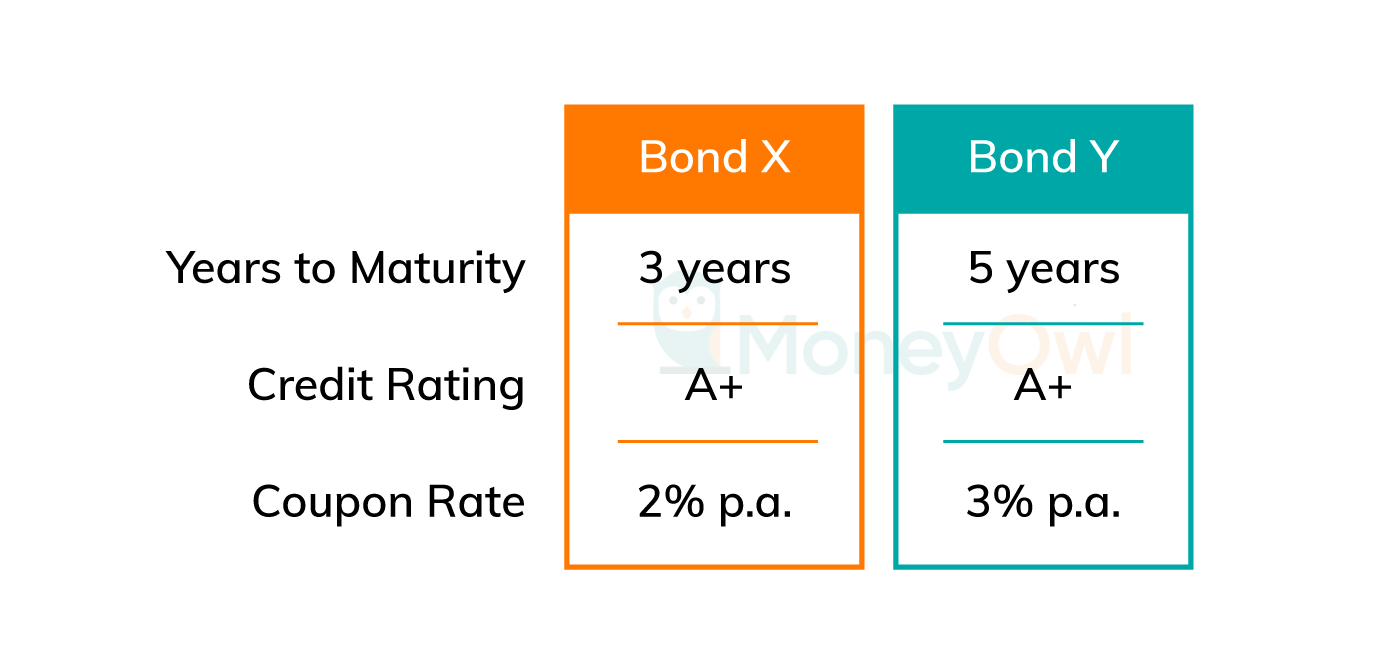

Suppose Amy wants to invest $100 for 3 years and there are 2 bonds to choose from. Bond X with 3 years to maturity, paying a coupon rate of 2% p.a. and Bond Y with 5 years to maturity, paying a coupon rate of 3% p.a.

Let’s take a look at 2 possible strategies which Amy could employ.

- Strategy #1: Buy the 3-year Bond X and hold it to maturity

- Strategy #2: Buy the 5-year Bond Y and sell it after 3 years

Strategy #1:

Her return is straight-forward. After 3 years, she will get back her principal amount of $100, plus the coupon payments of $6 ($2 x 3 years).

Which totals to $106 after 3 years.

Strategy #2:

After 3 years, Bond Y has a remaining maturity of 2 years, but its coupon rate is still 3% p.a. Referring to principle 1 and 2 above, a newly issued bond with a maturity of 2 years would have a lower coupon rate than Bond Y, therefore rational investors would be willing to pay a higher price for Bond Y. This is because it has a higher coupon with the equivalent number of years (2 years) remaining as the new bond.

Suppose Amy sells Bond Y at this time and receives $101 for it, in addition to the past coupon payments of $9 ($3 x 3 years).

She would have received a total of $110. That’s $4 more than the first strategy.

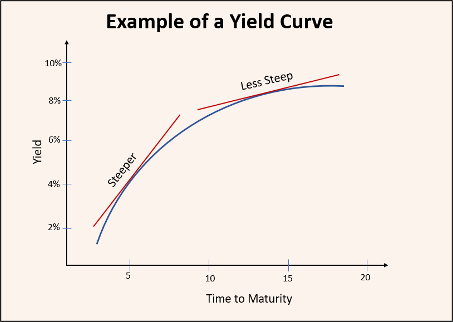

To sum up, the price of a bond increases as its maturity decreases because the coupon rate of other newly issued shorter-term bonds will be less attractive. The yield curve is not a straight line and is typically upward sloping and flattens out at longer maturities. Fund managers like Dimensional reap the greatest price appreciation by targeting the steepest part of the yield curve, i.e. where the change in yield, and hence the price, is the biggest over the shortest amount of time.

In the same way, it is possible to derive positive returns from bonds even in a negative interest rate environment. This is because the yield curve can still be upward sloping and steep even for negative-yielding bond markets such as Japan and parts of Europe.

For example, an investor may buy a negative-yielding 3-year bond and sell it after 1 year, similar to Amy’s first strategy above. Principle 1 would still apply, and the value of the 3-year bond would still be higher than a new 2-year bond, all else being equal. In other words, as long as the interest rates for shorter-term bonds are more negative than the longer-term ones, there is generally a possibility to make a positive return as you roll down the yield curve.

Role of Bonds in a Portfolio

We have spoken a lot about returns from bonds. However, in the context of constructing an investment portfolio, bond returns should not be the most important consideration.

At MoneyOwl, we use bond funds to play an important role in asset allocation by smoothing out the swings in the portfolio and diversifying the overall risk.

This is the reason we maintain high-quality investment-grade bonds in our funds rather than take risks with exposure to bonds in emerging markets. This helps our client to manage their emotions and stay invested, according to their risk profile.

In choosing the portfolio that best suits you, you should always consider your need, ability and willingness to take risk. Just like choosing a ride in the theme park, would you go for the most thrilling roller coaster ride, or rather hop on a scenic train with your favourite cartoon character?

If you are unsure, fret not, we can help you discover your risk profile in a few steps and recommend the most suitable portfolio for you.

The author and publisher shall have no liability for any loss or expense whatsoever relating to investment decisions made by the reader. This article should not be construed as an offer or solicitation for the subscription, purchase or sale of any fund.