Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

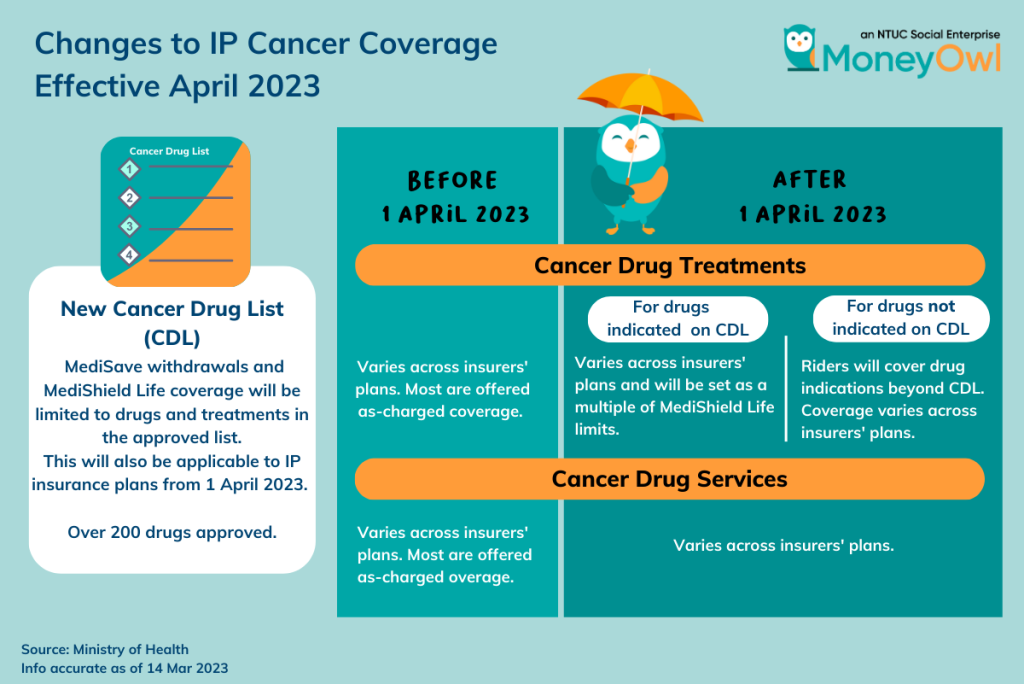

From 1 April 2023, the Cancer Drug List will come into effect for Integrated Shield Plans (IP), changing the way private insurers cover cancer treatment costs. For some of us, this change may impact our out-of-pocket expenses and overall care options should we be diagnosed with cancer down the road.

We compiled some commonly asked questions and posed them to our MoneyOwl Client Advisers to explain the changes in detail and what it means for those undergoing cancer treatment or considering critical illness coverage.

What is the Cancer Drug List (CDL)?

To reduce healthcare costs, only cancer treatments on the CDL can be claimed under MediShield Life, MediSave and IPs. This has been effective for MediShield Life and MediSave since 1 September 2022 and will come into effect for IPs from 1 April 2023

Treatments under the CDL are generally deemed to be clinically proven and more cost-effective. According to the Ministry of Health (MOH), the list includes over 200 approved drugs, which cover around 90% of treatment used by public healthcare institutions. The updated CDL can be read here.

How does it affect me?

Before 1 Sep 2022, MediShield Life pays up to $3,000/month for all cancer drugs and IPs often cover costs on an as-charged basis (i.e. no limit) with a small co-payment. The table below summarises the changes in your IP coverage with regard to whether your cancer treatments are under the CDL or otherwise.

Summary: Changes to Cancer Coverage Benefits for Medishield Life, Medisave And IPs

The differentiated approach towards treatments on the CDL or otherwise means that two existing benefits will cease: the broadly applied as-charged benefit for chemotherapy and immunotherapy treatments. Instead, the IP coverage of your cancer treatment varies across insurers and will largely depend on whether they are on the CDL or not.

If you had purchased a rider to your IP to further reduce your out-of-pocket expenses, they will be able to cover drug indications beyond the CDL. However, the coverage varies across insurers.

For example, here are the differences between the three insurers: Income, Singlife and Raffles Health Insurance (RHI).

Comparison between Income, Raffles Health Insurance, Singlife IP Riders for Non-CDL Treatments

2 Outpatient cancer drug treatments (Non-CDL) are excluded from the maximum co-insurance stated in the benefits schedule of the respective insurers. Treatment on the CDL will still enjoy the 5% or 10% co-payment limits, depending on the rider and insurer, subjected to a capped limit of $3,000 for each policy year for treatment provided by insurer’s panel and extended panel.

3 Applicable to all Singlife Health Plus Rider Cover except for Singlife Health Plus Deductible Cover.

At first glance, the additional limits of Income riders may seem more attractive, but you may also want to consider the co-payment (or out-of-pocket) amount required. Depending on your total medical bill, the co-payment percentage could have a large impact on how much cash you need to fork out.

To ensure that the needy will not be denied medical treatments due to cost, treatments under the CDL may be further subsidised under the Medical Assistance Fund (MAF) at public healthcare institutions, depending on your per capita household income.

If I am currently undergoing cancer treatment, how does it affect me?

If you have an Integrated Shield Plan/Rider

All IP insurers have committed to providing transitional support to IP policyholders undergoing cancer drug treatments beyond 1 April 2023 to help them ease into the change while more drugs are added to the CSL over time. You can check in with our client advisors on the exact support details.

Thereafter, the revised benefits will apply. If your cancer treatment is not on the CDL, you may face an increase in your out-of-pocket expenses, until your treatments are approved to be on the CDL.

If you do not have IP and are covered under Medishield Life only

Patients with MediShield Life will only receive additional financial support for their current course of treatment to ensure that their ongoing course of treatment is not disrupted. Generally, they may have more out-of-pocket expenses if the treatment is not on the CDL. Subsidised patients can approach a medical social worker in their respective public healthcare institution to find out the assistance measures available.

What if my current treatment uses drugs not on the CDL and was previously covered “as-charged” and I do not have an IP rider?

Cancer patients who are receiving private care with treatments not on the CDL, may need to discuss with your doctor and consider treatment options on the CDL.

Otherwise, you can also consider requesting to be directly referred to subsidised specialist care at public healthcare institutions, to review your treatment plan and apply for additional financial support if required.

How do I get financial support or additional coverage if I wish to opt for treatments not on the CDL?

IP insurers have collectively decided to continue to cover treatments beyond the CDL through benefits provided by the rider component of the plan. This will provide greater choice for those who prefer and wish to pay for broader coverage. The rider component is payable by cash only and cannot be funded from your MediSave.

Alternatively, you can consider tapping on your critical illness insurance plans, which provide a lump sum payout upon diagnosis of critical illnesses including cancer, to fund treatments which are not on the CDL. You can also consider medical insurance plans which specifically cover cancer treatments.

Singlife Cancer Cover Plus is an example of a cancer treatment coverage plan designed to offer protection against large medical bills from cancer treatments. It complements your coverage under existing plans, and you do not need to be under Singlife Shield (i.e., you can be under IncomeShield and still be covered by this supplementary plan). You can significantly reduce your out-of-pocket cancer treatment expenses both locally and overseas.

With these changes, should I switch my IP to the “best” IP provider which provides better coverage?

Non-CDL benefits should not be the key deciding factor on whether to switch your IP insurer. Instead, switching IP insurers may result in the loss of coverage for pre-existing conditions which could have been covered by your current plan.

Instead, to get more assurance for your cancer care treatments, you can consider upgrading your current IP plan to include a rider or consider buying standalone cancer coverage plans offered by various insurers. These are designed to cover your out-of-pocket cancer treatment expenses and may not be tied to your IP insurer.

Let Us Help

Navigating the news of a cancer diagnosis and going through the treatment options are already challenging tasks, and the CDL implementation adds an extra layer of complexity.

It is important to understand the changes and how they may affect you so that you can consider your options carefully – in light of your risk factors and budget – and take proactive steps to ensure that you have the support you need to focus on your treatment and recovery during this difficult period.

If you need help going through the available options, do send your queries to us, and our fully-salaried, conflict-free client advisers will be ready to assist you.

Disclaimer

The information contained herein does not have any regard to the specific investment objective(s), financial situation, or the particular needs of any person. Buying insurance is a long-term commitment and should be bought according to your needs, and products’ suitability. You may wish to seek advice from our client adviser before making any financial decision.