Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Despite the common belief that one will only become physically weaker and disabled in old age, the fact remains that disability may happen to anyone at any age.

It may be due to accidents – there were more traffic accidents involving injuries or fatalities in the first half of 2022, compared to the same period in 2021 – or even unanticipated medical conditions. One such condition is stroke. A stroke happens when the blood supply to part of the brain is interrupted, resulting in brain damage. While older people are more likely to suffer from a stroke, one in 10 stroke patients in Singapore is under 50, with patients as young as 24 years old.

Besides the high medical costs, we will also need to factor in the significant caregiving commitment and expenses. If you are thinking of getting disability income coverage, from now till 16 December 2022, MoneyOwl is offering free first-year disability coverage. Terms and conditions apply.

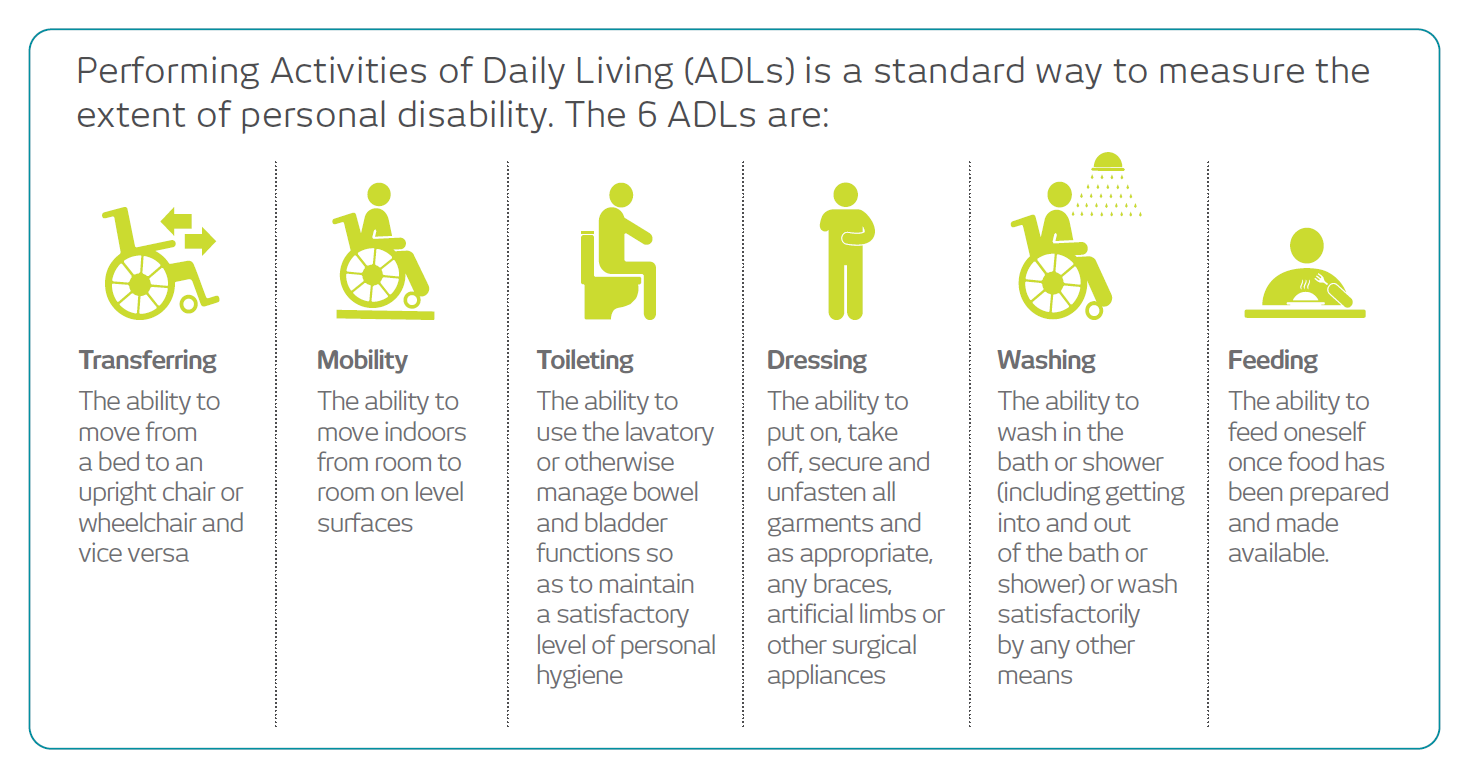

When such severe disability strikes, we will need to rely on others to carry out activities of daily living, collectively known as ADLs, for a prolonged period. These include needing someone else to help us with washing, dressing, feeding, toileting, walking or moving around, and transferring.

We need to prepare for such scenarios before they happen so that they do not cause a strain on our finances. It is even more critical for those of us with dependents who rely on our working income. We hence need to consider covering the possible loss of income or expenses during this extended period of disability.

Existing Long-term Care Insurance

Most of us will have heard of CareShield Life, which was launched in 2020. It is a long-term care insurance scheme designed to be basic and universal – provide basic financial support to help Singaporeans cover their expenses in the event that they become severely disabled. While CareShield Life will pay out over your lifetime while you remain severely disabled, the payouts are designed to be modest – $600 a month at 2020 and increasing by 2% each year.

With home-based care likely to cost over $1,000 a month – comprising a live-in caregiver and other miscellaneous costs such as rehabilitation and special transport costs – insurers have stepped in to offer CareShield Life supplements to give higher payouts with less stringent qualifying criteria.

So this means for a 30-year-old who wants to receive a monthly benefit of $1,000 for a 3-year period, the annual premium is just $80 per year.

Disclaimer: The information contained herein does not have any regard to the specific investment objective(s), financial situation, or the particular needs of any person. Buying insurance is long term commitment and should be bought according to your needs, and products’ suitability. You may wish to seek advice from our client adviser before making any financial decision.