Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

The explanation behind MoneyOwl’s Bionic advisory and roboadvisory together.

Dentist. Many people hate to visit one. I can’t say I love to visit dentists but I don’t loathe it. That is because I have a very experienced dentist who is very gentle, good at her work and extremely reassuring.

Six days ago, I had my implant surgery done. Implant surgery is a pretty rough surgery whereby they cut open your gums, drill into your jawbones and screw in a metal post. Thankfully, I have a high threshold for pain. So, when I sat in the dentist’s chair that day, I was pretty calm – until when I saw all the equipment, when I became a tad, just a tad nervous.

But my dentist made me feel at ease. She told me that she was going to put numbing cream on my gums before she gave me the injections. Knowing that I don’t respond very well to certain types of anaesthesia, she used a different one. When she was giving me the injections, she assured me again and did it very slowly. I didn’t feel much pain. And when the surgery started, she kept updating me on what she was doing and how long more it would take.

Before I knew it, the surgery was over. I can’t say that the entire experience was pleasant but with my dentist’s skilful hands, her constant updates and encouragement, I went through the surgery comfortably. So, what has this got to do with making financial decisions?

You see, over the past 2 years, Singaporeans saw a slew of investment roboadvisors being launched. The roboadvisor fever really started in the US when a company called Betterment launched their online investing service in the US in 2010.

Roboadvisors are online investment services provided by fintech companies. The idea was simple. Code those complex investment making decisions into an algorithm and after investors go online to answer a few simple questions, a suitable low-cost investment portfolio will be recommended.

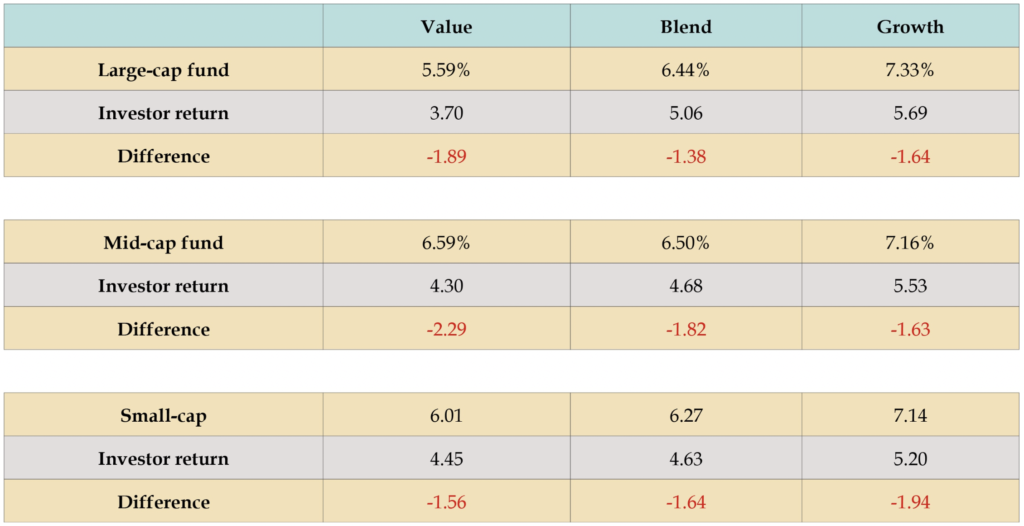

Investors are then expected to stay invested through the ups and downs of the markets and get the returns they deserve. I have no problems with using technology to deliver investment services. The problem I have is the over-reliance on technology in solving all financial problems. Investment services provider, Morningstar did a study on the returns of various funds versus what investors actually got by investing in those funds.

The table here shows that for all the different categories of funds, investors were not getting the returns that the funds delivered. Why? It was largely due to investors getting out of the markets earlier when they became volatile.

Source: Morningstar, Inc

The thing about making financial decisions for many people is this: the head understands the logic but the heart does not. While the head might understand the need to ignore short term noises and to stay invested for the long term, when the markets tumble, or when there is news, or when there are rumours or predictions of markets crashing, the heart rules. And this does not just apply to investing. It applies to other financial decisions in life.

So, while technology can tell you what decisions to make, whether you make them, and whether these decisions are really suitable for you is a separate matter. This is when having human financial advisers are so important. Unlike machines, human advisers possess empathy, wisdom and experience, all of which are necessary ingredients to making a good judgement as well as performing behavioural coaching.

This is why when MoneyOwl launched the insurance advisory service last year and the investment advisory service for the ordinary man on the street last week, it was not a roboadvisory but a bionic one. Bionic advisory is the use of roboadvisors together with salaried human advisers to deliver conflict-free, competent and comprehensive advice. While we use technology for:

- Extracting your information from MyInfo for speedy compliance due diligence

- Computing your financial needs, ascertaining your financial health, as well as your willingness to take risks.

- Creating investment portfolios with suitable asset allocation (different proportion of our money invested in equities and bonds) based on your need, ability and willingness to bear risk.

- Using quantitative methods to select suitable investment instruments for your portfolios

- Executing your investments in the most cost-efficient way

- Performing regular rebalancing of your portfolio

- Doing regular progress checks in the context of your overall financial plan so as to keep you motivated to stick to your plan

We believe that human advisers are best for:

- Listening to your needs, life aspirations and fears

- Judging your true willingness to take risk

- Making a qualitative judgement of the fund managers used for your investment portfolios

- Performing risk/behavioural coaching so that you can stay invested or not make rash decisions during market volatility

- Cheering you on to keep you motivated to stick to your plan

Remember my dental experience? While my head understood that the implant surgery would be a safe one and that it would be over after one and a half hours, the minute the surgery started, I became a tad nervous. While the X-ray machine, the anaesthesia and the expensive dental equipment (the so-called technology) were great for performing my implant surgery, it was my dentist who kept me comfortable throughout the surgery. Of course, you might say that unlike roboadvisors, X-ray machines and dental equipment cannot operate on their own. But even if there is such a thing as a robodentist, would you use one? Technology is useful, but when it comes to handling complex human emotions, machines alone

won’t cut it.

The story was told of Michael Faraday, that he was trying to explain his discovery of electricity to William Gladstone, but Gladstone was unimpressed. “But what use is it?” Gladstone had asked with frustration. “Why sir,” replied Faraday impatiently, “there is every possibility that you will soon be able to tax it!” While there will be many Gladstones who will miss or dismiss the use of technology, there will be an equal number of Faradays who will be so absorbed in technology and thus miss the social implications and limitations.

There is no need to take sides. Embrace both technology and humans. They work best together. That’s bionic.

Christopher Tan is the Executive Director, MoneyOwl, Singapore’s first bionic financial adviser and also the CEO, Providend, a fee-only retirement financial adviser. Both MoneyOwl and Providend share the same investment philosophy.

The edited version has been published in The Sunday Times on 19th May 2019.

Announcement: With effect from 1 June 2022, MoneyOwl is a 100% NTUC Enterprise (NE)-owned company.