Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

With Singapore’s headline inflation rising to 5.4% in March 2022 – the fastest in the last 10 years – it has left many investors concerned about the impact of inflation on their investments.

In this article, we seek to demystify the inflation monster and help you take the right action with your money.

What is inflation?

Inflation is the measure of how much the price of goods (such as bread or mobile phones) and services (such as movie tickets and transport fares) increase over time. Some of us may remember when the price of kopi cost less than $1, but it’s impossible to find such prices anywhere now.

Imagine you have $100 in your bank account that pays you a 1% interest annually. It’s great to see that by the end of the year, you will have $101 in your bank account for doing nothing. But if inflation is running at 4%, you would have needed a $4 interest on the same $100 capital in order to maintain the same buying power that you started with a year ago. Basically, if your interest rate given on your savings isn’t higher than the rate of inflation, then your money will have less purchasing power and your standards of living will become lower.

To be fair, inflation is not always bad. An economy needs a “healthy” level of inflation for sustainable economic growth. What we are concerned about is when inflation is too high or when deflation is happening. Deflation is the general decline of prices of goods/services and it is an economic phenomenon usually associated with recessions of an economy.

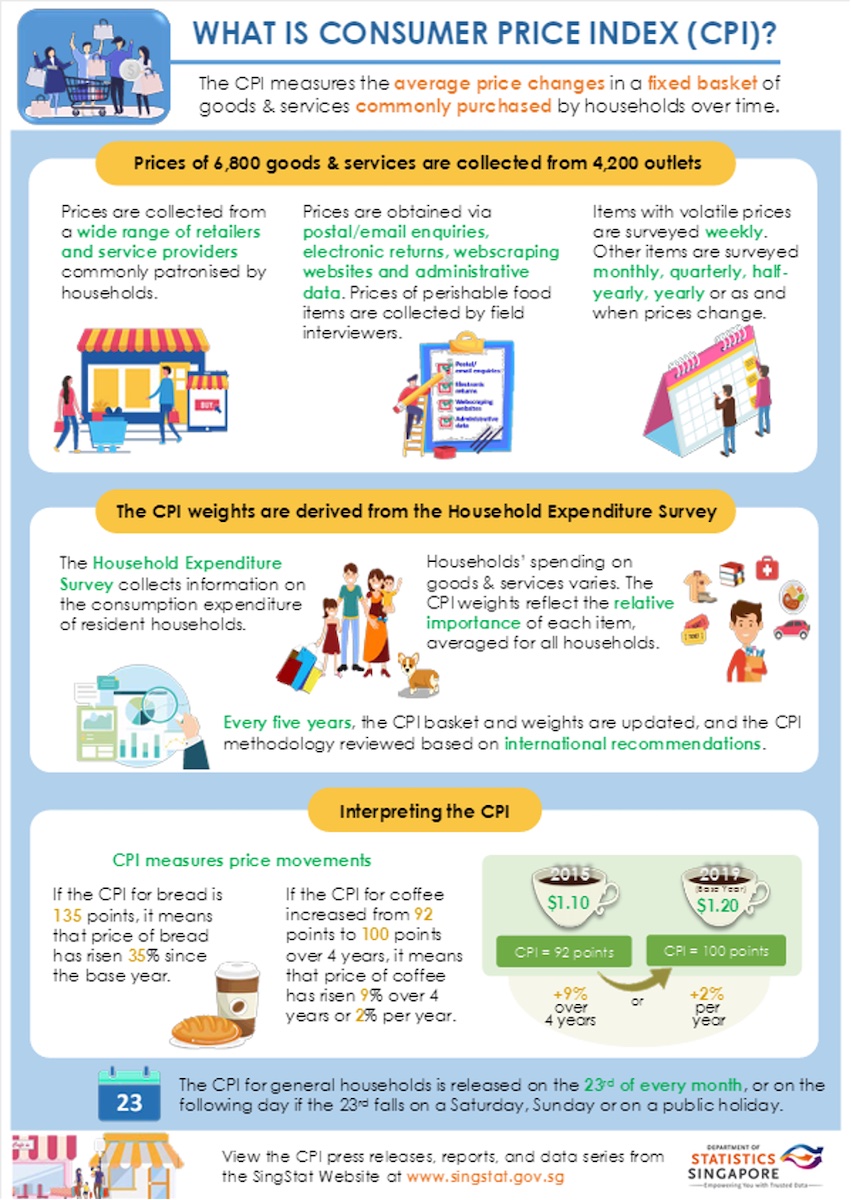

Inflation doesn’t just affect food prices and transport fares, but in general, almost everything is more expensive today than before. To monitor Singapore’s inflation, the Department of Statistics compiles various prices of goods and services monthly to calculate an index known as the ‘Consumer Price Index (CPI)’. The methodology in the index calculation is described in the image below.

Types of inflation

Here are the types of inflation and some examples of how they can happen.

Demand-Pull Inflation

Demand-Pull Inflation is typically caused by excess demand chasing limited goods and services. The higher demand makes consumers/businesses willing to pay higher prices in order to get the goods/services they want, causing an upward pressure on general consumer prices.

For example, a lemonade stand makes 100 cups of lemonade every day and sells 100 of them for $1 each. However, over time, the owner starts experiencing customers coming in and asking for a cup of lemonade after they are sold out. If the owner kept production constant (still producing 100 cups only each day), the seller will start increasing prices to reduce the excess demand, knowing the lemonade is popular.

Cost-push Inflation

Cost-push inflation occurs when the prices of production costs for goods/services increase. The higher cost is then passed on to consumers/buyers of the goods/services.

Using iPhones as an example, imagine you are the CEO of a company that supplies raw materials for Apple to produce their iPhones, and you decided to increase the prices of the raw materials supplied. Apple would then have to pay more to get their raw materials. However, to do so and maintain profits, they would need to earn more money. So Apple increases their price of iPhones. Consumers then end up paying more for the same goods. This could also happen if Apple decided to double their employees’ salaries, which also translates to a higher production cost and the higher cost is passed on to consumers/buyers of iPhones.

Singapore Inflation

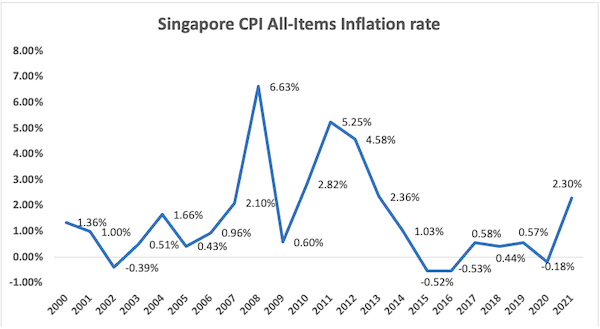

Naturally, too high of inflation is bad for an economy as your money quickly loses its purchasing power. The difference between this year’s and last year’s CPI is known as the “annual inflation rate”. In most countries, the job of managing inflation will fall on the central bank, by keeping annual inflation controlled at a sustainable rate (most countries use a 2% inflation rate target). Currently, Singapore’s 2021 annual inflation is at 2.3% which is the highest level since 2013. As of March 2022, the Year-on-Year Inflation has risen to 5.4%.

The higher rate of inflation in Singapore is not isolated. For the past two years, inflation has been creeping up globally. In 2021, the United States (US) annual inflation rate was 7%, the highest level in 39 years!

Inflation and how it impacts interest rates

To curb global inflation, the Central Bank of US (Federal Reserve, “Fed”) has decided to increase their benchmark interest rates (aka Fed Funds rate) in the country. As of April 2022, the current Fed Funds rate stands at 1% and the Fed is committed to raising rates 6 more times to 2.5% by the end of 2022, with each increment being 25 basis point (0.25%).

The Fed Funds rate is a benchmark for global interest rates and is simultaneously known as the ‘borrowing cost’ of money.

A higher interest rate (higher borrowing cost) will discourage consumer and business spending as it now costs more to borrow money for expenses or expansions. The higher costs of borrowing money essentially means that lesser money is circulated in the economy and demand is reduced.

The reduced demand will lower inflation as there is lesser money chasing goods/services. Inflated prices may then get some relief from having too much demand in the economy.

How inflation affects your investments

The impact of inflation on investments depends on the investment type. For investments with a set annual return, such as regular bonds or bank savings deposit, inflation can hurt performance – since you earn the same interest payment each year, it can cut into your earnings. If you receive a payment of $100 per year, for instance, that payment would be worth less and less each year given inflation.

For stocks, inflation can have a mixed impact. Inflation is typically high when the economy is strong. Companies may be selling more, which could help their share price. However, companies will also pay more for wages and raw materials, which increase their costs. Whether inflation will help or hurt a stock can depend on the performance of the company behind it.

But comparing among stocks, growth stocks (e.g. Technology) that have most of their value derived from future earnings growth expectations will most likely be hit the most as higher inflation will promote central banks to raise interest rates (higher borrowing cost for business expansion) which will affect the outlook of their future earnings.

When it comes to Singapore REITS (S-REITS), higher inflation will impact S-REITS from two perspective with direct and indirect effects. The direct effects stem from higher energy prices, on average, energy cost that REITS bear themselves is about 3-8% of operating cost. If certain REITS are unable to pass on energy prices, bankruptcies may happen.

On the other hand, the indirect effect will be from the higher interest rates. If inflation remains high and the US’s Fed decided to raise the Fed Funds rate more aggressively, S-REITS will have higher interest costs, which would erode their company’s business value.

Generally, the Central Bank of a country may raise interest rates to fight increasing inflation, but higher interest rate tends to weigh on asset prices, as less money is borrowed for investing causing less demand for investment assets. Additionally, higher inflation also reduces confidence in the economy as it increases uncertainty into the economy’s future outlook.

A recent article showed that demand for Singapore Savings Bond has risen to the highest it has been since July 2019. The increase in demand for savings bond was a ‘flight to safety’ behaviour due to confidence in equities and bonds crumbling as most investors believe that decades-high inflation will hurt asset prices.

In the next section, we will share some evidence why investing in savings bonds or keeping your money in cash may not be the right choice in such times.

How to deal with inflation

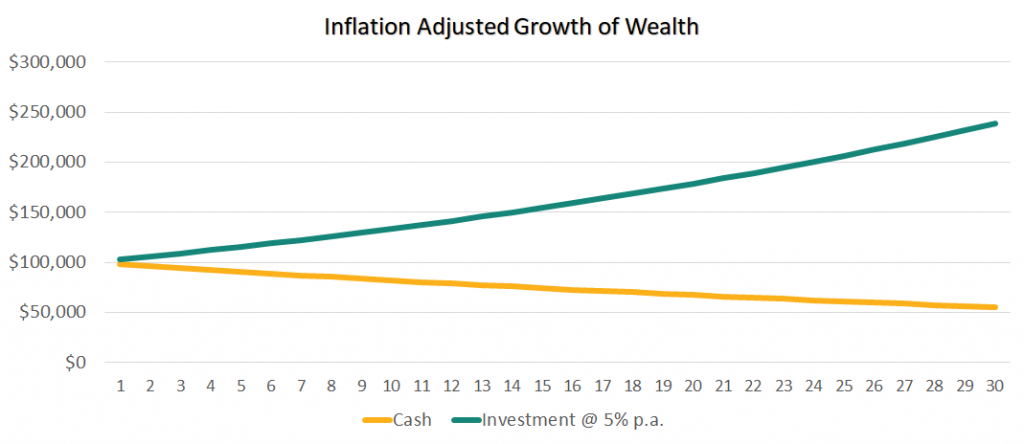

No one can predict the unexpected but you can plan for it. If you want to prevent inflation from eroding your wealth, it is recommended to structure your investments to outpace it by investing in a globally diversified portfolio of stocks and bonds. As shown in the graph below, keeping your cash on hand and letting inflation erode its value versus finding an investments offering 5% a year on average. The answer is clear on what you should do.

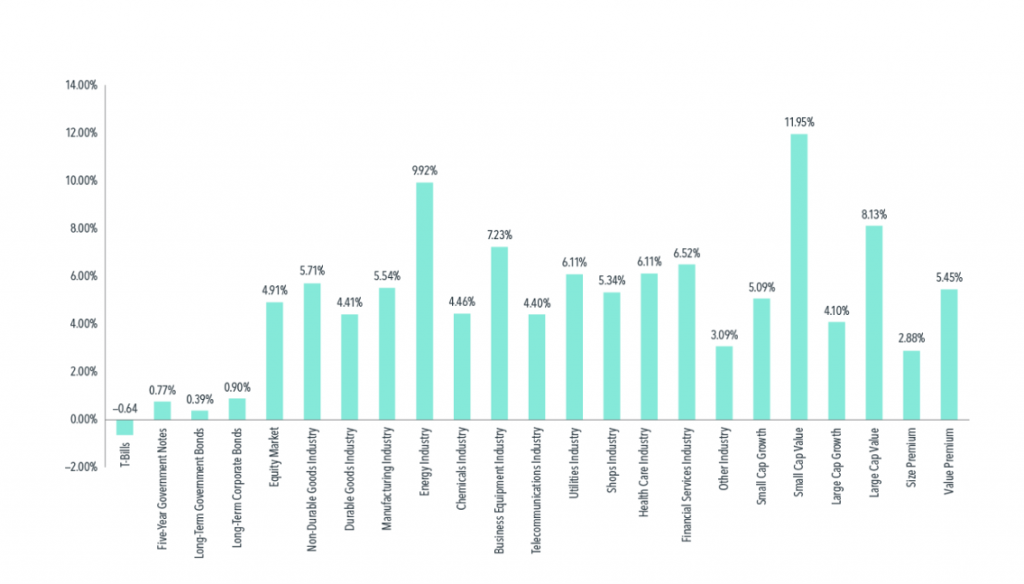

Take a look at how various asset classes has performed over different inflationary periods. Evidence from a study done by Dimensional Fund Advisors shows that these asset classes have had good returns when inflation has been strong or when it’s been low.

Historically, assets such as stock and bonds have provided a long-term return that can more than offset inflation. The analysis over 1927–2020 is useful because it covers periods with double-digit US inflation (like the 1940s and ’70s) as well as periods with deflation (like the Great Depression, 1929–32). But you will find similar results over the most recent 30-year period (1991–2020), when US inflation was relatively mild and stable.

The study covers non-USD bonds, developed- and emerging-market equities, real estate investment trusts (REITs), and commodities. Overall, outpacing inflation over the long term has been the rule rather than the exception among the assets studied.

As we can see, Equities historically offers higher expected returns than bonds, however, allocating more of your capital to equities may not be appropriate for all investors as you may take on more market risk than you are comfortable with. It is a well-known fact that equities are embedded with higher volatility than bonds.

REITs also provide natural protection against inflation. Real estate rents and values tend to increase when general prices do. This supports REIT dividend growth and provides a reliable stream of income even during inflationary periods.

Another alternative is to hedge inflation exposure with assets that are Inflation indexed securities – such as Treasury Inflation-Protected Securities (TIPS). TIPS prices are positively correlated with inflation expectations and thus are a good hedge for inflation. Unfortunately, such bonds are not available in Singapore and it wouldn’t be wise to use the US or global inflation indexed bonds since Singapore’s inflation experience is probably different from theirs.

To summarise, the investing framework to combat inflation is really simple. It is natural to be concerned about the potential impact of high inflation and rising interest rates on portfolio. However, history has shown that it is also possible for investors to put themselves in a better position by holding on to their investments with a long-term horizon.

Regardless of what you choose to do with your personal finance, keeping your money in savings bond or savings account during high inflationary times will give your money a higher chance in eroding away its purchasing power.

Suppose savings rate is lower than the inflation rate, then you have to outpace it by investing with assets with higher expected returns. An additional good rule of thumb in times of inflation is also to plan and control your budget for future expenses.

Inflation and retirement

One of the biggest risks faced by Singaporean retirees is outliving their savings due to their longevity and having enough wealth to sustain an income for life.

You may find a 4% withdrawal rule for your nest egg helpful in providing you with a structured drawdown that has taken into consideration actual inflation year on year while also sustaining pay-outs for your income needs for at least 30 years.