Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

With prices rising across the board – from groceries and meals, to COE and housing prices, we may be feeling quite discouraged.

But we found one thing that is dropping in price – term insurance! Read on more to see if you can reduce how much you pay for insurance while maintaining – or even increasing – your coverage.

Term Life Insurance – Is It Worth It?

Some of us may not be comfortable with term life insurance, as it means never seeing the premiums you pay. Instead, whole life plans, which offer a cash component, gives you more assurance that the money you pay will come back in some form.

But premiums for whole plan plans can be several times that of term life insurance. It is because term life insurance is in fact a component of whole life plans. Whole life plans are able to provide you with cash value because a part of the premium is invested by the insurer to build up the cash value.

Are You Sure Term Life Insurance Is Cheaper Now?

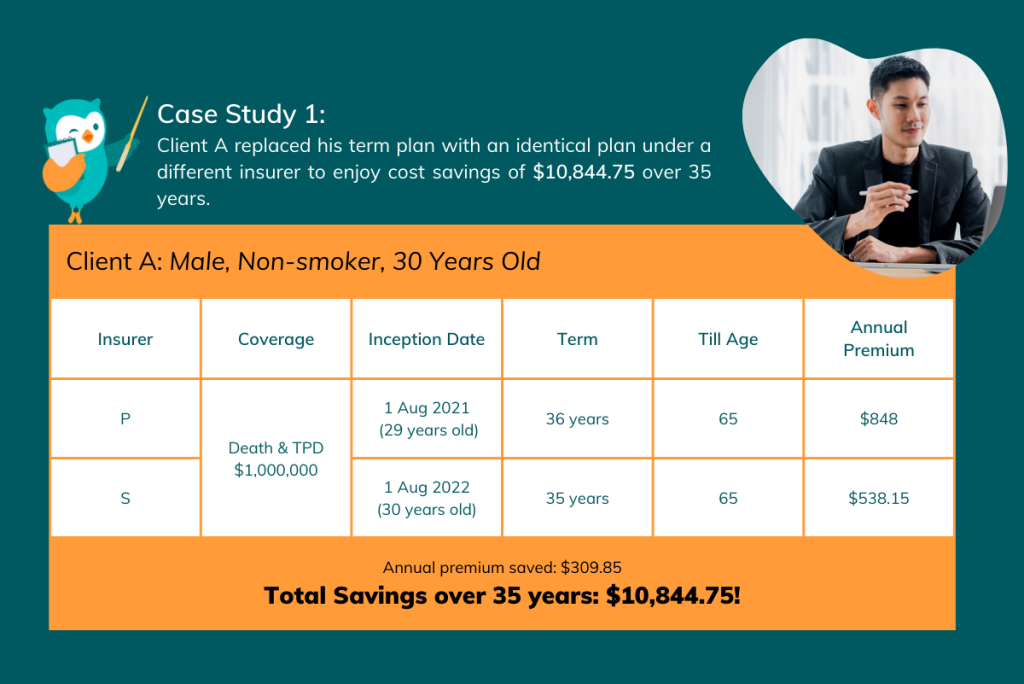

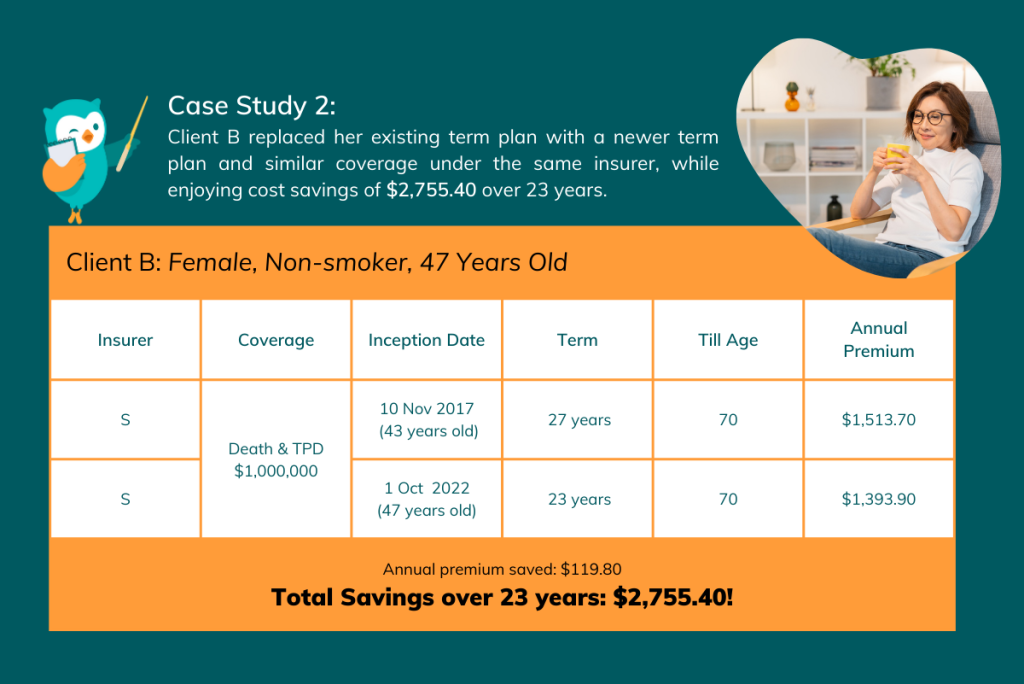

Don’t just take our word for it. Here’re two real-life examples where we were able to achieve significant cost savings of over $10,000 for one of our clients.

Both clients were able to save on insurance costs without being worse off in terms of protection, as there were no changes to their health condition when they took up their new plan, as compared to their previous term plan.

Furthermore, between a term life and a whole life plan, it is likely that most of us can only afford a term life plan to get the full protection that we need. While the ideal amount of coverage varies from person to person, the Life Insurance Association Singapore recommends about 10 times your annual income as basic life cover. With premiums for whole life plans likely to be five times more than term life plans, it comes as no surprise that whole life policy-holders are more likely to be underinsured compared to term life plan policy holders.

The Only Thing Cheaper Today Than Yesterday

The cost of term life insurance has been steadily dropping over the years. This is mainly due to us living longer.

| 2021 | 2011 | 2001 | 1991 | 1981 | |

|---|---|---|---|---|---|

| Total Life Expectancy at Birth* | 83.5 | 81.9 | 78.3 | 75.6 | 72.5 |

| Males* | 81.1 | 79.5 | 76.3 | 73.5 | 70.1 |

| Females* | 85.9 | 84.1 | 80.3 | 77.9 | 75.2 |

The table above shows Singaporeans’ life expectancy increasing significantly over the decades. And life expectancy is one of the key factors in how insurers price their life insurance premiums. This is because with better quality of life and advancement in medical treatments, people are living longer. And the longer you are likely to live, the lower the risk to insurers of having to pay out during your working years, and the cheaper they can charge for term life insurance premiums.

Put another way, most policyholders typically buy term life insurance to cover them against financial loss until age 65 or 70. But as more Singaporeans are expected to live into their 80s, the chance of insurers paying out the death benefit is greatly reduced. Hence, we see insurers offering higher cover at lower premiums.

Another reason for lower term plan premiums is the increased competition among insurance companies. We have seen new players in the market, including some General Insurance companies moving into the life insurance space. With greater competition, insurers will cut their prices to increase their market share. Insurers seek to expand their market base as the more policyholders they have, the better they are able to spread the risks to further lower insurance costs. Hence, if you had bought a term plan say 5 years ago, a similar term plan offering the same coverage would be sold at lower premiums today, even if you are entering the policy 5 years older. This runs contrary to the conventional wisdom that the younger you buy a life policy, the cheaper your premiums.

Should I Buy Or Change My Term Plan Now?

You may want to get a new or additional term plan if you want to get your insurance needs fully covered at the lowest cost possible. Your circumstances may also have changed and you now need higher coverage as you have heavier family commitments.

If you are thinking of getting a term plan, now is the best time to do so. From now until 31 March 2023, enjoy a 30% perpetual (not just for the first year) premium discount* on term life insurance. Click the button below to find out more. T&Cs apply.

What’s more, we offer up to 50% on first-year commission rebates for all qualifying plans^. This rebate is estimated to be about a quarter of your annual premium, so you get more value out of your insurance plans.

One very important caveat! Changing your term plan is not recommended if you have developed medical conditions since the inception of your existing plan. This is because the insurers will not pay claims on pre-existing conditions and undeclared conditions. There may also be a waiting period for new plans with critical illness coverage after inception, so hold on to your existing plans for at least the waiting period so there won’t be any potential lapse in coverage.

To find out if you can achieve cost savings or whether a replacement of term life insurance is suitable for you, you can indicate your interest below and a friendly, fully salaried MoneyOwl client adviser will get in touch with you.

Even if there are no cost savings after the review, at least you remain confident knowing that you have secured the lowest possible cost for adequate coverage. Just as we spring clean our closets and house before the new year, our insurance portfolio will also benefit from a thorough review by an expert from time to time.

Disclaimer

The information contained herein does not have any regard to the specific investment objective(s), financial situation, or the particular needs of any person. Buying insurance is a long-term commitment and should be bought according to your needs, and the products’ suitability. You may wish to seek advice from our fully-salaried Client Adviser before making any financial decision

*^ Terms and Conditions apply. For more information, refer to our Insurance Promotion Page and Insurance First-Year Commission Rebate pages for more details.