Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Inflation may be at an all-time high deterring potential investors from investing. Our investment team shares why now is the best time.

(12 September 2022 – 16 September 2022)

Last week’s US consumer price index released on Tuesday showed an 8.30% year-on-year increase, sending global stock indexes to their steepest weekly declines since June. In addition, the latest inflation report showed that prices aren’t settling down anytime soon and increased the likelihood that the US Federal Reserve will continue to lift its benchmark interest rates further than expected.

The market fell for the fourth time in 5 weeks, with the S&P 500 and MSCI World dropping 4.77% and 4.23%, respectively. MoneyOwl’s 100% Equity portfolio was relatively resilient owing to the value factor outperforming, falling by 3.59% in comparison. In fixed income, the US 10-year treasury bond yield was seen flying up 13 bps to 3.45% on Friday, representing more expectation of an interest rate increase from the Federal Reserve. Fixed Income assets overall declined, as the Bloomberg Barclays Global Aggregate Bond Index fell 0.62%.

Start Growing Your Money Early

With inflation multi-decades high, the cost-of-living problem looms for many people worldwide; investing in inflation-beating assets is more important than ever. When you think about your life span, you can easily break up into three parts. A third of our lives are growing up, another third maturing into various responsibilities, and the remaining third of our lives are in retirement.

Given that Singapore has one of the world’s longest life expectancies at 84.8 years, it is not surprising that you will spend 25-30 years in retirement, almost as long as you have worked. With this many years in retirement, having enough savings to last you does not happen by accident. Instead, it requires you to start growing your money as soon as possible.

Time is money!

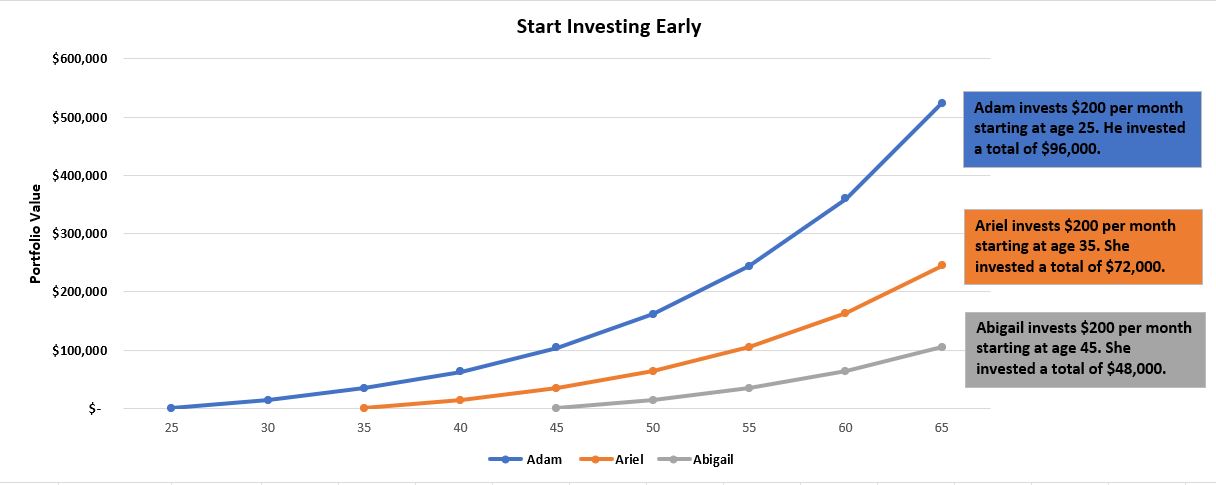

To illustrate how investing early can help you achieve your retirement goals, consider three investors, each getting a 7.0% p.a. rate of return with the same monthly investment amount of $200.

As the saying goes, the stock market is kindest to those who stay faithful to it longest. Starting early in your investment journey can help you to achieve your retirement goals much faster. For example, Adam started investing at the age of 25 and managed to have a portfolio value of more than $500k by the time he turned 65. On the other hand, Ariel and Abigail started 10 and 20 years later than Adam but could only attain a portfolio value of $245k and $105K respectively.

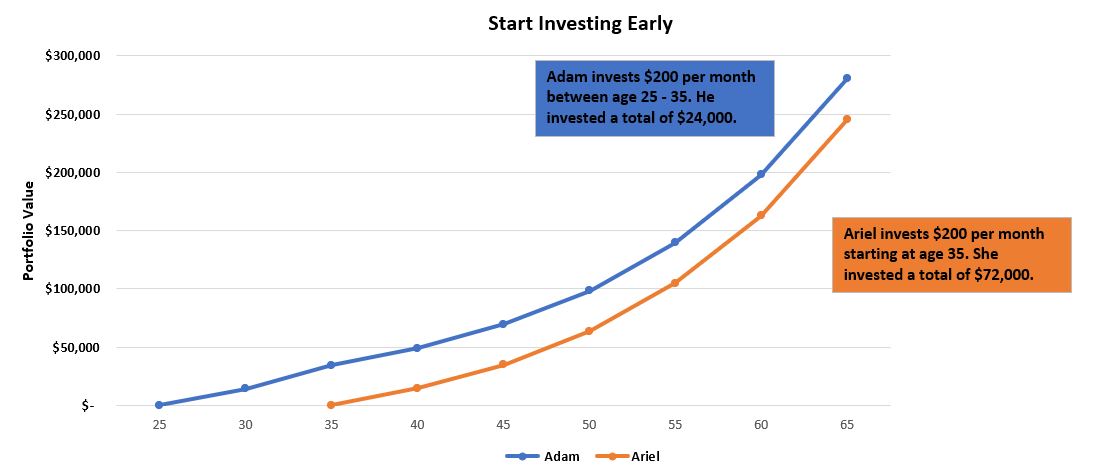

In fact, time invested is so important that Adam can stop adding to his investments at age 35 and still have more than Ariel at age 65.

If Adam were to contribute $200 per month from age 25 to 35 – contributing only $24,000 total over 10 years – his investments would be worth around $280,000 compared to Ariel’s portfolio value of $245,000 when they both reach age 65!

Whether you have a large or small capital to start investing matters in the long run, you don’t have to start investing $1,500 a month right away. It’s OK to start small, as long as you start. You can always increase your contributions later. Remember, starting early and staying invested can help you to achieve your financial goals and possibly retire earlier.

US Consumer Price Index

Tuesday’s release of worse-than-expected inflation data sent the major global stock indexes to their steepest daily declines since the early days of the pandemic in March 2020. The latest monthly inflation report increased the likelihood that the US Federal Reserve will lift its benchmark interest rates by 0.75% —or perhaps even by a full percent—in its upcoming meeting ending on Wednesday (21 Sep).

Goldman’s Cull

Goldman Sachs is embarking on its biggest round of jobs cuts since the start of the pandemic, with plans to eliminate several hundred roles starting this month. The headcount reduction is a resumption of the bank’s annual culling cycle that it had largely paused as Covid-19 swept around the world. Analysts expect the bank to post a more than 40% drop in earnings this year.

Singapore Show Your Hand

Singapore Exchange is planning to ask companies to reveal exactly how much their CEOs and directors are paid. The bourse’s regulator will also propose imposing a nine-year cap on the tenure of independent directors. There’s been a global push for more transparency on executive pay. The US Securities and Exchange Commission introduced a rule requiring the disclosure of additional details such as performance incentives last month. Singapore is also seeking to change low board renewal at local companies, where it’s common to see independent directors in their positions for about a decade or longer.

Fedex slowdown

FedEx withdrew its earnings forecast on worsening business conditions, dragging the broader market down in a potentially worrying sign for the global economy. The package-delivery giant flagged weakness in Asia and challenges in Europe and said conditions could deteriorate further in the current period.

Chinese Yuan’s Slide

China’s central bank (PBoC) is in a dilemma as the central bank continues to implement easy monetary policies while the economy continues to be held hostage by Covid-19. However, increasingly loose monetary policy sets the Chinese central bank apart from global central banks as they continue to tighten their policies to combat inflation. The resulting effect is in a weaker national currency, the Chinese Yuan, which tests the Chinese policymakers’ tolerance. Moreover, a weaker Yuan could stoke fear of capital outflows as Yuan-denominated assets become less attractive.

Read more Market Insights here.

Disclaimer: While every reasonable care is taken to ensure the accuracy of the information provided, no responsibility can be accepted for any loss or inconvenience caused by any error or omission. The information and opinions expressed herein are made in good faith and are based on sources believed to be reliable but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Expressions of opinions or estimates should neither be relied upon nor used in any way as an indication of the future performance of any financial products, as prices of assets and currencies may go down as well as up and past performance should not be taken as an indication of future performance. The author and publisher shall have no liability for any loss or expense whatsoever relating to investment decisions made by the reader.

Follow MoneyOwl on social media for more awesome content on investments, insurance, and financial planning!