Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

With the recent announcements from the Ministry of Health regarding CareShield Life, here is what you need to know if you’re currently on ElderShield.

MOH announced that CareShield Life will be made available to all Singaporeans born in 1979 or earlier with effect from Nov 6, 2021. To make joining the scheme more convenient, those born in 1970 to 1979, who are insured under ElderShield400, and are not severely disabled, will be auto-enrolled into the scheme from Dec 1. Older Singaporeans are not auto-included as the shift would mean paying higher annual premiums and thus should be considered only after weighing the pros and cons.

If you’re someone or know someone who falls into this age band, you may be wondering if shifting to CareShield Life is a good choice for you. In this article, I will break down the considerations based on the additional benefits from the scheme as well as the additional premiums payable. Also, you may want to read this article if you would like to learn more about CareShield Life and how it is different from ElderShield or other disability insurances in the market.

1) Benefits

According to MOH, the Healthy Life Expectancy at birth for Singaporeans is 73.9 years. This is the number of years that a Singaporean is expected to live in good health. Since our average life expectancy is about 85 years and we are expected to live about 74 of those in good health, this means that we can expect to live about 10 years in poor health whether due to sickness or injury. In fact, MOH expects that 1 in 2 healthy Singaporeans aged 65 could become severely disabled in their lifetime, and of this, 3 in 10 could remain in disability for 10 or more years.

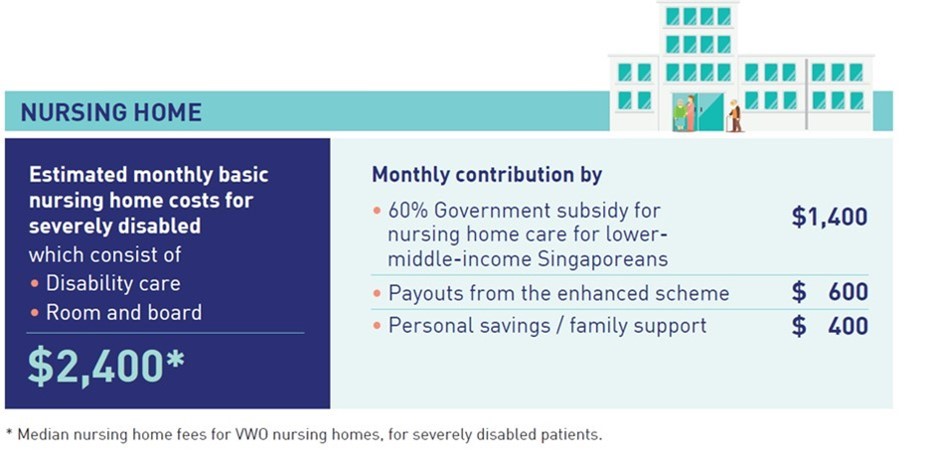

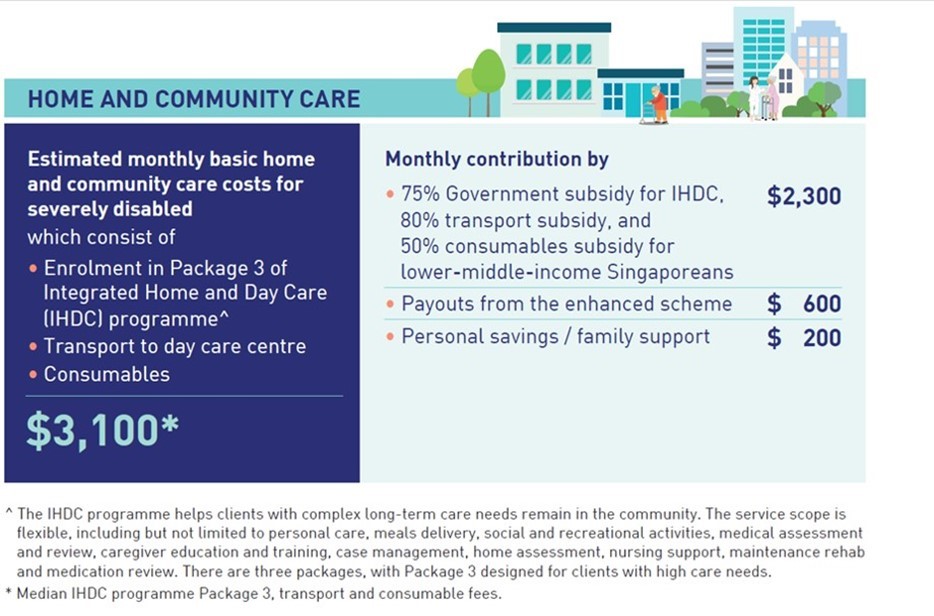

What this means is that monthly payouts of $300 to $400 under ElderShield for up to six years are going to be insufficient to meet long-term care costs. Long-term care options in Singapore include staying in a nursing home, being looked after by a helper or family member at home, or a combination of daycare and home care. The cost can easily range from $1,000 to over $3,000 per month before subsidies. Even after means-tested subsidies and CareShield Life payouts of $600 per month, there will still be a cost that has to be borne out of one’s retirement income.

Estimated Costs of Long-Term Care Options for lower-middle-income Singaporeans after subsidy and CareShield Life Payouts

Source: Eldershield Review Committee Report, 25 May 2018

Source: Eldershield Review Committee Report, 25 May 2018

Given the high probability of severe disability, the duration of disability (should it happen), and the strain of long-term care costs on the family, joining CareShield Life will certainly enhance your safety net for long-term care expenses. This saves you from setting aside more savings for your retirement to cater to this potential expense.

You can also increase these monthly payouts by adding a supplementary Long-Term Care Plan (or ElderShield Supplement) from a private insurer. Here’s a simplified comparison of the three long-term care supplements in the market.

| NTUC Care Secure | Aviva MyLongTerm Care | Aviva MyLongTerm Care Plus | Great CareShield | |

| Claim Conditions | Unable to perform at least 2 out of 6 Activities of Daily Living (ADL)**. | Unable to perform at least 3 out of 6 ADL. | Unable to perform at least 2 out of 6 ADL. | Unable to perform at least 2 out of 6 ADL (Pays 50% of monthly benefit if unable to perform at least 1 out of 6 ADL.) |

| Monthly benefit duration | Lifetime | Lifetime | Lifetime | Lifetime |

| Option to increase the payout to keep up with inflation | None | Option to increase monthly benefits by 2% or 3% per annum | Option to increase monthly benefits by 2% or 3% per annum | None |

| Premium Term | (i) Up to age 67; or(ii) Up to age 84 | (i) Up to age 97 (ALB); or (ii) Up to age 67 (ALB) or 20 years from entry age, whichever is later | (i) Up to age 97 (ALB); or (ii) Up to age 67 (ALB) or 20 years from entry age, whichever is later | i) Up to age 67 or 95 (ALB) ii) Up to age 95 (ALB) or 20 years from entry age (for insured entry age 47 to 64) |

| Additional Benefits | ||||

| Premium Waiver Benefit | At least 2 out of 6 ADL. | At least 1 out of 6 ADL. | At least 1 out of 6 ADL. | At least 1 out of 6 ADL. |

| Provides initial support benefit and dependent benefit? | Yes | Yes | Yes | Yes |

| Other benefits | Nil | Receive 50% of your last monthly benefit when your condition improves but you’re still unable to perform 2 ADL. | Nil | Nil |

| Additional annual premiums to get $1,500 monthly benefit (including CareShield Life) | ||||

| 45yo Male |

Premiums for this age group are not yet available

| $511.50* | $614* | $590.90* |

| 45yo Female | $629.40* | $755* | $797.75* |

*Premiums are net of 20% perpetual discount offered by the insurers.

**Activities of Daily Living refer to the activities of self-care such as washing, dressing, toileting, feeding, moving around and transferring.

These supplements can be paid using your MediSave savings of up to $600 per year, per insured. It is possible to enhance your coverage without any out-of-pocket expense too! If you are keen to learn more about which option is most suitable for you, speak to our salaried advisers for a non-biased consultation.

2) Premiums

To find out how much your CareShield Life premiums will be, head over here for the Premium Calculator e-Service (available from 6 November 2021). I have also included a simplified table below to provide an indication of how much more you’re likely to pay with and without means-tested premium subsidies. To further incentivise you to join/remain enrolled in CareShield Life, all citizens born 1979 or earlier who join the scheme before the end of 2023 will be entitled to a participation bonus between $500 to $4,000 paid over 10 years. This will be used to substantially offset the increase in premiums especially for those in the Merdeka and Pioneer Generation.

|

Entry Age

| Male | Female | ||||

| ElderShield400 | CareShield Life (no subsidy, with participation incentive) | CareShield Life (20% subsidy, with participation incentive) | ElderShield400 | CareShield Life (no subsidy, with participation incentive) | CareShield Life (20% subsidy, with participation incentive) | |

| 45 | $175 | $318 | $244 | $218 | $412 | $320 |

| 55 | $175 | $405 | $294 | $218 | $562 | $420 |

| 65 | $175 | $218 | $94 | $218 | $423 | $258 |

Based on the table above, the estimated increase in premiums ranges from 18% to 158% which is really meant to pay for the additional benefits of higher lifelong payouts under CareShield Life. If you can afford the additional premiums which can be paid fully using your MediSave savings, it does make sense to switch to CareShield Life. Putting into perspective, if you currently have at least $15,000 in your MediSave Account, the annual interest of about $600 would be more than sufficient to cover your CareShield Life premiums.

Next, let’s look at the total increase in premiums over the entire premium term. This is because while ElderShield premiums are level and payable only until age 65, CareShield Life payouts and premiums are expected to increase by 2% every year until 2024. Thereafter, further adjustments will be decided by an independent CareShield Life Council. Premiums are payable until 67 years old, or for 10 years if you join the scheme at age 59 or older.

The table below shows the total premiums payable for the same examples while considering that participation incentives last only for 10 years, and assuming that CareShield Life payouts and premiums will continue to increase at 2% per year.

|

Entry Age

| Male | Female | ||||

| ElderShield400 | CareShield Life (no subsidy, with participation incentive) | CareShield Life (20% subsidy, with participation incentive) | ElderShield400 | CareShield Life (no subsidy, with participation incentive) | CareShield Life (20% subsidy, with participation incentive) | |

| 45 | $3,500 | $9,546 | $7,537 | $4,360 | $12,112 | $9,590 |

| 55 | $1,750 | $5,944 | $4,455 | $2,180 | $8,049 | $6,140 |

| 65 | $0 | $2,291 | $1,033 | $0 | $4,378 | $2,703 |

The percentage increase in total premiums paid ranges from 115% to 269%. For the 65-year-old, they will have to continue paying premiums for another 10 years. This functions like a catch-up component for the additional benefits.

Lastly, let’s compare the total premiums payable against the total benefit gained from joining CareShield Life. The table below shows the total benefit received assuming the person qualifies for claims at the age of 75.

|

Entry Age

| Male/Female | ||

| ElderShield400 Total payout received over 6 years | CareShield Life Total payout received over 6 years | CareShield Life Total payout received over 10 years | |

| 45 |

$28,800

| $66,786 | $111,310 |

| 55 | $54,788 | $91,313 | |

| 65 | $44,945 | $74,909 |

Dividing the total benefit by the total premiums payable for the various scenarios will reveal that in most cases, a person entering CareShield Life at age 45 will be in a better position compared to staying on ElderShield. This is probably the reason why those born from 1970 to 1979 are automatically enrolled into CareShield Life. For those born from 1960 to 1969, if you are eligible for subsidies, you would likely be in a better position with higher coverage over a longer duration. For those born from 1950 to 1959, as you would be reaching the tail end of your premium term for ElderShield, the decision would boil down to your preference to continue paying premiums into your retirement years for the additional benefit.

Nonetheless, this research is an academic one. Your decision whether to move or stay on CareShield Life should be based on your caregiving expectations, your ability to afford the higher premiums, as well as other resources you can depend on such as your retirement income. If you would like to speak to an adviser to learn more about having enough to cater to your long-term care needs in retirement, we’ll be more than happy to help you make an informed decision.