Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

For MoneyOwl, we go for a high bar of reliability when we look for investment solutions for our client’s financial plans

Value and small caps, to which the Dimensional equity funds in MoneyOwl’s portfolios are tilted, have been massively outperforming for more than 6 months since the third quarter of 2020. From August 2020 to February 2021, MSCI World Value Index returned 16.1% vs 7.8% for the MSCI World Growth Index, while the MSCI World Small Cap index returned 29.9% vs 11.7% for the MSCI World Index (net of dividends, in USD).

As advisers who encourage taking a long-term view in investing, MoneyOwl would be the first to say that we should not make too much of our own short-term outperformance. We know that the value, small caps, and profitability premiums can hide for extended periods. The premiums are volatile, no doubt.

But what we can say is that when value, small caps (and profitability) premiums do appear, they can come back very strongly. They remind us that these dimensions of long-term, higher expected return stand on the solid ground of both evidence and logic – on the back of the Nobel prize-winning standard of research, no less!

You may ask, then, what makes value, small caps, and profitability each a long-term dimension of higher expected return, as opposed to just a short-term “market rotation”?

For MoneyOwl, we go for a high bar of reliability when we look for investment solutions for our client’s financial plans. This reliability must be:

- Grounded in financial logic

- Supported by evidence

- Assured by cost-effectiveness in implementation

The Logic Behind the Premiums

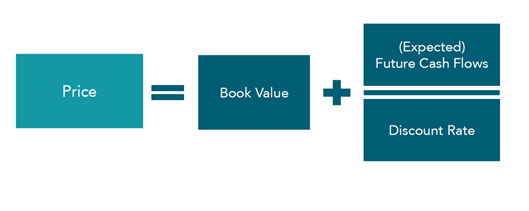

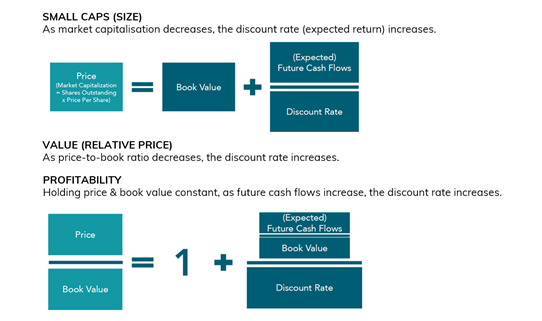

The logic behind the premiums is found in valuation theory. The Price of a security is its Book Value plus the Present Value of expected future cash flows discounted at a certain discount rate. This discount rate is also the expected return.

One way of understanding a discount rate is to see it as the opportunity cost of your capital – the rate of return from other opportunities at similar risk levels. For example, I expect to get an average of 5% p.a. return from investing in Company X’s peer competitors. I would thus discount the future cash flows of Company X one year out by 1.05, the cash flows two years out by 1.052, and so on. 5% is my discount rate.

Most market analysts will use an assumed discount rate (as I did in the simple example above) and try to find the intrinsic or “correct” price for the share. Thereafter, they find “underpriced” shares to buy and “overpriced” shares to sell. What I learned during my time as a strategist and analyst in an active fund house is that there are often many assumptions and even forecasts used in arriving at this discount rate. And a small change in this discount rate, built on many assumptions, can greatly affect the target price.

Dimensional’s approach, founded on the Nobel prize-winning thought of Eugene Fama about efficient markets and other world-class academics, is to treat the Price as “fair”. “Fair” does not mean correct, but it means that prices reflect the combined knowledge and expectations of millions of participants and adjust to them very quickly, such that we cannot reliably time the market or forecast prices.

With Price as a “fixed” starting point in the valuation equation, they then look for securities with a higher discount rate (also the expected return for the security). We can use the valuation equation and its rearrangements to illustrate the small cap, value, and profitability premiums.

Don’t worry if the above brings back bad memories of muscle-tensing Math homework. MoneyOwl’s clients are not left to a robo. We have a full team of more than a dozen full-time human advisers all on the internationally recognised Certified Financial Planner (CFP) programme giving real advice, to explain this to you and help you construct a financial plan.

The Evidence About The Premiums

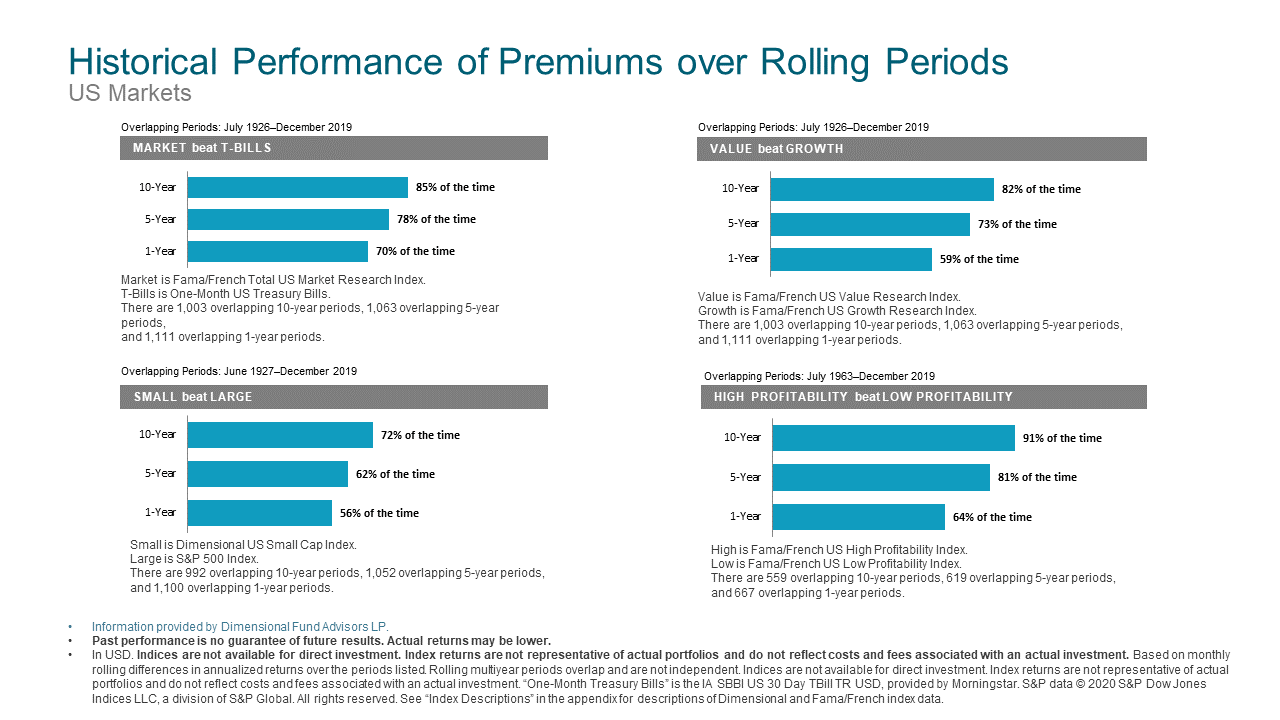

There is ample evidence that value, small caps, and profitability premiums, while volatile, are persistent over time, pervasive across geographies and sectors, and robust enough in terms of quantum. We have talked about this a lot, including in our most recent investing webinar. (Drop us an email if you wish to take a look at the recording.) Here is a snapshot from US markets. It is very similar to the larger global markets.

The Cost of Harvesting The Premiums

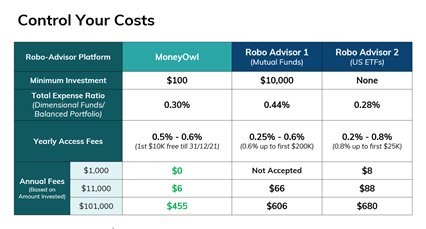

Finally, the premiums must be sensible and cost-effective to implement. Here, again, Dimensional funds have some of the lowest expense ratios of unit trusts in Singapore. Dimensional pays no trailer commissions (and MoneyOwl thus receives none) that bulk up expenses that eat into your fund performance. In addition, MoneyOwl has additionally chosen the “Core” funds among the suite of Dimensional funds to give you broad, globally diversified market exposure (to more than 8,000 securities in each portfolio) which are also the most inexpensive among Dimensional funds. Our portfolios’ blended expense ratios are currently 0.28%-0.32% p.a., and will fall further to 0.254% to 0.274% p.a. as Dimensional further lowers the expenses of some of their funds come May 2021. In terms of advisory fees, while we don’t aim to be cheap (we’re a full-fledged comprehensive financial advisory practice with real salaried advisers!), we are probably also one of the lowest cost ways to access Dimensional funds, especially for smaller investors.

It’s All About Sufficiency and Reliability

Investing is ultimately about getting the return you need, not the maximum return in any short-term time frame. Broad-based equity markets have been shown to reward investors with more than good enough long-term return that beats inflation and which is sufficient for most accumulation needs. Where we can, we would like to capture some additional returns to build a buffer for our nest egg. Dimensional funds have outperformed in recent times, but this is not the reason why you should invest in them through MoneyOwl. Rather, you invest in Dimensional funds because the reliability of your returns is most important for your goals. The logic and evidence upon which these funds are built and the sensible cost of investing combine to give us the assurance and comfort for sufficiency and reliability over the long term.

Disclaimer: While every reasonable care is taken to ensure the accuracy of information provided, no responsibility can be accepted for any loss or inconvenience caused by any error or omission. The ideas, suggestions, general principles, examples, and other information presented are for reference only and are not meant to be a substitute for professional investment advice. The information and opinions expressed herein are made in good faith and are based on sources believed to be reliable but no representation or warranty, express or implied, is made as to their accuracy, completeness, or correctness. Expressions of opinions or estimates should neither be relied upon nor used in any way as an indication of the future performance of any financial products, as prices of assets and currencies may go down as well as up and past performance should not be taken as an indication of future performance. The author and publisher shall have no liability for any loss or expense whatsoever relating to investment decisions made by the reader.