By Ernest Tham, Financial Planning Solutions Specialist

The number that intimidates people

If you’ve been following the BTO conversation online, you’ve probably seen the headlines. A 4-room flat in Tampines at $600,000. A 3-room flat in Redhill at $500,000.

Such prices have fuelled concerns about affordability and whether a BTO is still within reach. Take the June 2026 BTO exercise. A mid-floor 4-room at Berlayar Rise in Bukit Merah comes in at around $700,000 before grants. If you’re a couple earning a combined $6,000 a month, you’d be forgiven for looking at that large number and giving up before you even start.

Here’s what we’d say: don’t give up, but do adjust your expectations. Not because your situation is hopeless, but because the $700K flat is probably not the right flat for you, and that’s actually fine.

The flat everyone wants doesn’t exist

Scroll through enough property forums and you’ll sense a pattern – the dream first home is:

- Centrally located (near MRT, near town)

- Spacious (at least a 4-room)

- Affordable (priced like a non-mature estate)

That flat does not exist. It has never existed. And social media, which amplifies outrage over the most expensive launches while quietly ignoring the more affordable ones, has made many first-time buyers feel entitled to a combination of features that is very hard to find all at once.

For most first-time Singaporean homeowners, you can realistically pick two out of three.

The question isn’t: can I have it all? The question is: which two matter most to me right now, and which trade-off can I live with?

The trade-off: location, size, price

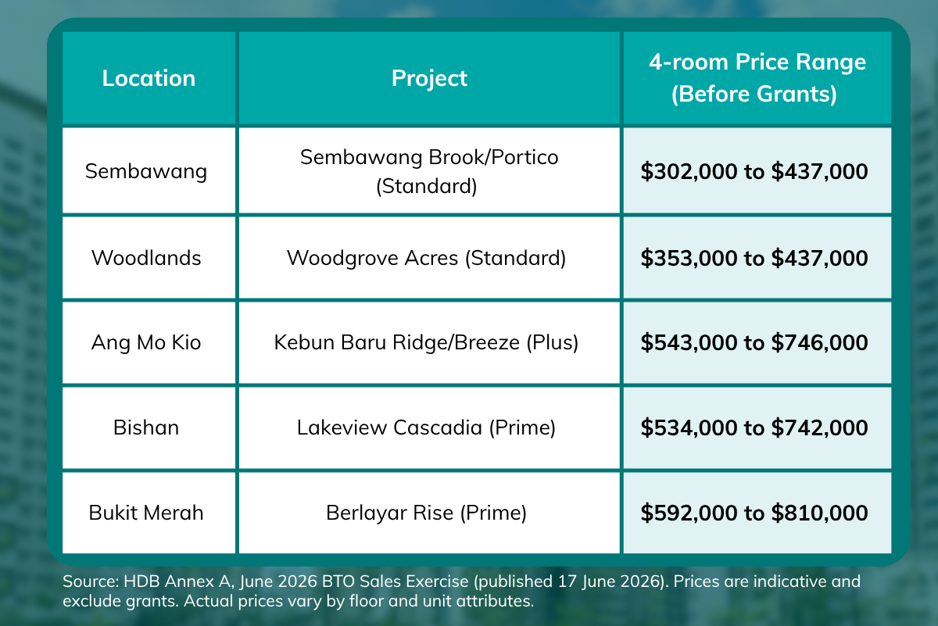

Every BTO purchase involves a genuine trade-off across three dimensions. Here’s what the June 2026 BTO exercise actually looks like, using 4-room flats as the baseline:

The flat in Sembawang gives you the size and the price, but you give up some convenience. The flat in Bukit Merah gives you the location and the size, but you pay significantly more upfront. Neither choice is wrong. They reflect different priorities.

One thing worth noting: Lakeview Cascadia in Bishan starts lower than the Ang Mo Kio Plus flats before grants, even though nearby resale flats in Bishan transact at $840,000 to $950,000. This is because Lakeview Cascadia is a Prime flat, and it carries a heavier government subsidy to bring the sticker price down. That subsidy comes with a 10-year Minimum Occupation Period and a clawback on resale. The sticker price is not the full picture.

So what can $6,000 a month actually get you?

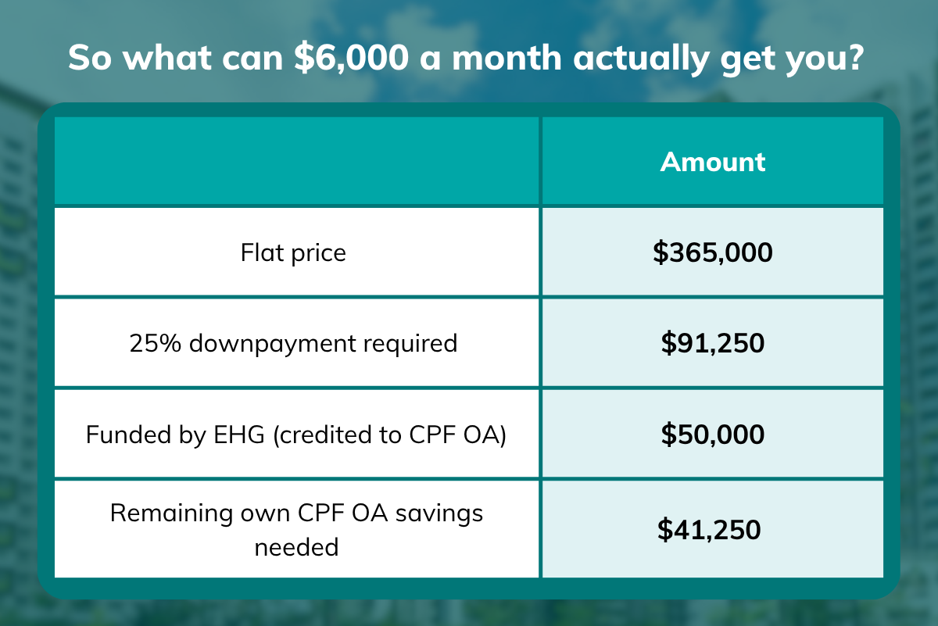

Let’s put some numbers to it. A couple who are Singapore Citizens, applying as first-timers with a combined income of $6,000 a month, would qualify for the Enhanced CPF Housing Grant (EHG). At that income level, the EHG works out to $50,000, credited directly into your CPF Ordinary Account.

Here is how the downpayment comes together on a Standard 4-room flat in Sembawang, using $365,000 as the midpoint of the Sembawang Brook price range. Lower-floor units would start from $302,000, making the maths even more favourable:

With an HDB concessionary loan, the 25% downpayment itself can be paid fully from CPF OA. The EHG contributes $50,000 of that immediately. The remaining $41,250 needs to come from your own CPF OA savings. At combined CPF OA contributions of roughly $1,380 a month for this couple, that takes around 2.5 to 3 years to accumulate from scratch, well within a typical BTO waiting time of 3 to 4 years.

That said, buying a flat is not entirely cash-free. You will need some cash for upfront costs like the option fee at flat selection and legal fees. These are relatively modest, but worth setting aside as part of your planning.

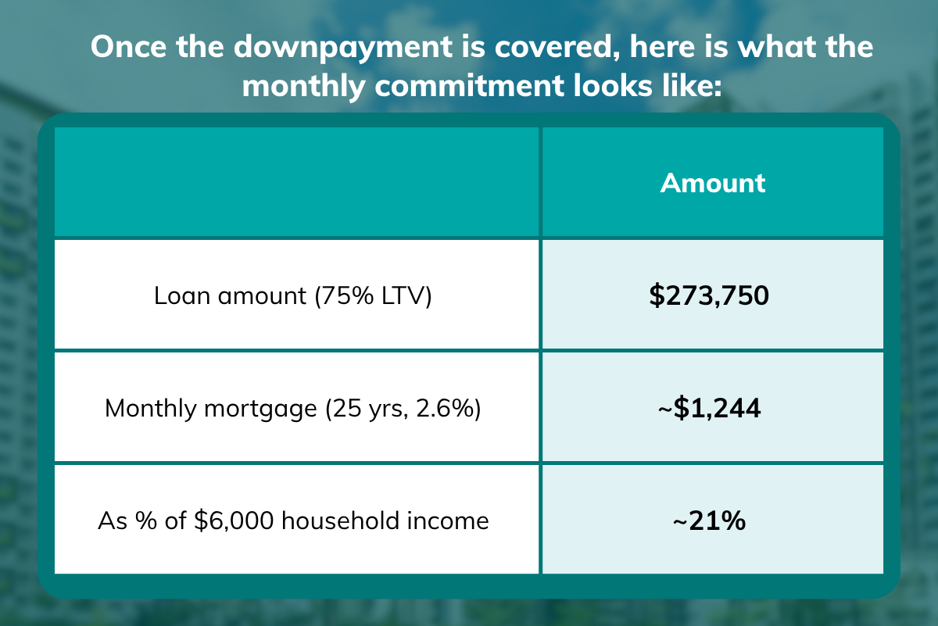

To put that in context: MAS sets a Mortgage Servicing Ratio (MSR) cap of 30% of gross monthly income for HDB flat purchases. At 21%, this couple is well inside that limit, with room to spare for daily expenses, insurance, savings, and the general unpredictability of life.

Buy what you can afford, not what you think you deserve

Whether you are buying a home you plan to stay in for life or one you might upgrade from later, the right principle is the same: buy within your means.

The risk is not in choosing a flat that is further from town.

The risk is in stretching for a more expensive flat because it feels like the “right” choice and then spending the next decade house-rich but cash-poor, with no buffer for emergencies, career changes, or children.

A home bought within your means is a stable foundation. One bought beyond your means becomes a source of chronic financial stress, regardless of the address.

This trade-off should not be seen as a consolation prize for people who cannot afford better. Rather, it offers a practical framework for making a deliberate and financially sound decision on your own terms. Before you do anything else, know your actual number

Most of the anxiety around BTO affordability comes from comparing your income to a headline price without accounting for the full picture: the grants you qualify for, CPF contributions that do the heavy lifting, and the loan structure that spreads the cost over time.

The number that matters is not $700,000. It is your monthly mortgage payment after grants, and whether it fits comfortably within your household income.

Use MoneyOwl’s HDB BTO Planner to work out what you can afford.

Based on your income, age, and CPF savings, our planner estimates your loan amount, monthly repayments, and more. Try it out here:

All BTO prices are from HDB Annex A, June 2026 BTO Sales Exercise (published 17 June 2026). EHG of $50,000 is based on the official HDB grant table (August 2024 revision, $5,501–$6,000 income bracket) for eligible first-timer Singapore Citizen households. EHG eligibility is subject to HDB assessment. Mortgage estimate uses HDB concessionary loan rate of 2.6% per annum over 25 years on a loan of $273,750, based on a $365,000 flat price at the midpoint of the Sembawang Brook 4-room range; lower-floor units start from $302,000. MSR limit of 30% sourced from MAS (mas.gov.sg). CPF OA contribution estimate assumes both applicants are aged 35 and below contributing at the prevailing CPF OA rate. Combined contribution figure assumes equal salaries of $3,000 each. Always verify current figures at hdb.gov.sg or via an HFE letter application.

Disclaimer: This material is provided for general information only and does not constitute financial advice, a recommendation, or an offer to buy or sell any financial product. While reasonable care has been taken to ensure accuracy, no representation or warranty is made as to the completeness or reliability of the information, and no responsibility can be accepted for any loss or inconvenience caused by any error or omission. Any opinions or estimates are subject to change and should not be relied upon as an indication of future performance. You should consider your own financial objectives, financial situation, and needs before making any financial decision. It is advisable to seek advice from a qualified financial adviser to assess your needs and understand the features, risks, and costs of any financial product before making a decision.

This publication has not been reviewed by the Monetary Authority of Singapore.