By Chuin Ting Weber, CFP, CFA, CAIA

CEO & CIO, MoneyOwl

Once upon a time, this was my job.

To guess what would happen to stocks and bonds, countries and sectors, after guessing what the Fed would do about interest rates.

Of course, this guess work was done with fancy tools and research resources, and written up nicely. (Investors pay for this through their fund management fees.)

Yesterday, on 18 Sep 2024, the Fed cut interest rates by 50 bps (0.50% p.a.), a larger cut than the 25 bps traders were predicting. The markets went up for a while, and then went down.

If you had asked traders and analysts a week earlier, quite a number would have said that the stocks would rally with a larger cut.

Explanations given for last night’s whipsaw action included: stocks were already too expensive. A bigger cut means a poor economy, which means it is bad for companies and their stock prices. The Fed Chair said it might not cut more.

I wonder what would be written if the stock market “decided” to recover tonight. Probably equally extremely logical explanations based on economy and market analysis.

It’s hard trying to predict market movements based on the Fed

A lot of energy and money is lost trying to figure out what is the “right” thing for markets to do, on the assumption that markets would get there eventually.

So, if you figure it out better than others, you can get ahead. If you time your buys and sells, you can make more money.

Unfortunately, this is really hard to do.

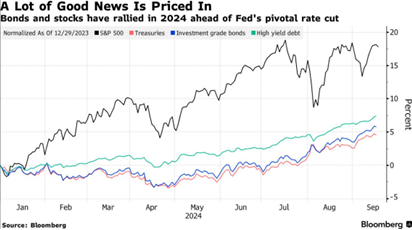

Markets move quickly. They do the “pricing in” quickly, but what is missing from this Bloomberg chart below is that it’s much more than the Fed cuts that markets price in.

Markets incorporate all kinds of data and expectations – both hard, objective data and subjective factors like expectations and feelings – of millions of people.

The only thing we can say for sure when stock prices go up, is that more is being bought than sold. And when stocks go down, that there are more sells than buys.

And how can one know who would buy or sell how much and why, and collect this all ahead of time, every time?

Use the information for your short-term planning instead

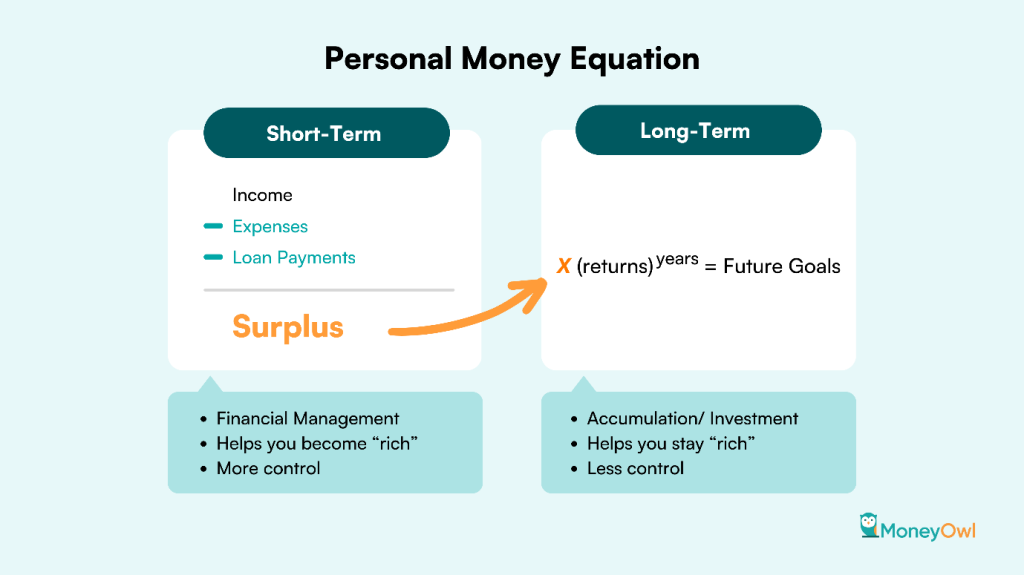

What’s more relevant when listening to the Fed is to use the information to help you make shorter-term financial planning decisions – things under your control – on the left side of your personal money equation:

For example, the larger Fed cut might be good news for your mortgage rate, if you are looking to refinance, as there is a knock-on impact from what happens in the US to what happens in Singapore.

The Fed’s objective to engineer a soft landing is also about a weakening jobs market in the US. While the implication for Singapore may not be obvious, as the job market remains robust, other news in Singapore about slowing employment growth and retrenched workers taking longer to find new jobs, might give us pause for how we build an emergency fund. Plus the wider action that we should always be upskilling and improving our ability to safeguard and earn more income, which is the basis for our building of wealth.

There’s never a best time, but it’s always a good time

For quite a couple of years now, holding cash and T-bills have been popular because of higher interest rates.

But if stocks are suitable for you, I hope your adviser did not advise you to switch over to cash. That’s also market timing, which hurts you in the long term.

Look at the same Bloomberg chart. If you had been in stocks, you would have been up double digit per cent this year and more than that, over a longer time frame.

Now that the Fed has finally cut rates, there might, belatedly, come the advice to buy something else. It’s better late than never.

But the temptation is to look at the stock market and think it is “too high”.

My challenge to friends who tell me that the stock market is too high is to ask, at what level would you buy, then? If markets fell by 10%, would you say that you are catching a falling knife, and it is too early? If the stock market was down by 20%, would you go in?

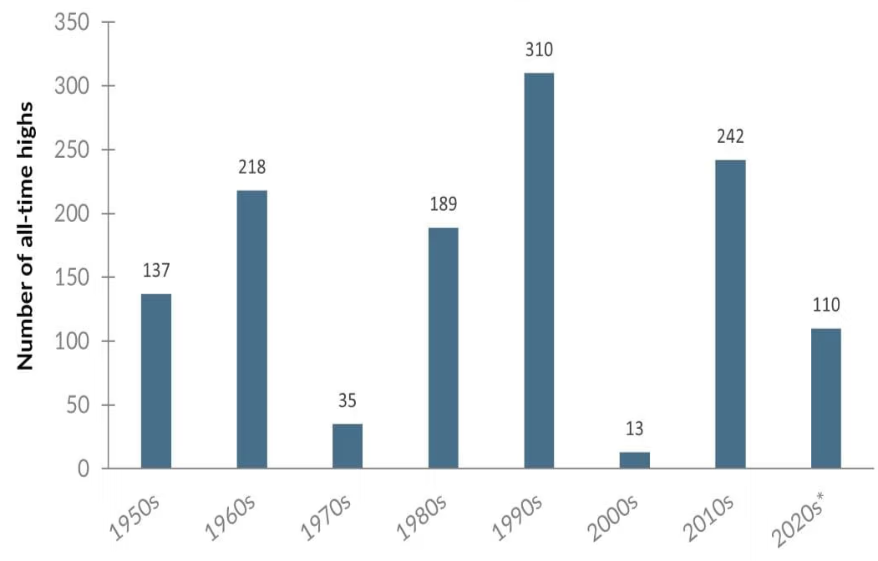

The evidence is that stock markets do have a good chance of going higher each time they hit new highs. There are many, many all-time highs.

And over the long term, we know that stock markets will go up

The people who lose out are those who wait and miss out on the big runs, compounded. Stocks are one of the most powerful engines to beat inflation over the long term. Cash is one of the worst.

The conclusion:

Leave guess work and stress to people who get paid to run after the wind. But try not to be the one paying for guesswork through high-cost active management fees.

Consider instead, making it a habit to invest regularly in the broad market through a low-cost, global indexed fund, then stay invested and ride through the volatility, while strengthening your financial health in the short term through better income-outflow management.

Let time and markets do their thing for you, while you live your life.

Subscribe here for our soon-to-come and free monthly OwlHoots on financial planning insights and analysis.

Disclaimer:

While every reasonable care is taken to ensure the accuracy of the information provided, no responsibility can be accepted for any loss or inconvenience caused by any error or omission. The information and opinions expressed herein are made in good faith and are based on sources believed to be reliable but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. All investments carry risk. Expressions of opinions or estimates should neither be relied upon nor used in any way as an indication of the future performance of any financial products, as prices of assets and currencies may go down as well as up and past performance should not be taken as an indication of future performance. The author and publisher shall have no liability for any loss or expense whatsoever relating to investment decisions made by the reader. This publication has not been reviewed by the Monetary Authority of Singapore