Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

In our previous article, we discussed how CPF LIFE

payouts form a good Safe Retirement Income Floor. For some Merdeka generation

retirees, however, you may feel that the payouts from CPF are less than what you

wish to have for your lifestyle. If so, you can build on top of your Safe

Retirement Income Floor, by investing in financial instruments, to fulfil the

Second Must-Have in Retirement: a monthly income for daily expenses.

In this article, we share strategies a Merdeka

Generation senior can employ in building this second layer of retirement income.

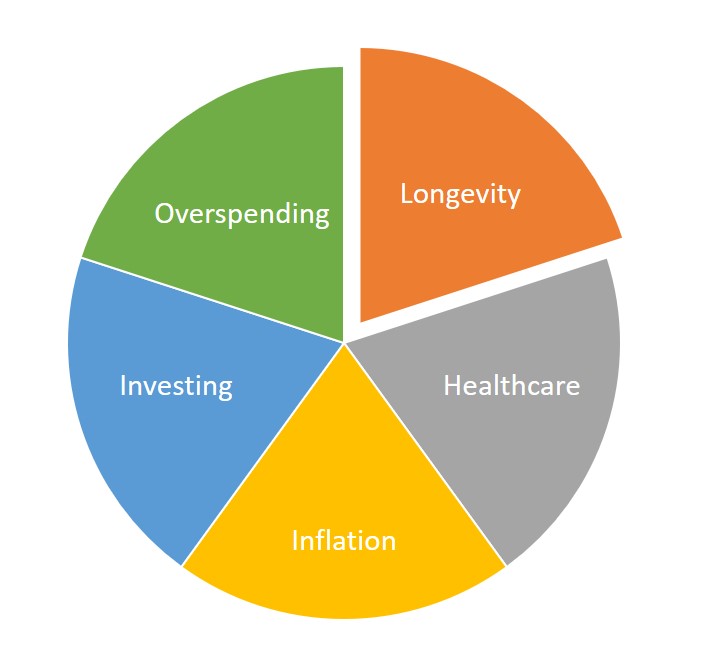

The 5 risks faced by

retirees

Retirement planning for retirees is more

complicated than for accumulators because of the combination of 5 risks that retirees

need to deal with:

- Longevity risk –

living too long - Inflation risk – things becoming more expensive

- Investing risk – assets value rise and fall

- Over-spending risk – unsustainable spending

- Healthcare risk – huge

medical expenses

Retiree’s Five Risks

The combination of these risks poses a conundrum

for retirees. While an annuity like CPF LIFE takes care of longevity risk to

some extent, rising costs (inflation risk) mean that a much bigger retirement

fund is required to maintain your current standard of living. Leaving your

money in the bank to earn fixed deposit interest rates is unlikely to support

your retirement spending and hence there is a need to invest for higher returns

on your savings. However, investing carries risk (investing risk) and too much

volatility on your investment might become uncomfortable for retirees to

accept. At the same time, if left unchecked, excessive spending (over-spending

risk) especially in the early years of retirement could deplete their savings

faster. Finally, as we age, our medical cost (healthcare risk) increases and

this will put further strain on the retirement funds.

A good retirement plan needs to try and reconcile these 5 risks for the retiree. Here are some instruments you can consider using to build an additional layer of retirement income, on top of CPF payouts:

1. Invest in suitable low-cost, well-diversified, market-based portfolios to stretch your savings, while setting withdrawal rules

Contrary to popular

intuition, you can still invest in markets during your retirement years. Your

investment decision should be a combination of the need to take risk (what return you need), your ability to take risk and your willingness

to do so.

The need to take risk

includes your need for income and your need to overcome longevity and inflation

risks. As for your ability to take risk, consider your financial situation, such

as whether you have an emergency fund and the time horizons that are relevant

to you. Given that an average retirement can span 15 to 20 years today, you

certainly have the time horizon to invest at least a portion of your savings

that you do not immediately need. However, you need to be willing to accept

some volatility because staying invested is key to capturing market return.

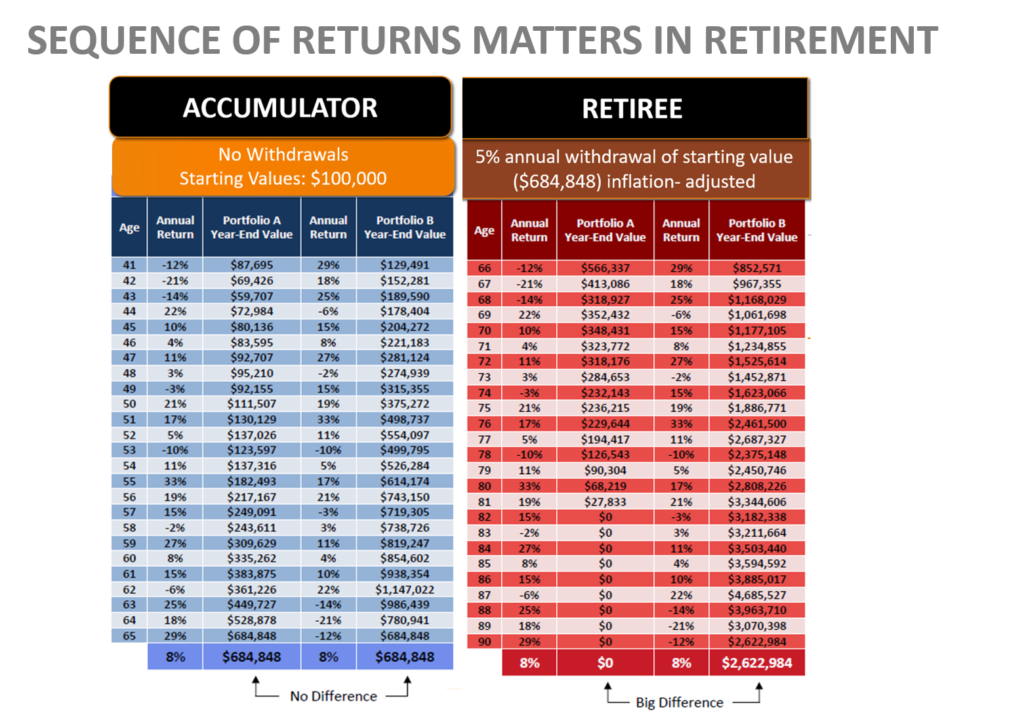

Unless you have a large enough pool of capital to

be able to spend only the return, you should also set a retirement withdrawal

rule at between 2.5% to 4.0% of initial invested capital, to help mitigate the

negative impact of sequence of returns risk in investing. This is the risk of experiencing

negative market returns at the beginning of your drawdown, such that you would

deplete your capital base quickly if you are drawing down a fixed amount (or an

amount that is adjusted for inflation yearly), compared to a situation in which

the returns are positive at the start of your drawdown period. Alternatively,

you can bucket your investments according to different time horizons and invest

later “buckets” into higher risk portfolios and earlier “buckets” into low-risk

instruments.

MoneyOwl will soon be launching our own suite of low-cost, well-diversified and market-based portfolios that do not try to time the market based on forecasts or other techniques. Costs matter because they impact return, while the disciplines of diversification and avoiding going in and out of market are important if an investor is to capture market return.

2. Consider Retirement Income products

For those who prefer not to make portfolio

investments, you may wish to consider retirement income products offered by

local insurers. When CPF LIFE was introduced, it effectively killed off the private

annuities market as it was close to impossible to match the returns, all else

being equal. Nevertheless, the insurance companies have reinvented this product

range as retirement income products which now offer themselves as a complement

to CPF LIFE, especially if you have already hit the CPF top-up limit.

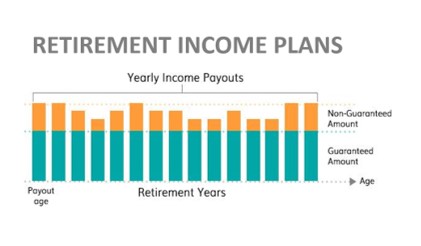

Retirement income plans provide a monthly payout

over a fixed period. The payout comprises both a guaranteed and non-guaranteed

portion depending on the performance of the underlying fund. It is important to

take note that a portion of the return is not guaranteed. Compared to portfolio

investments, Retirement income products generally present less visible

volatility as the payouts depend on the insurer’s ability to make the different

threshold of investment returns in the insurance fund. In terms of

disadvantages, you may find the capital outlay large relative to the return.

To compare the different retirement income plans in the market, try MoneyOwl’s Insurance Robo.

3. Park your liquid funds in Singapore Savings Bonds (SSBs)

Singapore Savings Bonds

are more savings than investment instruments. For

retirees (or anyone, actually), they can be a very good place to park your

liquid funds. They are flexible alternatives to fixed deposit accounts, but

without penalty for redemption. These bonds are backed by the Singapore

government and principal is guaranteed.

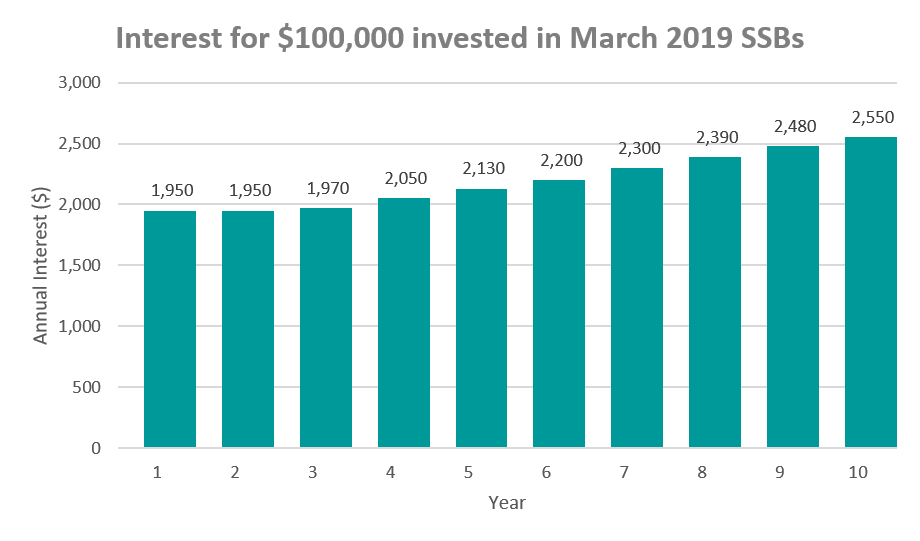

The SSB has a full tenure of 10 years and its interest

is tied to that of Singapore Government Securities (SGS). You get a coupon

every 6 months. You receive less interest at the start, but the interest steps

up over time. The coupons and effective interest rates you will receive are all

announced prior to your investment. If you hold your SSB for the full 10 years,

your return will match the average 10-year SGS yield the month before your

investment.

The difference between SSBs and SGS is that you have the flexibility to redeem the bond at any time, with a maximum waiting period of one month, without price risks. You always get back your full principal even if you sell before the 10 years is up. In this regard, SSBs are unlike Singapore Government Securities (SGS), which have to be sold on the secondary market if you want to redeem them early. The price at which you can sell the SGS is dependent on market factors. If the interest on newer issues of SGS has gone up, buyers will ask for a lower price to compensate for the opportunity cost. If market forces move the other way, the price of SGS can go up as well. Not so for SSBs. You get back what you invested, no more, no less, and of course you keep the coupons you have already clipped. In terms of overall return, an investor who holds an SSB for a given number of years would have an average return similar to that of an SGS of the same tenor. You even know what this return is ahead of time!

SSBs deal with the risk of investing loss (given

that they are not really a traditional investment), but not inflation or other

risks faced by retirees. They can complement your retirement plan in two ways. The

first is to receive the coupons, but these are not high. The coupon rate for

March 2019 issues are 1.95% in the first 12 months and step up to 2.55% for a

10-year period. Assuming you

buy into $100,000 worth of these SSBs and hold it till maturity, you can expect

to receive an average of just under $1,100 in coupons every 6 months. The

second way is to draw down your SSBs by redeeming them gradually over set time intervals

or when you have unforeseen emergencies.

You can buy SSBs

through one of our three local banks – DBS/POSB, OCBC or UOB, via the ATM or

internet banking. You will need either a CDP account or an SRS account and

there is an administrative charge of $2 per application. The minimum investment

amount is $500, capped at a maximum holding level of $200,000. In months when

the SSBs are oversubscribed, you may not get your full allocation.

Other sources of income

In an earlier article,

we had talked about monetising your home for additional income in retirement.

In the event of severe disability in retirement, there may be payouts from ElderShield

or the upcoming CareShield Life to help in long-term care expenses, in addition

to what you may have from CPF LIFE/ Retirement Sum Scheme and investments. We

will cover this in our next article.

The saying goes that the journey of

thousand miles begins with a single step. So does a 20, 25 or 30-year

retirement. We’ve listed down several ways you can supplement your income for a

more secure and purposeful retirement. We hope you are encouraged to take them.

Stay tuned for the next part in our series where we will discuss healthcare risk and our Third Must-Have in Retirement: a Medical Safety Net.

MoneyOwl is Singapore’s 1st bionic financial adviser. To find out more about us, visit www.moneyowl.com.sg