By Daphne Lye, CFP®

Senior Lead, Solutions, Research & Investment, MoneyOwl

Introduction

Singapore is one of the fastest ageing societies in the world. By 2030, one in four Singaporeans will be aged 65 and above.

When planning for retirement, it is important to factor in long-term care costs if one becomes severely disabled in old age.

The reality is sobering: nearly one in two healthy Singaporeans aged 65 today is expected to experience severe disability in their lifetime1, which will require assistance with daily activities for years.

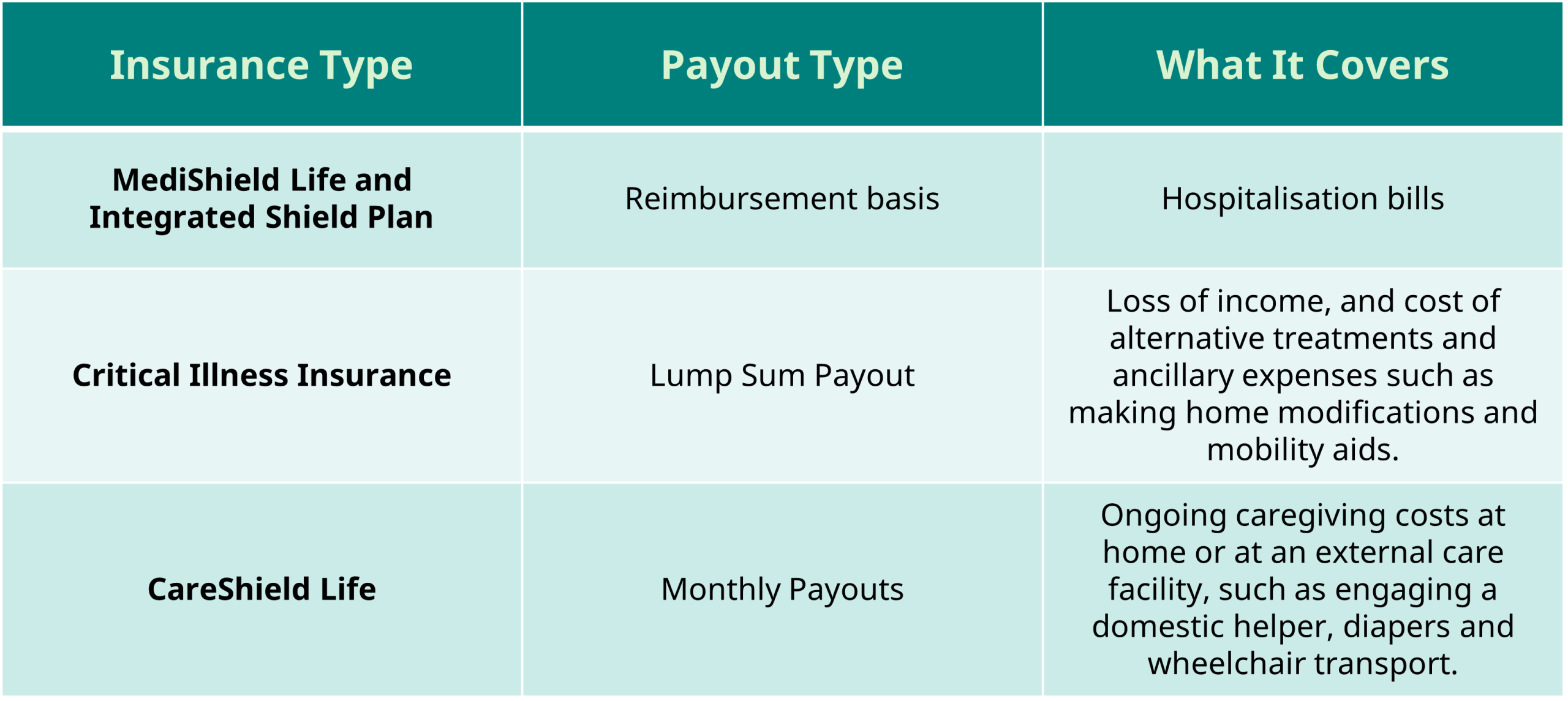

What is CareShield Life?

To mitigate concerns of long-term care costs, CareShield Life is a national scheme that provides monthly cash payouts in the event of severe disability.

Severe disability is defined as the inability to perform at least three out of six Activities of Daily Living (ADLs) — namely washing, dressing, feeding, toileting, walking or moving around, and transferring (such as from bed to chair).

When severe disability hits, monthly payouts from CareShield Life can help support ongoing care needs such as hiring a caregiver, paying for community care, or making adjustments to the home environment.

Before the 2026 changes to CareShield Life, monthly payouts grew by 2% each year until age 67, starting from the base amount of $600 per month in 2020.

Those who made claims from 2025 would have received $662 per month.

Once a claim was made, the individual would continue receiving the payout level applicable in the year they claimed for, as long as they remain in severe disability. Premiums for CareShield Life can be fully paid using MediSave, with additional subsidies for lower- and middle-income households.

All Singapore Citizens and Permanent Residents born in 1980 or later are automatically covered under CareShield Life once they turn 30, regardless of pre-existing medical conditions or disability status. For those born in 1979 or earlier, they can choose to opt in to CareShield Life

CareShield Life enhancements from January 2026

With rapidly rising costs of long-term care costs, CareShield Life will be enhanced from January 2026:

- Faster Payout Growth

Currently, CareShield Life payouts grow by 2% annually until age 67 or when a successful claim is made.

From 2026, payouts will increase at a faster rate of 4% p.a., ensuring that benefits can better keep pace with inflation and care costs.

This means that one making a CareShield Life claim in 2030 will receive $806 per month, compared to $731 per month under the current annual growth rate. This provides a higher level of basic long-term care protection.

- Greater Premium Support

With higher payouts, premiums will increase too.

To help Singaporeans cope with the premium increases, Government will provide support such that the annual premium increases between 2026 and 2030 will be about $38 on average, and no more than $75. Low- to middle-income Singaporeans will see even lower premium increases, as they will continue to receive means-tested premium subsidies.

- Adjust underwriting criteria for older individuals

As a limited time measure since the launch of CareShield Life, individuals born in 1979 or earlier with mild and moderate disabilities could still enrol in the scheme.

Enrolment rules for CareShield Life will tighten from 2026, reinstating the underwriting criteria as planned. Only older individuals without pre-existing disabilities will be able to enrol in the scheme.

How do the CareShield Life changes affect me?

For individuals and families, it is important to understand how CareShield Life integrates with retirement savings, CPF LIFE payouts, and other forms of insurance to build resilience against life’s uncertainties.

For example, if you suffer from a stroke and are severely disabled, CareShield Life payouts come in to provide monthly payouts during your disability period to offset the costs of caregiving, alongside other insurance claims and payouts:

A higher amount of CareShield Life monthly payouts can better keep pace with inflation and care needs after you are discharged. It gives you more assurance in retirement planning and reduces financial stress on your loved ones.

Indicative bill examples of community care facility and a nursing home are about $2,700 and $4,900 a month respectively. After Government subsidies and CareShield Life payouts, the monthly out-of-pocket costs could come up to about $100 and $500 for a community care facility or nursing home2 respectively.

These costs can be paid from one’s savings, or by tapping on other Government schemes including:

- MediSave Care – Allows those with severe disabilities to withdraw up to $200 monthly from their MediSave

- Home Caregiving Grant – Monthly payouts of up to $400 (or up to $600 from April 2026)

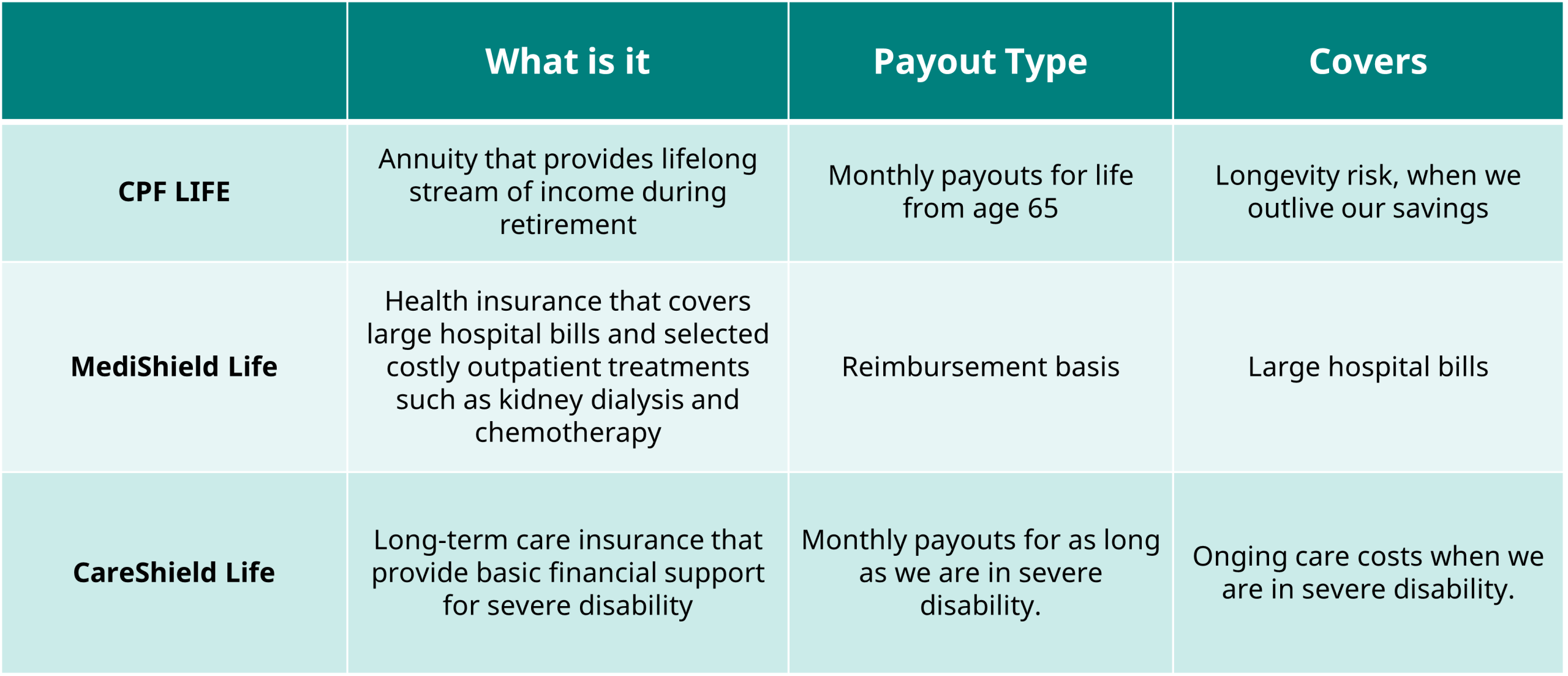

CareShield Life is a key pillar in safeguarding retirement adequacy.

Besides saving up for a nest egg and having adequate insurance for medical bills, we must also plan for the possibility of needing daily living assistance especially in our older ages. Without adequate long-term care coverage, we may have to deplete our retirement savings or over-rely on our family.

Together, the three national ‘Life’ schemes provide a strong foundation of protection in our silver years when illness and severe disability is more likely to happen.

Should I get a CareShield Life supplement?

To address residual or unexpected expenses, you may be considering a private CareShield Life supplement to enjoy more benefits such as higher monthly payouts, additional lump sum payouts, and more relaxed criteria such as being able to claim from being unable to perform one instead of three ADLs.

MoneyOwl’s advice is to balance comprehensiveness and cost. We need to consider whether the additional premiums, part of which may need to be paid by cash, remains affordable even as we are older.

We can also consider our situation in retirement and whether we need higher payouts from CareShield Life supplements. Think about caregiving capacity within the family, living arrangements, as well as sources of retirement income. Together, these can help decide whether CareShield Life’s baseline payouts are sufficient.

An alternative to purchasing CareShield Life supplements is to save and invest the equivalent premium amount that gives us more flexibility on how to use the nest egg that is not limited to long-term care. If you are risk adverse, you can also consider topping up your CPF Special or Retirement Account for higher monthly payouts in retirement, which can also be used to pay for long-term care costs if needed.

Conclusion

As more Singaporeans live longer, the risk of severe disability grows, and with it, the demand for sustainable and dignified long-term care.

The enhancements to CareShield Life, supported by additional government subsidies, help strengthen the safety net for Singaporeans. They provide greater assurance that if severe disability strikes, financial support will be available to ease the burden of care.

Planning for long-term care is not just about money — it is also about peace of mind. Knowing that you have structured your finances to handle the unexpected allows you and your family to focus on care and recovery.

- Source: Ministry of Health Singapore. ↩︎

- Source: MOH news release. Based on aged 56 or below in 2026 with severe disability, with a Per Capita Household Income of $1,500 ↩︎

Disclaimer:

The information contained herein does not have any regard to the specific investment objective(s), financial situation, or the particular needs of any person. Buying insurance is a long-term commitment and should be bought according to your needs, and products’ suitability.

It is advisable to seek advice from a financial adviser to assess your needs and guide you on the features and details of the products before making any financial decisions.

This article has not been reviewed by the Monetary Authority of Singapore.