Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

CPF forms the foundation for most Singaporeans’ retirement and helps to fund different aspects of our lives, such as providing us with retirement income, and helping to pay for our housing, and with our healthcare costs.

To help us grow our savings in a risk-free way, CPF pays interest to the following accounts:

| Name | Ordinary Account (OA) | Special Account (SA) | MediSave Account (MA) | Retirement Account (RA) |

|---|---|---|---|---|

| Base Interest (p.a.) | 2.5% | 4% | 4% | 4% |

| Purpose | Primarily for housing | For our retirement | For our medical needs | Provides retirement payouts |

In addition, to further boost our CPF savings, the Government pays extra interest on the first $60,000 of our CPF balances, with older members receiving more:

- If you are below age 55, you will earn an extra 1% p.a., or up to 5% p.a., on the first $60,000 of your combined CPF balances, capped at $20,000 for the Ordinary Account.

- If you are 55 or above, you will earn an extra 2% p.a., or up to 6% p.a., on the first $30,000 of your combined CPF balances, capped at $20,000 for the Ordinary Account. You will also continue to earn an extra 1% p.a., or up to 5% p.a., on the next $30,000 of your CPF savings.

If you are willing to take some risks, you can also choose to invest your CPF savings to earn potentially higher returns under the CPF Investment Scheme (CPFIS).

What is the CPF Investment Scheme about?

According to the CPF Board Annual Report 2021, over $20 billion of CPF savings had been invested by close to 1 million CPF members as of end 2021.

Anyone above age 18 can invest their CPF savings if they meet the following criteria:

- Are not a discharged bankrupt;

- Have more than $20,000 in your Ordinary Account, and/or more than $40,000 in your Special Account;

- Completed the CPFIS Self-Awareness Questionnaire (SAQ) (applicable to those new to CPF investing as of 1 October 2018).

The amount of CPF savings you can invest is:

- CPF Ordinary Account: Any amount above the first $20,000

- CPF Special Account: Any amount above the first $40,000

Tip 1: Before you invest your Ordinary Account savings, you should ensure that the savings are in excess of what you need for housing payments, including an emergency mortgage-payment buffer should you not receive an income for about 6 months.

Tip 2: We do not advocate investing one’s Special Account savings as the risk-free rate of up to 5% is hard to beat. And if you are risk-averse, you can also consider transferring your excess Ordinary Account savings to the Special Account to earn higher risk-free interest.

You’ll also need to consider the fees and charges1 incurred when you invest your CPF savings. In addition to the one-off transaction fees, a fee unique to CPFIS is the charges by agent banks, which comes up to about $2 per counter per quarter.

Tip 3: Due to the transaction fees in addition to the quarterly service fees payable to agent banks under the CPFIS, we do not recommend frequent transactions if they are of small quantum. Any regular monthly investments should be at least $200 for it to be worthwhile.

What can I invest my CPF savings in?

There is a wide range of investment products in which you can invest your CPF savings, which include:

| Invest with your | ||

|---|---|---|

| Investment products | Ordinary Account Savings | Special Account Savings |

| Unit Trusts | Yes | Yes, selected. |

| Investment-Linked Insurance Products | Yes | Yes, selected. |

| Annuities | Yes | Yes |

| Endowment Policies | Yes | Yes |

| Singapore Government Bonds | Yes | Yes |

| Treasury Bills | Yes | Yes |

| Exchange-Traded Funds | Yes | None currently available |

| Fund Management Accounts | Yes | No |

| Fixed Deposits | Yes | Yes |

There are also selected investment options which only a portion of your CPF Ordinary Account investible savings – amount of CPF savings above the first $20,000 – can be used:

Up to 35% of investible savings

| Investment products | Invest with your Ordinary Account Savings |

|---|---|

| Shares | Yes |

| Property Funds | Yes |

| Corporate Bonds | Yes |

Furthermore, up to 10% of your CPF Ordinary Account investible savings can be invested in:

| Investment products | Invest with your Ordinary Account Savings |

|---|---|

| Gold ETFs | Yes |

| Other Gold Products | Yes |

Investing your CPF for reliable returns

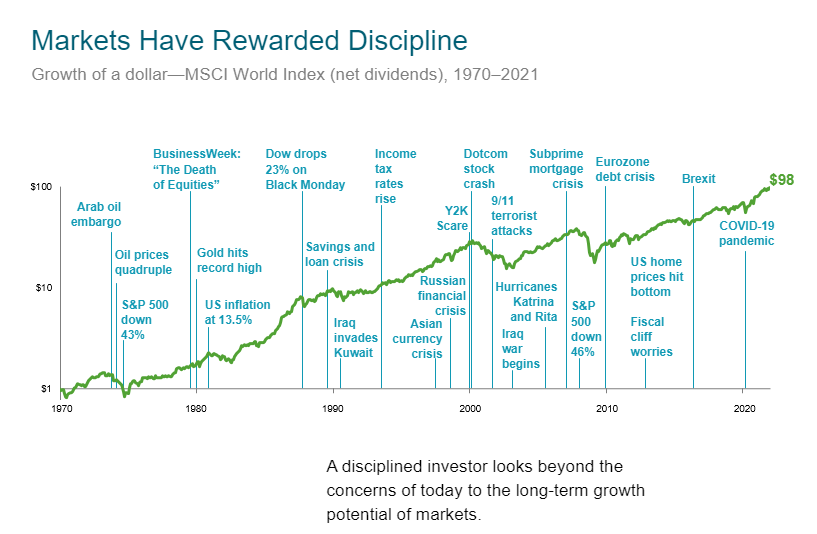

If you are new to, or unfamiliar to investing, you may not know where to start investing your CPF savings. You could worry if the timing is right for you to enter the market, fear of choosing the wrong company or fund, or experience anxiety if the next global financial crisis is impending.

The good news is that if you invest in a broadly diversified fund, are able to hold your investment for about 10 years or more, and choose a low-cost fund, you have a good chance of doing better than the 2.5% return given by CPF.

This is because despite the short-term volatility, the market generally goes up over the long-term. And when you are able to keep the cost of investment low, you can keep more of the returns from your investment.

Tip 4: When considering what to invest their CPF savings in, one should consider investing in a broadly diversified fund to reduce unsystematic risks. It is also important to take a long-term view when investing and resist reacting to short-term fluctuations in the market.

Tip 5: Those who have a sufficiently long time horizon of at least 10 years and are able and willing to stay invested through mid to high-level short-term volatility can consider investing a portion of their CPF OA savings to earn potentially higher returns.

Investing your CPF savings with MoneyOwl

A year ago, MoneyOwl launched our CPFIS portfolios to grow your money in using time-tested strategies and without guesswork. We partnered with Lion Global Investors and UOB Asset Management to offer adviser retrocession-free share classes for two funds that make up the CPF portfolios. This means that there are no hidden trailer commissions to advisers, and investors immediately enjoy lower fees. Investors do not need to manage troublesome trailer fee rebates, which are ultimately subject to an advisory firm’s business strategy. The two funds are:

- Lion Global Infinity Global Stock Index Fund share class C, a unit trust that feeds into a passive Vanguard fund tracking the MSCI World Index (representing equities); and

- United SGD Fund shares class D, a short-duration global bond fund (representing bonds).

We offer three portfolios with differing allocations of equities and bonds. In general, bonds are safer and more stable, while stocks are more volatile and have larger price movements. If you hold a smaller proportion of stocks, you may feel better when markets go down, but you have to balance that with feeling like you are missing out during times when the markets go up.

| Name | Allocation to: | Annualised historical return | Annualised Std Dev | Total Expense Ratio | |

|---|---|---|---|---|---|

| Equities | Bonds | ||||

| CPF Equity | 100% | 0% | 5.19% | 12.70% | 0.42% |

| CPF Growth | 80% | 20% | 5.03% | 10.29% | 0.41% |

| CPF Balanced | 60% | 40% | 4.81% | 7.89% | 0.40% |

The table above shows the annualised historical returns of our CPF portfolios comprising of Lion Global Infinity Global Stock Index Fund (Equities) and UOBAM United SGD Fund (Bonds). Based on the 15-year rolling return from Feb 2004 to Dec 2021, adjusted for the impact of retrocessions.

Conclusion

When you choose to invest your CPF with MoneyOwl, you will be able to manage your entire investment portfolio on a single platform – including your cash and Supplementary Retirement Scheme (SRS) savings. You can easily monitor your investment performance and keep track of your portfolios’ progress.

You can also get access to holistic and unbiased advice from our Client Advisers on your CPF investment options depending on your needs. While CPF investment has its advantages, but it may not be the right option for everyone.

[1] https://www.cpf.gov.sg/content/dam/web/member/faq/documents/INV_AnnexD.pdf

Disclaimer:

While every reasonable care is taken to ensure the accuracy of information provided, no responsibility can be accepted for any loss or inconvenience caused by any error or omission. The information and opinions expressed herein are made in good faith and are based on sources believed to be reliable but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Expressions of opinions or estimates should neither be relied upon nor used in any way as indication of the future performance of any financial products, as prices of assets and currencies may go down as well as up and past performance should not be taken as indication of future performance. All investments carry risk. The author and publisher shall have no liability for any loss or expense whatsoever relating to investment decisions made by the reader.