Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

In this fifth article, we will talk about the third Must-Have for Retirement – a strong healthcare safety net that takes care of your healthcare needs.

Ageing is inescapable and as we age, our body’s healing ability declines significantly, especially in the silver years. We become more susceptible to illnesses and injuries which may eventually lead to some forms of disability. The Ministry of Health (MOH) estimated that one in two healthy Singaporeans age 65 could become severely disabled in their lifetime and may need long-term care. Furthermore, 3 in 10 severely disabled persons remain disabled for 10 years or more. With rising medical costs and longer life expectancy, it is no wonder that

The cost of healthcare can come from 3 areas;

- Outpatient treatments

- Hospitalisation

- Long-term care

Retirees should have a strong medical safety net in the form of savings and medical insurance that can support their healthcare needs without compromising their standard of living.

With the generous benefits under the Merdeka Generation Package, Merdeka Generation seniors can now be more assured of their healthcare funding. Let us look at how Merdeka Generation seniors can manage their healthcare funding in the following areas.

First Safety Net – Outpatient Treatments

These are treatments for common ailments (e.g. cough and colds), dental care as well as chronic conditions like hypertension and diabetes. The cost of treatment at GPs or even specialist clinics are generally manageable but the on-going follow-ups for chronic conditions can be a burden.

There are affordable options. Pioneer Generation (PG) and Singaporeans with low to middle-income can enjoy subsidies at clinics participating in the Community Health Assist Scheme (CHAS). With Budget 2019, this scheme is now extended to all Merdeka Generation Singaporeans regardless of income:

- Special CHAS subsidies at CHAS GP and dental clinics, which are higher than CHAS Blue subsidies (the more subsidised of the two CHAS tiers, for persons whose per capital household income is <=$1,100 and living in HDB flats) but lower than CHAS for Pioneer Generation; and

- Extra 25% off the subsidised bill at polyclinics and public specialist outpatient clinics.

With this as a reference, the Merdeka Generation seniors might be able to enjoy outpatient benefits, such as:

- Treatment for common illnesses at GPs could enjoy a subsidy of somewhere between $18.50 to $28.50 per visit.

- Simple outpatient consultation for chronic conditions (such as diabetes, hypertension) could enjoy a subsidy of somewhere between $80 to $90 per visit, up to a cap of $320 to $360 per year.

With these subsidies, outpatient treatments for the Merdeka Generation become more affordable and with many clinics participating in CHAS, it is not difficult to find one nearby.

Second Safety Net – Hospitalisation

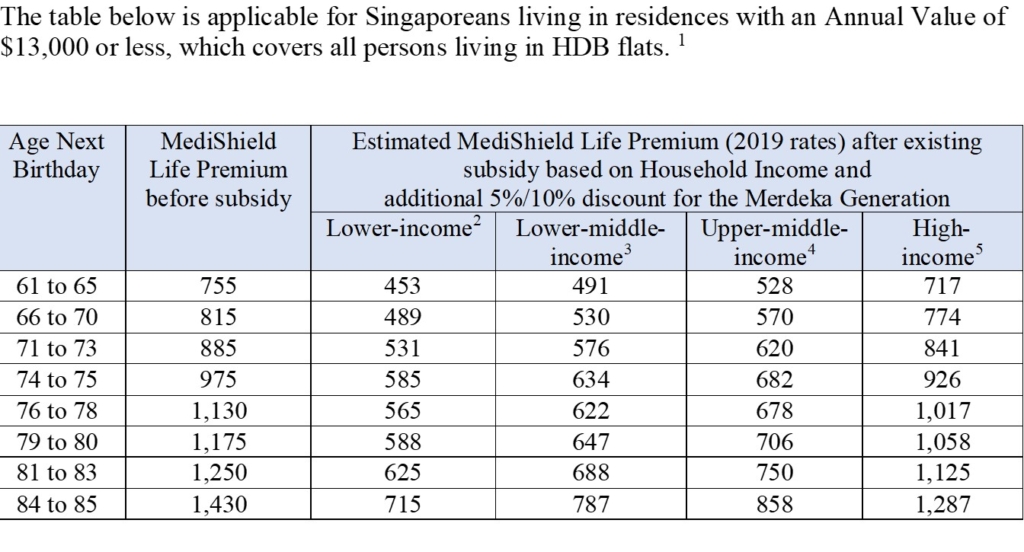

This is a key area where huge healthcare costs can arise. Big hospital bills pose a serious strain on retirement savings. Fortunately, every Singaporean and Permanent Resident is now covered under the compulsory MediShield Life scheme, which helps to defray the cost of huge medical bills at restructured hospitals for B2/C wards and selected outpatient treatments such as dialysis and chemotherapy for cancer.

MediShield Life is a good and affordable medical safety net and Merdeka Generation seniors can look forward to these benefits to help pay for the premium.

- Extra 5% discount on MediShield Life premium will be given and this will increase to 10% when a Merdeka Generation senior turns 75.

- MediSave top-up of $200 per year from now till 2023.

The amount of subsidy the Merdeka Generation gets depends on their citizenship (Singaporean or Permanent Resident), the Annual Value of their property, and the household income per person.

The overall discount on the MediShield Life premium for the Merdeka Generation is quite significant especially for the lower income.

You can estimate your MediShield Life premium by using the Premium Calculator on MOH’s website[6] (before the 5%/10% Merdeka Generation premium discount).

Is MediShield Life adequate for you?

MSHL is catered for those who will stay at Class B2 or C wards at restructured hospitals. These are heavily subsidised wards with basic amenities and no flexibility to choose your preferred doctors.

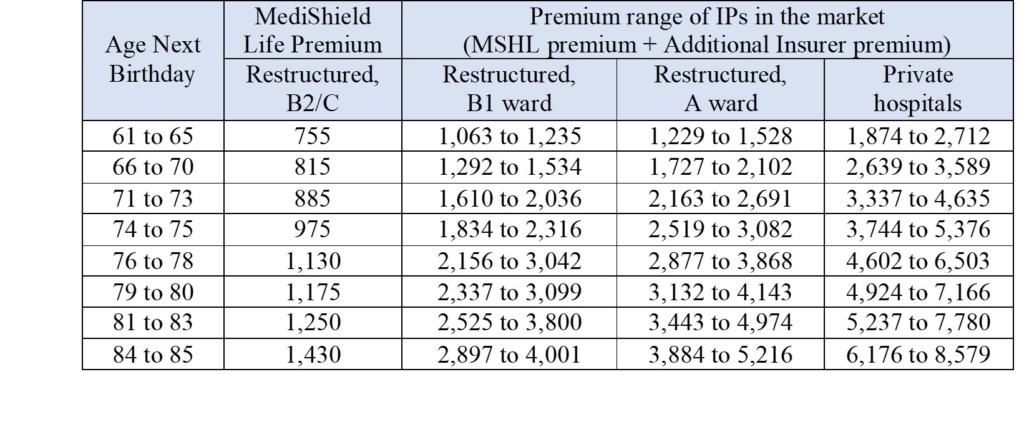

Those who prefer amenities such as air-conditioning, attached TVs and toilets or choice of own doctors, may upgrade to an Integrated Shield Plan (IP) for:

- Restructured hospital in B1 ward

- Restructured hospital in A ward

- Private hospitals

Interestingly, more than 6 in 10 people in Singapore own an IP and about half of them are catered for private hospitals. With rising IP premiums, some may find it no longer affordable.

Upgrading or downgrading your IP

Before making changes to your MediShield Life or IP, you should consider the following.

- Affordability

The premium for MSHL/IP increases over time. Consider the current and future premium.

The MediShield Life Premiums shown above are before any subsidy given based on household income as well as the 5%/10% premium discount for the Merdeka Generation (refer to the previous table for reference). With these subsidy and discount, the IP premium will be lower than reflected above.

Note that you can pay the MediShield Life premium fully using Medisave. For IP, you can only use Medisave to pay the additional insurer premium up to these caps:

- $300 if you are 40 years old or younger on your next birthday.

- $600 if you are 41 to 70 years old on your next birthday.

- $900 if you are 71 years or older on your next birthday

You can compare IP plans here (URL: https://www.moneyowl.com.sg//app/direct)

- Always Upgrade or Downgrade with the same insurer

If you must upgrade or downgrade your IP, the golden rule is to make changes within the current insurer. If you switch to a different insurance company, the new insurer could impose exclusion on pre-existing conditions that you may have. What this means is that you cannot make any claims on the IP that is related to the excluded pre-existing condition.

Third Safety Net – Long-Term Care

Many will require long-term care due to severe disability in old age. A person is severely disabled if he or she is unable to perform at least 3 Activities of Daily Living (ADLs) independently, namely, feeding, dressing, toileting, washing, mobility, and transferring. When it happens, caregiving is needed.

ElderShield was launched in 2002 to address the financial concern of long-term care. Being a non-compulsory scheme, a significant number of people chose to opt-out especially when it first started. The benefits of ElderShield are kept low for affordability. Monthly payouts are either $300 for up to 5 years or $400 for up to 6 years.

CareShield Life

From 2020, CareShield Life (an improvement from ElderShield) will be launched. Not only does it provide higher payouts of at least $600 (which increases till age 67 or when a claim is made, whichever earlier), the payouts are for life as long as severe disability persists. Severe disability can be due to a physical injury, illness or even severe mental impairment.

You can read our commentary on CareShield Life (URL: here)

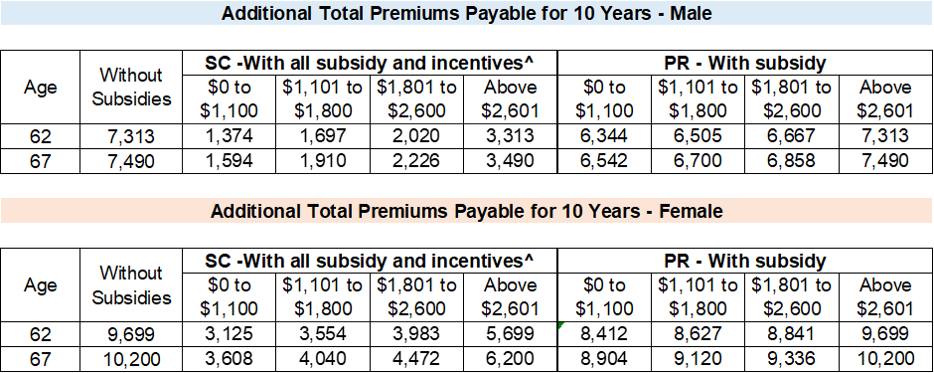

Merdeka Generation seniors who are not severely disabled can join CareShield Life in 2021. To encourage Merdeka Generation seniors to join CareShield Life, an additional participation incentive of $1,500 is given to join the scheme. This is on top of a previously announced $2,500 sum, making it a total of $4,000 discount to offset CareShield Life premium. This is in addition to current means-tested premium subsidies.

Your CareShield Life premium is dependent on several factors including your age, gender, citizenship, monthly per capita household income, residential property, and whether you are currently on ElderShield plan or not.

Estimated CareShield Life Premium Table for selected Merdeka Generation ages (currently with Eldershield 300 and staying in an HDB flat)

^ Incentives include both Participation Incentive and Additional Participation Incentive for MG

For a male, age 62, Singaporean, whose monthly per capita household income falls within the $1,101 to $1,800 range, his CareShield Life premium is estimated at $1,697 after subsidy and incentives for ten years. This works out to less than $170 per year. Premium without subsidy is estimated at $7,313, or about $731 per year.

The full details on CareShield Life premium will only be available later. However, you can estimate your premium using the CareShield Life Premium Calculator[7] but it is only restricted to certain scenarios[8].

Those who opted out of ElderShield can either wait till 2021 to sign up for CareShield Life or get immediate coverage by first applying for ElderShield provided they are not older than 64 and are not severely disabled.

Should I switch from ElderShield to CareShield Life?

Monthly payouts of $300 to $400 under ElderShield are insufficient to meet long-term care costs, especially as severe disability is likely to last longer than the 5-6 years after the occurrence.

While you may have income from CPF LIFE payouts, it can be a strain to pay for long-term care costs out of these payouts.

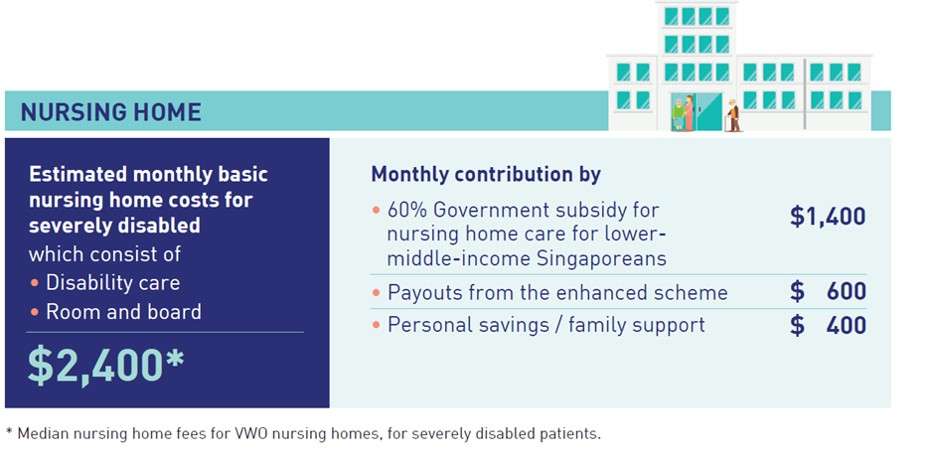

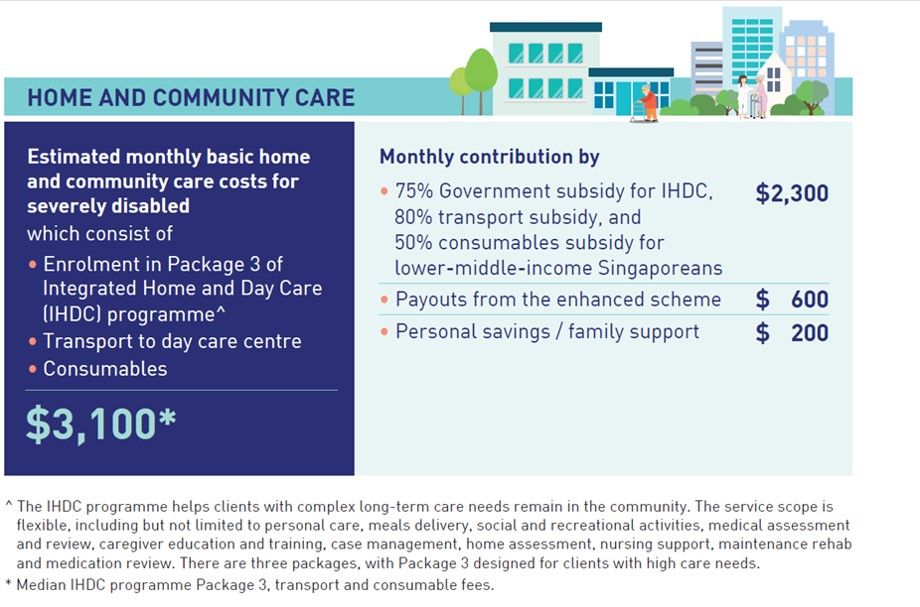

Long-term care options include staying in a nursing home, being looked after by a helper or family member at home, or a combination of day care and homecare. The cost can easily range from $1,000 to over $3,000 per month before subsidies. Even after means-tested subsidies and CareShield Life payouts of $600, there will still be a cost that has to be borne out of one’s retirement income.

Estimated Costs of Long-Term Care Options for lower-middle-income Singaporeans after subsidy and CareShield Life Payouts

Given the high probability of severe disability, the duration of disability should it happen and the strain of long-term care costs on the family, Merdeka Generation seniors who are not yet severely disabled should consider joining CareShield Life early to take advantage of the Participation Incentives if they are able to afford the premiums. This will provide a better safety net for long-term care.

You can further enhance the payouts by adding a supplementary Long-Term Care Plan (or ElderShield Supplement) from a private insurer. You can compare long-term care plans here (URL: https://www.moneyowl.com.sg//app/direct )

Eddy Cheong, CFP is Chief Advisory Officer of MoneyOwl.

[1] Refer here for subsidies rate for Permanent Residents and those living in larger properties. https://www.moh.gov.sg/medishield-life/medishield-life-premiums-and-subsidies/premium-subsidy-tables

[2]Lower-income refers to individuals with a household monthly income per person of $1,100 or less.

[3] Lower-middle-income refers to individuals with a household monthly income per person of $1,101 to $1,800.

[4] Upper-middle-income refers to individuals with a household monthly income per person of $1,801 to $2,600.

[5] High-income refers to individuals with a household monthly income per person of more than $2,600.

[7]https://www.moh.gov.sg/careshieldlife/about-careshield-life/careshield-life-premium-calculator

[8] If you have ever opted out and re-joined ElderShield, have a single or 10-year ElderShield premium payment plan, or have a paid-up policy, your personalised premiums will be available closer to 2021.