Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Estate planning – one of the most important aspects of financial planning

In this sixth and final article in the Merdeka Generation series, we will be exploring estate planning – one of the most important aspects of financial planning that may often be overlooked by seniors and younger people alike. Indeed, everyone needs to plan ahead and take action while one still has the mental capacity, as one never knows when something may happen. For seniors in the Merdeka Generation, there may be a heightened sense of urgency as one starts to age.

Estate planning concerns the loved ones left behind upon your eventual passing, how you can provide them with your hard-earned assets – leaving a legacy for your family and loved ones, a final act of love.

So, what happens to our assets when we pass on? How would these assets be distributed and who gets what? These are important questions that should be decided by none other than you – the owner of your assets – and distributed in accordance with your wishes. Without proper planning, we could be leaving a financial mess for our loved ones to pick up after our passing.

Distribution of assets upon death – or estate distribution – need not be difficult. A better understanding of the estate rules governing common assets such as property, CPF savings, life insurance, and the benefits of having a will, and taking action thereafter, can ensure that our assets will go to our intended beneficiaries without unnecessary hassle.

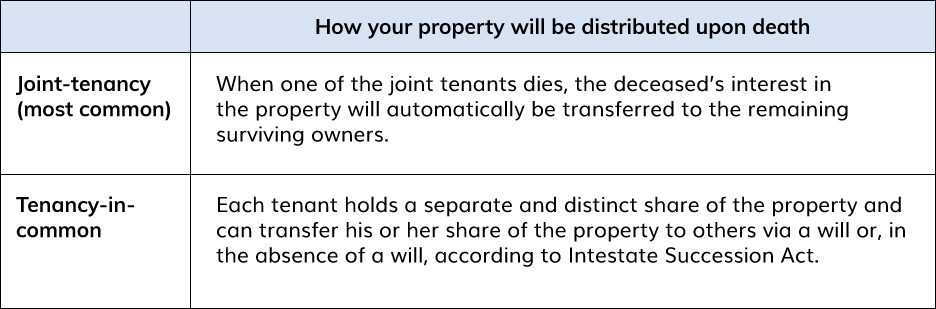

Home Property

How your share of the property gets transferred upon death depends on how it is being held, whether joint-tenancy or tenancy-in-common.

Take, for example, Mr. and Mrs. Tan who are joint-tenants of a property, and if, say, Mr. Tan passes on, the surviving spouse (Mrs. Tan) will inherit and become the sole owner of the property. As the property is under joint-tenancy, Mr. Tan cannot create a will to distribute away his share. However, if the property is held under tenancy-in-common, Mr. Tan could write a will to distribute away his share to others.

Most properties are held under joint-tenancy. You can find out your property ownership status here

What if yours is an HDB flat?

HDB flat can only be retained if the beneficiaries fulfill certain eligibility criteria including Singapore Citizenship or Singapore Permanent Residency and are at least 21 years of age; otherwise, it must be sold.

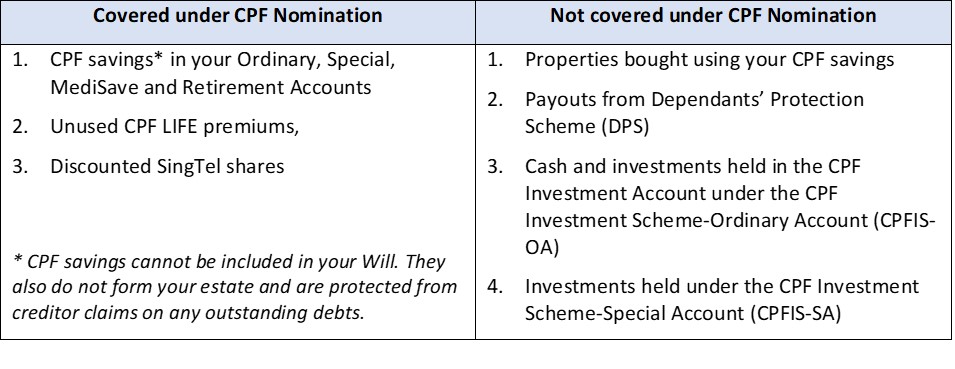

CPF savings

You should make a CPF nomination to specify how your CPF savings should be distributed. In the absence of a CPF nomination, your CPF savings will be transferred to the Public Trustee’s Office for distribution to your family under the Intestate Succession Act or the Inheritance Certificate (for Muslims).

Your CPF savings cannot be distributed via a will.

The process of disbursement via CPF nomination is swift, and I have personal experience in this regard. When my father passed on a few years ago, the CPF Board disbursed the CPF monies to my mum (the nominee) very quickly within 3 weeks because my late father did a CPF nomination. To my mum, it was not so much the money she inherited, but the expediency of settling such matters did help to bring about a closure sooner.

What does a CPF Nomination cover?

Not all assets involving CPF are covered by a CPF nomination. Those assets not covered must be addressed separately.

What are the different types of CPF Nomination?

Before making a CPF nomination, do note there are 3 types to choose from depending on your needs.

1. Cash Nomination – this is the default option. In this nomination, your nominees will receive the CPF savings in cash. Download the form here (URL: https://www.cpf.gov.sg/Members/Schemes/schemes/other-matters/cpf-nomination-scheme).

2. Enhanced Nomination Scheme Nomination – Your nominees will receive the CPF savings in their CPF accounts. You can decide to transfer your CPF savings to their:

- MediSave account – for their healthcare needs; or

- Special account – for their retirement needs.

Visit any of the CPF Service Centres to make this nomination.

3. Special Needs Savings Scheme Nomination – this allows parents to nominate their special needs children to receive the CPF savings on a monthly basis. To make this nomination, you would need to work with the Special Needs Trust Company (SNTC) and the CPF Board. More information on this scheme here .

Life insurance policies

If there are no beneficiaries named in your insurance policies, the proceeds can be distributed by way of a will or, in the absence of a will, by the Intestate Succession Act.

With effect from 1 September 2009, you can make a revocable nomination or a trust nomination on your insurance policies for your beneficiaries.

- A trust nomination – is irrevocable and is meant to benefit your spouse and/or children.

- A revocable nomination – can name any person as a nominee and can be revoked anytime by you.

If there are beneficiaries named in your insurance policies before 1 September 2009, there could be some potential issues:

- If the named beneficiaries are a spouse and/or children, your policy is now under Section 73 of the Conveyancing and Law of Property Act, essentially you have created a statutory trust. This cannot be revoked unless the named beneficiaries give their consent.

- If the beneficiary is anyone other than a spouse or children, there may be issues regarding its validity. Hence it may be prudent to remove the named beneficiary and do a revocable nomination or distribute it by way of a will.

Having a Will

Other than most circumstances as explored above, the deceased’s estate of a non-Muslim will be distributed either by way of a will or, in its absence, according to the Intestate Succession Act.

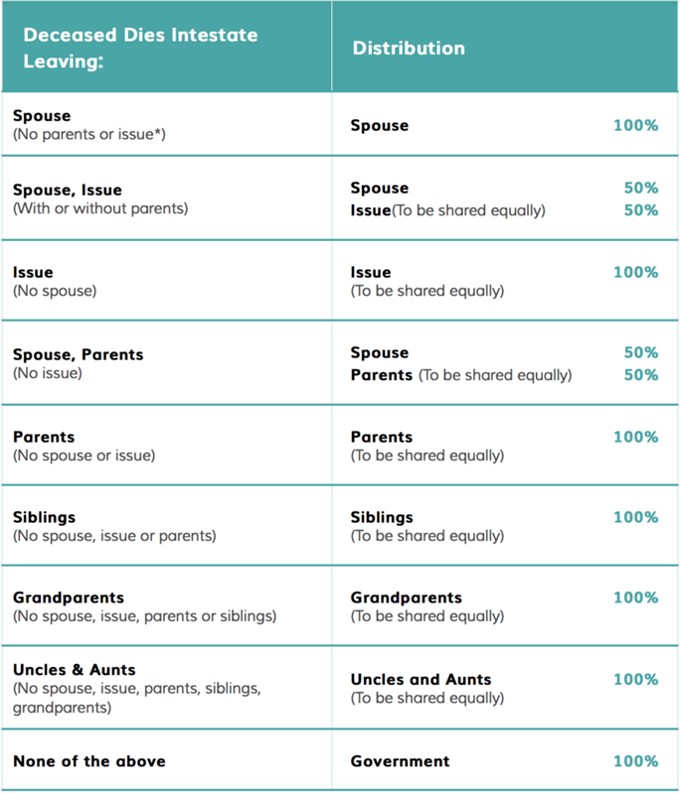

Death without a Will – Intestate Succession

Without a will, the distribution of a deceased’s estate will follow the priority as set out by the Intestate Succession Act (ISA).

Under the ISA, spouse and children take precedence over parents, siblings and other family relationships. While it may seem logical with some, such a distribution order can be problematic, such as:

- A married person with children hopes to leave behind something for his or her parents. Under ISA, the parents are excluded.

- A single person wishes to provide for both his or her parents and siblings. Siblings are excluded in this case.

These issues can be easily solved by having a will.

Benefits of a will

With a will, you can decide who your beneficiaries are and how much they get. Equally important is the control you exercise to choose whom you trust to be your executors, trustees, and guardians. Having a will can also avoid the potential conflicts and disharmony among loved ones who may dispute how the estate should be distributed. Lastly, the process of administrating the estate is generally faster with a will than without one.

Interestingly, many people do not have a will. Common reasons are the high cost of writing a will, not knowing how to begin, and perhaps the time is not right.

With MoneyOwl’s online will writing service, which is complimentary with a promotional code, there is no reason to put off will writing any further. The guided will writing process will help you draft out your will in no time. Get it printed and signed before two witnesses (who cannot be a beneficiary or the spouse of a beneficiary) and your will is legally binding. If you need to make further edits, just come back and use the service again.

More info on Why Write a Will?

Lasting Power of Attorney (LPA)

Finally, do consider making a Lasting Power of Attorney while you have the mental capacity to do so. An LPA basically allows you to appoint one or more people [‘donee(s)’] to manage your personal welfare and property should you (‘donor’) lose mental capacity one day.

A donee can be appointed to act in 2 broad areas, whether separately or jointly:

- Personal Welfare – such as, where and who should donor live with, healthcare matters, what to wear and eat.

- Property and affairs – such as dealing with the donor’s property, managing bank accounts, investing, and making purchases of equipment for donor’s needs.

To make an LPA, you need to:

- Fill up a form from the Office of Public Guardian. From now till 31 August 2020, the LPA application fee is waived for the most common LPA option (Form 1).

- Engage a certificate issuer to sign as a witness and certify that you understand the implication of an LPA. A certificate issuer could be an accredited medical practitioner, a practicing lawyer, or a registered psychiatrist. The average fee charged by an accredited practitioner is about $50.

- Send the form and certificate back to the Office of Public Guardian for registration. If there are no valid objections in the six-week waiting period, your LPA will be registered. The stamp of the Office of Public Guardian will be impressed on the registered LPA. The Office of Public Guardian will send it back to you for safekeeping.

Conclusion:

We can come to the end of the 6-part series on Financial Planning for the Merdeka Generation. I hope that this series has given you some ideas on how to prepare for your retirement with greater confidence.

Eddy Cheong, CFP® was the Chief Advisory Officer of MoneyOwl.