Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Find out more about housing matters in this article for the Merdeka Generation

We all know someone from the Merdeka Generation perhaps a parent, neighbour, colleague or even yourself. Born in the 1950s, each has a story to tell, stories of how one lived through the independence struggle of the nation, joined the workforce early and experienced serving National Service as one of the earliest batches. These are men and women who contributed to the early nation-building of Singapore. In the next few articles in this series, we will be covering the retiree’s journey and the second Must-Have in Retirement – your monthly income for retirement. Stay tuned.

In recognition of this special group of unsung heroes, the Merdeka Generation Package (MGP) worth more than $8 billion was created primarily to support their medical needs in the silver years. As announced in Budget 2019, the MGP includes:

- One-time $100 top-up to PAssion Silver cards.

- Additional annual Medisave top-up of $200 from 2019 until 2023

- Additional CHAS subsidies for outpatient care, for life

- Additional MediShield Life premium subsidies for life, with means-testing

- Additional Participation incentives of $1500 to join CareShield Life from 2021, on top of a previously announced $2500 sum, i.e., $4000 in total.

In the following days, more details on the package benefits will be made known.

Financial Planning for Merdeka Generation

People of the Merdeka Generation are either in retirement or nearing retirement. A common worry among them is their retirement adequacy, whether there is enough money for their living expenses as well as medical needs. The question of “enough” is a subjective one and is dependent on one’s means and expectation. In any case, when it comes to retirement, there are essentially 3 Must-Haves to consider:

- A home to stay in

- Monthly retirement income for life

- Medical safety net

To offer some perspectives on this, we have put together a series of articles to highlight these planning considerations as well as a piece on the eventual distribution of the estate to the loved ones upon demise.

Let us start with the housing matters in this first article.

1. A fully-paid home

We all need a place to stay, a place we call home, where lives and memories are built. All thanks to our housing policy, most households here (more than 90%) owns a property. I remember when my parents bought their first HDB flat in 1970, a 3-room flat in Toa Payoh was only about $8,000. Even with his meagre salary, my dad was able to fully repay the home loan quite easily. Some, however, continue to upgrade their houses and in the process added more loans. My guess is most of the Merdeka Generation would have repaid their mortgages by now, but if for some reasons if one has not, the immediate goal is to review the finances and try to pay it off as soon as possible in preparation for retirement. There is psychological bliss, peace of mind, from being debt-free.

What if there are difficulties in clearing the loan? Or if one is caught in an asset-rich, cash-poor dilemma? What should you do?

There are no easy answers but suffice to say that you need to review your assets, optimise your savings, CPF and estimate how much is needed for your retirement. We will cover more of that in the next article.

One option to monetise your property, i.e. unlocking it to supplement your retirement needs. There are a few ways to go about it and the ultimate decision boils down to personal preference.

2. Monetise by renting out spare room(s) or whole flat

Do you have a spare bedroom or have alternative accommodation arrangement such as staying with your children? If so, renting out the excess space for income is not a bad idea. I have seen my relatives doing so, even though they are certainly not in any financial difficulties. Renting out excess space rewards them with the extra money to enjoy their retirement. A spare room can typically fetch about $600 to $1,200 in rental income depending on location and condition.

The benefits of this option include keeping your property (and your neighbours), receiving rental income and continuing to participate in the appreciation of your property value.

3. Monetise by down-sizing

But what if you do not wish to share your property with others? Or find that the current house is now too big to upkeep as your children or family members have moved out. In such cases, perhaps downsizing or right-sizing is a consideration. This option allows you own the entire unit, albeit a smaller one, but with extra money from the exercise.

One affordable option of a smaller flat is the 2-room flexi unit from HDB. You can select how long a lease you need. The shorter the lease, the smaller the property price.

Seniors who are aged 55 and above can take up a lease of between 15 and 45 years as long as it must cover the age of the applicants up to 95 or more.

Such a flat is quite attractively priced. According to HDB as of April 2018, such a flat is priced around $150,000 in the matured estate and $90,000 in the non-matured estate for a 40-year lease [1]. These flats are getting quite popular in recent years and HDB has been ramping up supply of such units to meet demand.

Besides receiving extra money from downsizing, you could also save on running cost from lower conservancy charges, property tax and lower upkeep of a smaller unit.

4. Monetise by Lease Buyback Scheme (LBS)

Finally, what if you prefer to age in place because you love the neighbourhood or you just cannot accept the idea of renting out your rooms? In that case, there is the Lease Buyback Scheme (LBS).

In LBS, you are essentially selling the tail-end lease of your flat back to the HDB for money. In this way, the lease of your flat is now shortened. There are conditions on the sales proceeds, which requires one use the money to first do a top-up into your CPF Retirement Account (RA); any remaining balance would then be available for cash spending. The whole idea of the top-up is for you to join CPF LIFE which will then provide a stream of income for your retirement for life.

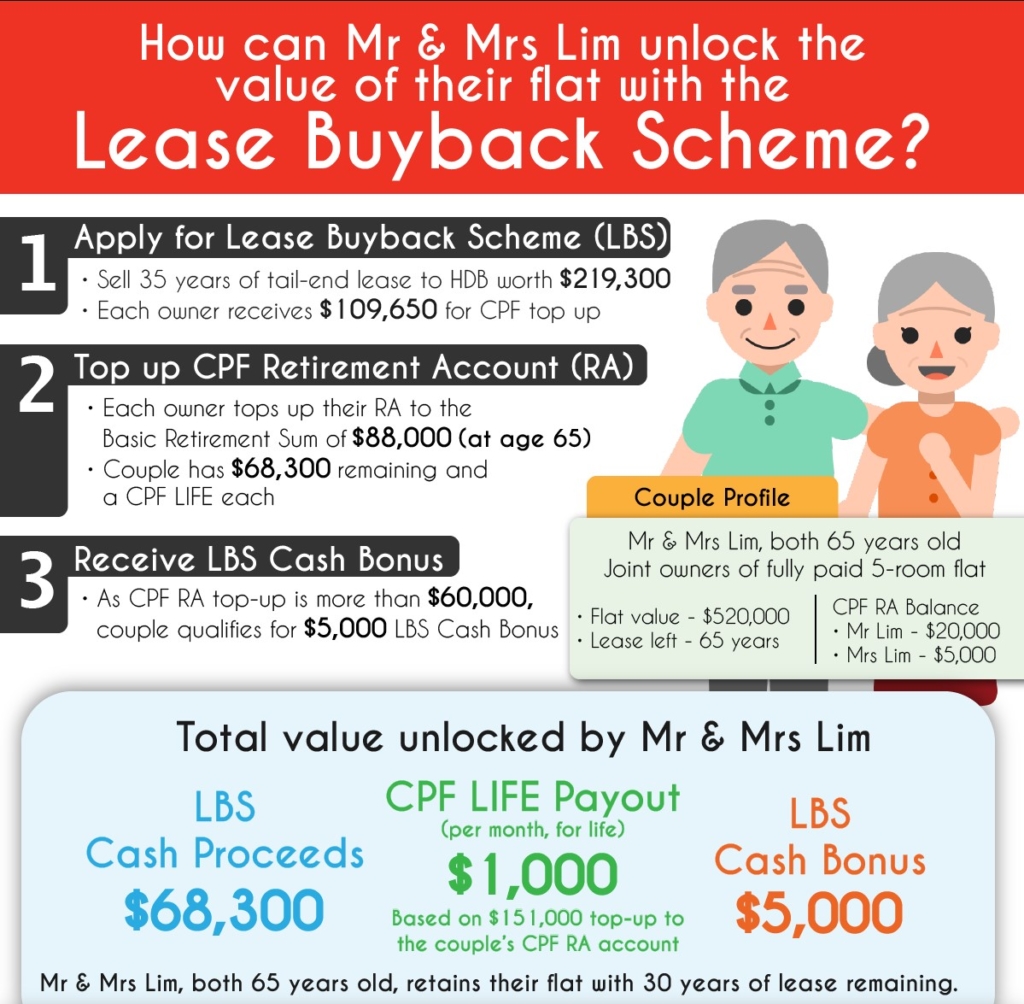

Perhaps the following example from the HDB website [2] can help us understand how the LBS works.

In this example, Mr & Mrs Lim, both age 65, own a fully paid 5-room flat, valued at $520,000 with a remaining lease of 65 years. Their CPF-RA savings stand at $20,000 and $5,000 respectively. With such low CPF savings, their combined CPF LIFE payout (assuming Standard plan) is about $160 [3] monthly. This is insufficient for their retirement needs if that is all they have.

Suppose they decide to participate in LBS, this is how it works:

- Sell off 35 years of their flat’s lease to HDB for $219,300.

- Sales proceeds to top-up their respective CPF-RA up to the Basic Retirement Sum of $88,000.

- $151,000 is required to do the top up; ($88,000 – $20,000 + $88,000 – $5,000)

- Net proceeds left after CPF top-up is $68,300 ($219,300 – $151,000)

- Receive a $5,000 LBS Cash Bonus, since the CPF top up is more than $60,000.

Benefits of LBS

The couple could now receive a lump sum cash payout of $73,300 and a monthly income stream from CPF LIFE of $1,000. Not bad considering that before this, the couple could only enjoy about $160 monthly from their CPF LIFE.

The key drawback of LBS is the once in the scheme, you are not allowed to sell the flat in the open market or rent out the whole flat. In other words, you are not able to participate in the potential appreciation of the property value.

What if you outlived the lease period, e.g., beyond age 95? HDB assures you that in such a situation, you will not be left without a home. HDB will review your circumstances on a case-by-case basis taking in factors such as family support, health conditions and financial status and work out an appropriate housing arrangement with you.

Read their website for more info on LBS.

In the next article, we will be covering the second Must-Have in Retirement – your monthly income for retirement. Stay tuned.

MoneyOwl is Singapore’s 1st bionic financial adviser. To find out more about us, visit www.moneyowl.com.sg

Eddy Cheong, CFP, is Chief Advisory Officer of MoneyOwl.

[1] Source: HDB data dated 24 Apr 2018, https://www.hdb.gov.sg/cs/infoweb/various-options-for-seniors-to-monetise-hdb-flats

[2] Source: http://www.hdb.gov.sg/cs/infoweb/img/top-up-worked-example.jpg;wa54c8c9d1c6f02b4f

[3] Source: This amount is estimated from the CPF LIFE Estimator. Mr Lim is estimated to receive $$126 to $133 monthly and $29 to $31 monthly for Mrs Lim.