Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

There was a recent article that discussed when it was suitable to Buy Term and Invest the Rest (BTIR) and when to use Whole Life Insurance.

Contrary to what many think, the purpose of buying term insurance is not so that one can invest the difference from the amount saved by buying a term instead of a whole life.

The main purpose of buying insurance is for protection and buying Term Insurance is the best way to be sufficiently covered. Whether one should invest the rest is a different discussion together.

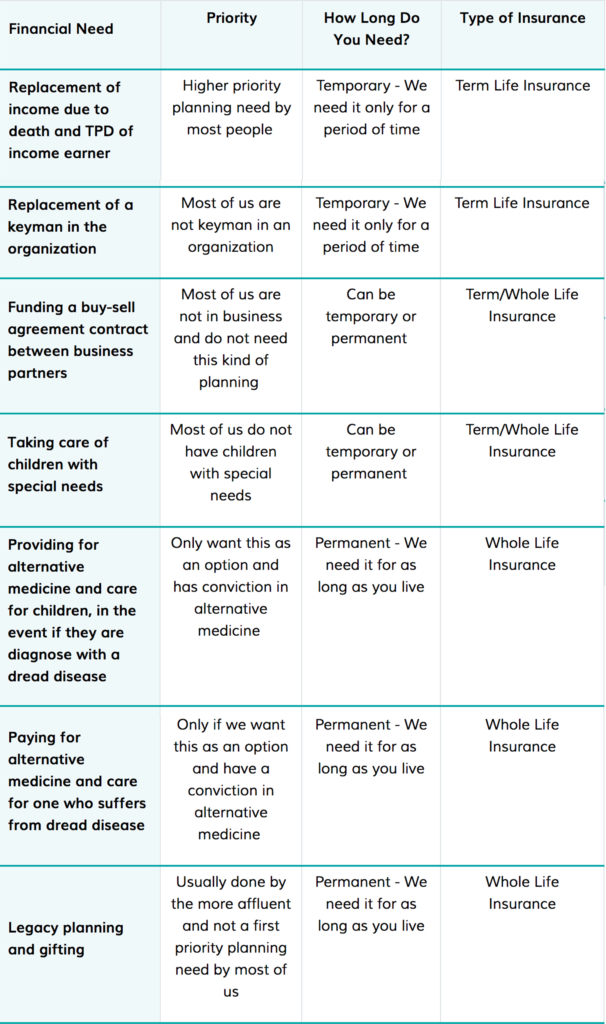

Why Is Term Insurance The Most Appropriate?

Most people are not against that the main purpose of insurance is for protection, to transfer a potential financial risk loss to the insurer. There are 2 main reasons why term insurance is the most appropriate to help us achieve our purpose.

a. Most of our top priority needs are not permanent

b. Term Insurance is the most affordable way to be fully covered

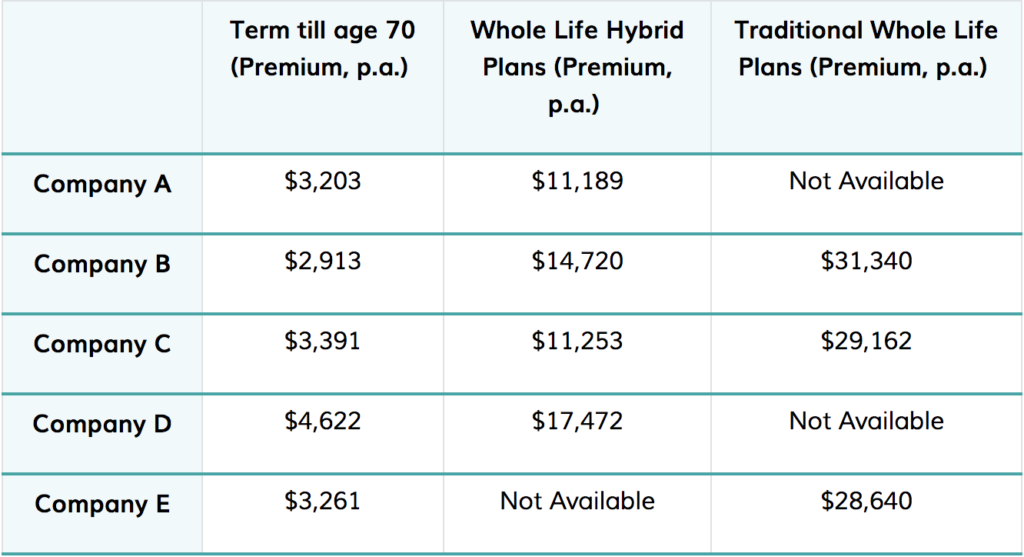

We illustrate with an example. For a 45-year-old male to be insured with $1M life insurance coverage, a term insurance policy would cost $2,913 while a whole life insurance would cost $29,162.

Possible insurance plans for a 45 year-old male to cover $1,000,000 Death/TPD

How many of us are willing to pay more than $20,000 a year to insure ourselves? Most people in Singapore would pay $3,000 a year towards a whole life plan and end up being severely underinsured.

The Use of Whole Life Insurance

As illustrated in our table of insurance needs, most of our high priority planning needs are temporary can be taken care of using Term Insurance. After we have sufficiently insured ourselves for the high priorities, we can begin to look at our lower priorities.

You should only consider whole life insurance if you want the option of providing for alternative medicine. However, you need to weigh this want against other needs you may have such as providing for your retirement and your child’s education.

Use whole life insurance to help you manage your risk for your needs that are permanent and not because for the reason that it is better than the philosophy of “Buying Term and Investing the Rest”.

On Investing

The recent article also assumes that one could face a 30% drop in value of one’s investment portfolio near retirement age.

This is unlikely to occur.

Most retirees de-risk their investment portfolio nearing retirement. During the worst of the financial crisis in October 2008, the US S&P500 index total returns (inclusive of dividends) was -16.78%. If you were in a conservative portfolio then, your portfolio would have dropped by -7.48%, a drop which is easier to stomach. No one should experience a devastating drop in the value of their entire investment portfolio near/during retirement.

Alternatively, use a “Bucket System” for your retirement. For monies that you need to draw-down in the short-term, they should be in safer portfolios. (Eg. money market funds and funds with a large proportion in bonds). For monies that you only need later (15-20 years), you can invest in more aggressive portfolios as you have time to ride the volatility of the markets.

We have written a series of articles on how one can manage their investments and draw-down during retirement. Read the 9-part RetireWell series that was published in the Business Times over 10 months.

If you are keen to grow your wealth, there are many instruments available to do so. It is not necessary to use an insurance product. Before investing in any product, consider the following factors:

- Liquidity (how easily can you sell your investments when you want to)

- Cost (the higher the cost of the instrument, the lower your return)

- Asset Allocation (Does it invest in a diversified global portfolio?)

- Risk (Does the portfolio match your risk profile?)

- Strategy (Does it aim to market-time/stock-pick or is it a passive instrument? Research has shown that those who market-time/stock-pick do not beat the market in the long-run)

Insure the Right Way

In the last protection gap study conducted by Life Insurance Association Singapore (LIA), the overall protection gap in Singapore as at the end of 2011 is S$462 billion.

Despite paying a lot towards their insurance policies, many people in Singapore are not sufficiently insured and are not insured for their top priority needs.

It is only when we understand the true purpose of how we use the different types of insurance to meet our needs that we can spend smartly on insurance and insure our loved ones and ourselves the right way.

Announcement: With effect from 1 June 2022, MoneyOwl is a 100% NTUC Enterprise (NE)-owned company.