Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

If the current state of investing dynamics constitutes a “bubble”, what does that mean for our financial plan?

A few days ago, Michael Burry, a fund manager whose massively successful bet against the US subprime housing market was dramatised in the film, “The Big Short”, said that passive investing was a “bubble” that had caused investors to neglect small caps and value stocks.1 This drew an energetic response from financial adviser Joshua Brown of Ritholz Wealth Management, who said that the real bubble had always been in active management – an investor hobby for stock picking that was a historical anomaly.2

The first thought that came to mind when I read this exchange was that MoneyOwl’s globally diversified portfolios contained what both sides wanted. The Dimensional funds we use to make up our portfolios can be described as “enhanced indexed funds”. The manager takes a broad global index as the core (similar to indexed or passive investing) but tilts it towards dimensions that have shown evidence of higher expected return, namely, profitability, value, small size (the latter two being favoured by Michael Burry). Dimensional funds have a low expense ratio of average 0.35% p.a. and employ no forecasting and no market timing.

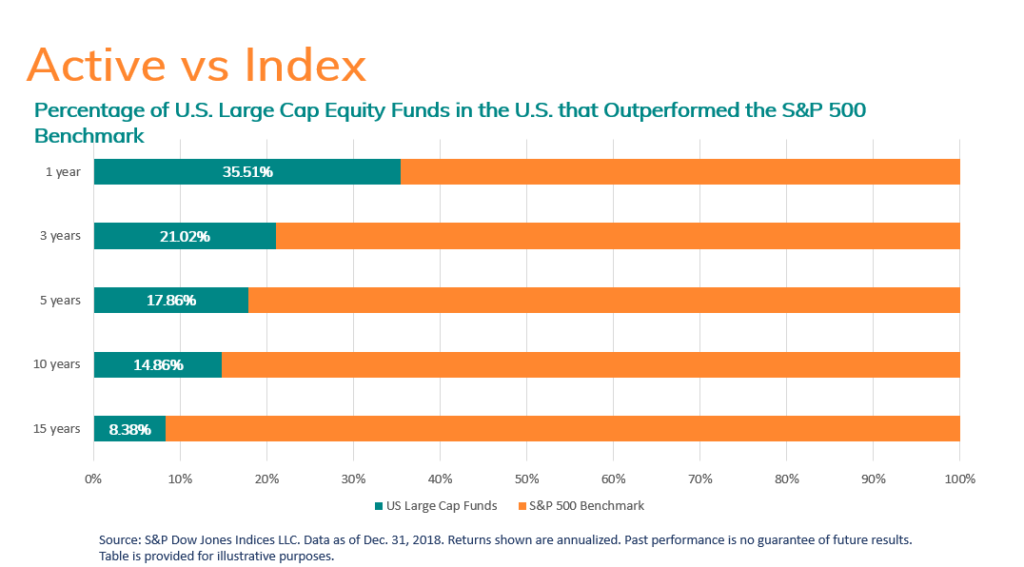

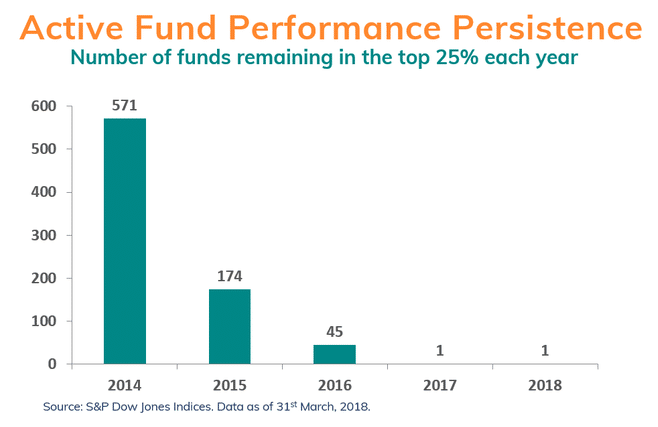

But the choice of the word “bubble” to describe passive investing deserves deeper discussion. Given that the bursting of the last bubble was painful – this was the very “housing bubble” that Burry had predicted – the word brings with it fear of a huge crash and large losses. Joshua Brown had countered that passive investing was popular, but this did not make it a bubble, any more than saying that water was wet. Brown’s view was that a bubble was characterised by unsustainability and the only thing that had been unsustainable thus far was a reliance on active management to deliver above-market returns. There is good data supporting Brown’s thesis. Over multiple time frames, active managers have struggled to beat indices and even those who sometimes do, cannot do so consistently. Not saying that it is impossible, but that it has proven to be very hard.

What is it that makes a bubble unsustainable? A bubble is prone to bursting because it is not filled with substance. The US housing subprime crisis was a bubble. The supposedly highly-rated mortgage-backed securities (which packaged a hundred or so underlying subprime mortgage loans), the Collateralised Debt Obligations or CDOs (which packaged the mortgage-backed securities that packaged the loans) and even CDO-squares (which packaged the CDOs that packaged the mortgage-backed securities that packaged the loans) were products of financial engineering. Financial engineering turned mortgages lent to borrowers with very poor (subprime) credit standing into AAA, AA, A and BBB-rated securities. These investment-grade securities were anything but – they were filled with air. Furthermore, CDOs are, by construction, leveraged structures – meaning that a 20% loss in the underlying asset (in this case, mortgages) can wipe out the investment in the security by much more. Add in mortgage fraud, broker dishonesty, unscrupulous selling, a failure of stewardship and greed for yield, and there we had the bubble which burst when interest rates rose and house prices fell.

But passive investing is fundamentally about investing in companies’ earnings and shareholder value. Here I am talking about investing that tracks truly diversified, market indices and not narrowly defined sector or factor-based indices. A passive fund buys the stocks of companies, just like an active fund – it is just that the passive fund manager buys them in proportion to what market participants in aggregate (made up of all active fund managers, sovereign wealth funds, individuals, speculators and so on) buy. There is no inherent leverage in the plain vanilla passive funds which also do not use synthetic derivatives. How, then, can passive investing in real companies be a bubble, if active investing, which is also about investing in real companies, isn’t?

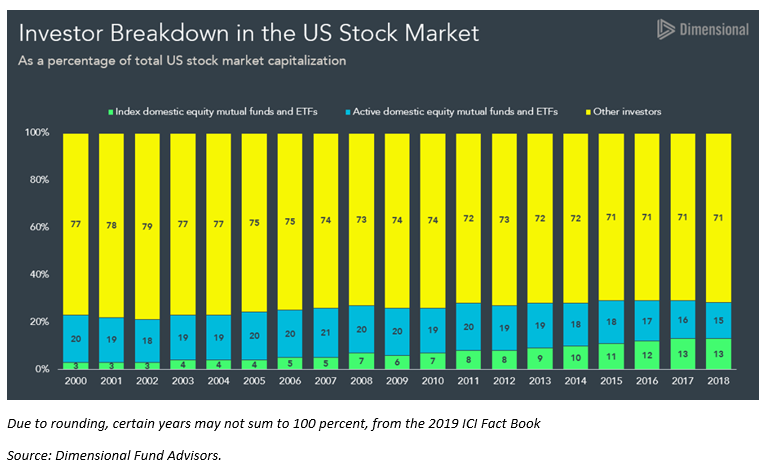

Let us also take a look at how much passive investing there actually is. Indeed, index-based approaches have become increasingly popular in recent years, but based on information from the Investment Company Institute, by US total stock market capitalisation, domestic index mutual funds and ETFs comprised only 13% in 2018. That said, it should also be noted that many investors use nominally passive vehicles such as ETFs to engage in traditionally active investing, through dynamic or tactical asset allocation, which are often euphemisms for market timing.

Besides, the rise in investing in market-cap weighted index funds is not the culprit for growth stocks appreciating in price more than value stocks, even though growth stocks tend to have large market capitalisations. Suppose we have a portfolio comprising a growth stock of a market cap of $80 and a value stock with a market cap of $20, for a total value of $100. If the portfolio itself goes up to $120, the return on both stocks would be the same, 20%. Fund flows into the index fund does not cause an outsized price appreciation of the larger stocks in percentage terms.

One final point – even if the current state of investing dynamics constitutes a “bubble”, what does that mean for our financial plan? An investor who had continued to invest through the bursting of the US subprime housing bubble would have averaged down and captured the returns that came with the recovery; whereas one who sold too early and failed to get back in – like many active managers in the 2008-2009 period, just because market timing is so difficult – would have given up a lot of return. What you need is the time horizon to ride out the fluctuations; if you have a shorter time frame, you should allocate part of your portfolio to bonds to cushion the volatility. Indeed, every few decades, the stock market goes through a crisis, but no matter how bad it is, the market always recovers and goes up in the long run. This is because over the long term, the stock market is driven by companies’ earnings, which are in turn driven by demand, and global demand in aggregate is driven by population growth and an increase in standards of living. This is as fundamental and non-bubbly as it gets.

The writer, Chuin Ting Weber, CFA, CAIA, is Chief Executive Officer and Chief Investment Officer of MoneyOwl. Our investment advisory platform at www.moneyowl.com.sg can help you to arrive at a suitable asset allocation based on your time horizon and risk profile. You can also read more about MoneyOwl’s investing philosophy.

1. https://www.businessinsider.sg/big-short-investor-michael-burry-calls-passive-investment-a-bubble-2019-8/?r=US&IR=T

2. https://thereformedbroker.com/2019/08/29/the-real-bubble-has-always-been-in-active-management/