Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

What a tumultuous past couple of years it has been. The history pages would undoubtedly colour them as some of the most tainted, testing the will of many, including doctors, governments, and investors.

With black swan events like the pandemic and the Russian-Ukraine war riddling the past few years as well as pesky, out-of-control inflation forcing the Fed’s hand into quantitative tightening – an anti-thesis to businesses’ profitability – was investing during this time still practical?

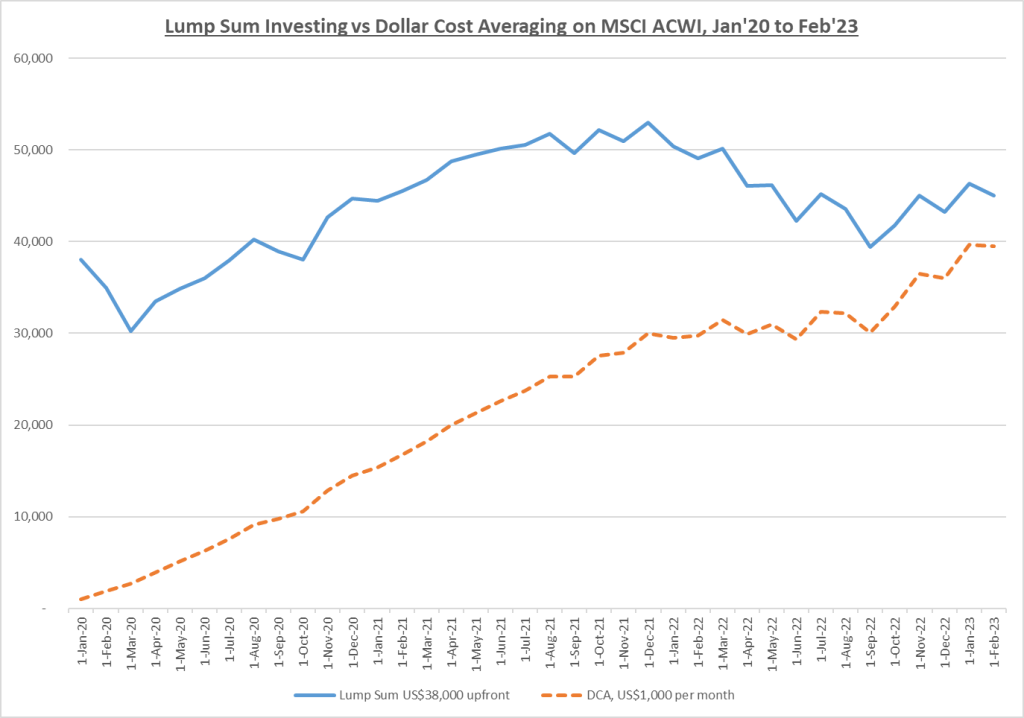

How would a US$38,000 portfolio have performed from 31-Jan-2020 to 28-Feb-2023?

Specifically, if Mr Owl had a crystal ball in January 2020, would he have been better off putting off investing? How would a US$38,000 sum invested in the MSCI All Country World Index on 31-Jan-2020 fare on 28-Feb-2023?

It would surprise most that that portfolio would have stood at US$44,997.06, netting Mr Owl a cool US$6,997.06 in profits at an annualised return of 5.48% p.a.! Not bad for such a volatile period, and Mr Owl was finally able to buy that nice handbag that Mrs Owl had secretly admired all this while.

While the end of the road was a sweet one, this journey was one of those “simple, yet not easy” kind of thing. You see, although Mr Owl emerged net positive on 28-Feb-2023, little was spoken about the dark days of March 2020, when his portfolio plummeted to US$30,214.90, a staggering 20.5% drop. Never mind handbags; Mr Owl was afraid he wouldn’t have much of a nest egg (no pun intended) by the end of all this. Crucially, in that time of desperation, it was laudable that Mr Owl did not decide to withdraw his investments. However, when push comes to shove, not all investors might be able to stomach such a downturn.

So, what have we learned so far? To the uninitiated, it would seem that, notwithstanding the fact that sticking to the investment strategy would mostly always pay off, it is wrought with volatility and sleepless nights – and is the latter really something that we want to go through? At least Mr Owl was nocturnal!

Source: Morningstar

Market returns, without the sleepless nights

Well, there is another strategy that aims to get you there more comfortably. That is, to capture market returns while giving you a smoother ride. Dollar Cost Averaging (DCA) is a strategy that advocates spreading out your capital into multiple “bullets” instead of plonking it down all at once. If one had invested US$1,000 every month in the same time period, investing US$38,000 in total, he would still have seen an annualised return of 2.35%p.a., which, although lower than Mr Owl’s lump sum strategy, would have only exposed the portfolio (and Mr Owl’s heart) to an 11.3% drop on 31-Mar-2020 (compared to 20.5%).

In short, lump sum investing may sometimes net you a higher return, but DCA investing evens out the ride while still ensuring that you don’t miss out on market returns. DCA investing also makes it easier to stick to a plan, as it takes emotions out of the equation by buying when prices are low and when they are high. This way, wherever the market turns you will be buying, same date every month. What’s even sweeter is that once you automate this with a standing instruction and invest a fixed percentage of your income every month, you will be in a “set in and leave it” state of mind and no longer have to worry about what to do every time the latest headline presents on the news channel.

What our CIO (Chief Investment Owl) does for her own portfolio

I asked my Chief Investment Owl how she does it for herself. She does a combination of lump sum investing and monthly regular savings plan (RSP). That’s the best of both worlds! Beyond her emergency fund, which is in cash, and after topping up CPF Special Account to the max, she invested fully into a long-term retirement portfolio. Then, she has standing instructions for a monthly pre-set sum that goes into this portfolio, as well as another two, one for each kid’s education.

Whenever there is a larger cash inflow, e.g. if she has an annual bonus, or when markets are down, she will do lump sum investing again. For “dry powder” investing when markets are down, she may spread it out into three tranches, and invest a third of the “dry powder” once every month. This is also a kind of limited DCA-with-lump sum hybrid that can help psychologically.

When owl’s said and done

We hope this article has helped clarify any doubts you may have had about whether investing is profitable during bad market cycles. More importantly, we believe that if you had been sitting on the fence about investing due to a bad appetite for volatility, you would find comfort in the benefits that DCA investing provides, as an additional strategy to lump sum investing. An important caveat to note is that, DCA or otherwise, it is essential to diversify your investments into broad markets rather than a small basket of securities that would concentrate risk. Also, ensure that you have a sufficient time horizon to ride out market volatility. Cost of investing should also be kept as low as possible to ensure it does not eat into the returns of the fund.

Disclaimer:

While every reasonable care is taken to ensure the accuracy of information provided, no responsibility can be accepted for any loss or inconvenience caused by any error or omission. The information and opinions expressed herein are made in good faith and are based on sources believed to be reliable but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. All investments carry risk. Expressions of opinions or estimates should neither be relied upon nor used in any way as indication of the future performance of any financial products, as prices of assets and currencies may go down as well as up and past performance should not be taken as indication of future performance. The author and publisher shall have no liability for any loss or expense whatsoever relating to investment decisions made by the reader.