Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

If you have started your investment journey and are wondering how investment returns should be calculated, we have put together some materials that hopefully will help you understand returns better. Let’s start off with some basics.

Simple Investment Return

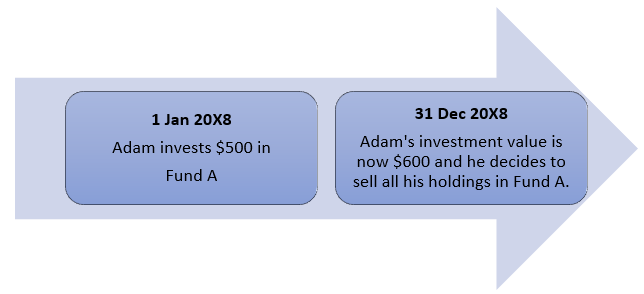

Adam invested $500 in Fund A. 1 year later, he sold all his holdings in Fund A and realised $600 proceeds. What was his total return?

We know that Adam invested $500 and took home $600 when he sold his investment. We can then derive the rate of return as below:

Fantastic, Adam has earned 20% return from this investment!

Investment returns incorporating additional investment or withdrawal

Investment return calculations become more complicated when there are cashflows involved. Cashflows refer to money flowing in or out from the investment portfolio, for instance: additional investments, dividends received or even withdrawals. We will illustrate this concept with two scenarios below.

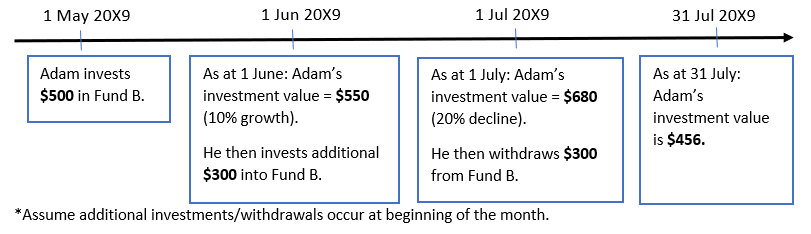

Scenario 1:

Adam is back again with his $500, now he decides to invest in Fund B. Below shows his investment journey.

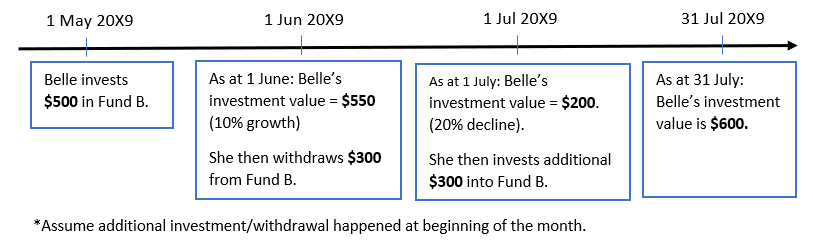

Scenario 2:

If you haven’t already noticed, while Adam and Belle both invested in the same fund (Fund B) over the same period (1 May – 31 Jul), their final investment values as at 31 July vary greatly, which is mainly due to the different timing of their withdrawals and top-ups. So how do we calculate their returns?

Money-Weighted Return (MWR)

Money-Weighted Return (MWR) can be used to calculate Adam’s and Belle’s investment return (in percentage) over their entire investment period.

With a financial calculator or Excel, we compute the MWR as below:

Adam’s MWR for the 3 months = -7.35%

Belle’s MWR for the 3 months = 24.91%

MWR captures the joint effect of the actual investment performance and the impact that cashflow timing (in/out) has on the investment returns.

Consequently, due to different cashflow timings, Adam made a loss of 7.35% and Belle successfully gained 24.91% from Fund B. This shows that cashflow timing can greatly impact the individual investor’s returns.

Is Fund B a good fund?

Carey knows both Adam and Belle. She is interested in fund B as well. She asked both for advice on Fund B. Adam doesn’t like the fund because he lost money, but Belle had positive feedback about the fund’s performance. Carey is puzzled and wants to know how she can evaluate the fund’s performance more accurately. Time-Weighted Return (TWR) is the measure that can do this for us.

What is Time-Weighted Return (TWR)?

TWR captures the rate of return of the investment independently of the individual’s cashflows decisions. In short, it measures the investment performance only, without being influenced by investor cashflows.

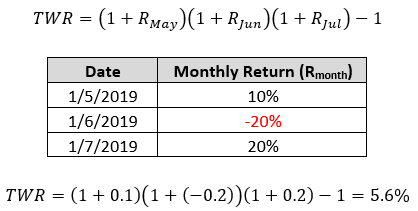

Going back to Fund B, if we calculate the TWR for both Adam and Belle, we will obtain the same answer, as TWR calculation is not driven by the additional investment or redemptions.

TWR for Adam and Belle can be calculated as:

Positive or Negative returns?

Interestingly, because of the computational differences, there is a possibility that investors might see a positive TWR, but their dollar returns or MWR is negative, or vice versa. This is not uncommon as only in the absence of cashflows within the investment period will MWR be equal to TWR.

Why MoneyOwl chooses to use TWR?

The two returns, MWR and TWR, clearly measure different dimensions of the investment performance. As you have entrusted us with your savings and we commit to help you stay invested for a positive investment experience, it is our responsibility to present your investment returns in the most meaningful way possible. The TWR is a more concise measure of the actual performance of $1 in your portfolio, without considering the effects of cashflows. Hence, it would be a more accurate measure of the value MoneyOwl brings to you.

TWR is also recognized as a standard measure in fund management industry. With the objective to encourage fair and transparent investment performance reporting, the Global Investment Performance Standards (GIPS®) was introduced in 1999 and TWR is the required measure for investment performance under GIPS standards. Currently, the GIPS standards administered by CFA Institute are considered industry best practice for investment performance presentation and are adopted by investment management firms globally. Therefore, TWR serves as a consistent measure for performance comparisons between various funds.

*Adam, Belle and Carey are hypothetical investors

*Fund A, B and C are hypothetical funds.

The author, Law Shiang Rou, was a client adviser at MoneyOwl Pte Ltd.