Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

How Much Monthly Income Do You Need During Your Retirement

If you have ever tried to figure out how much you need to have to retire in Singapore, you’ve most likely been confounded by one of the most basic yet most difficult question to answer – how much monthly income do you need during your retirement? This requires one to imagine what life is going to be like when we stop working – will we be globe-trotters, happy-go-lucky shoppers, active-agers or home-bounders? Couple that with inflation rates and years in retirement (how long you expect to live till), it is no wonder many give up trying to figure it all out.

We have some surveys that can help to shed some light:

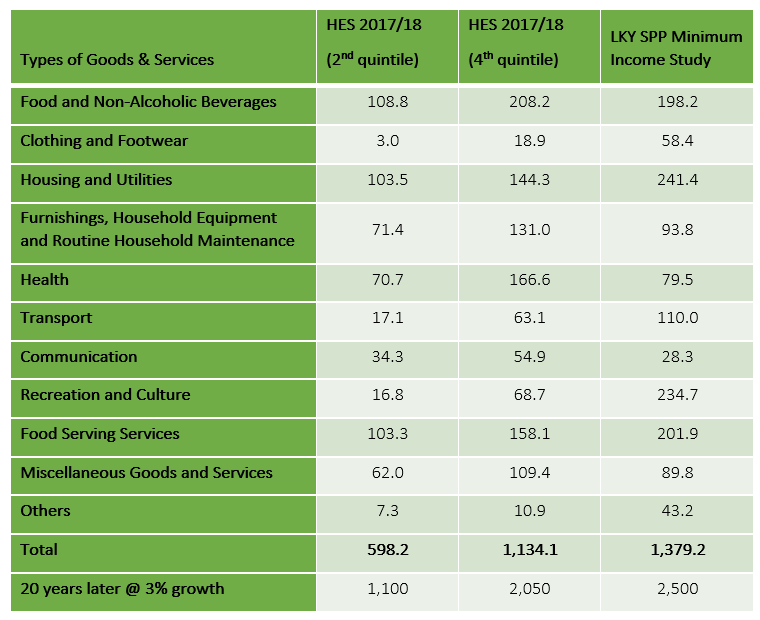

- The latest Household Expenditure Survey (HES) 2017/18 included information on how much retiree households in Singapore spend. Based on the second quintile (20th to 40th percentile, or lower-middle segment), this spending is about $600 per month today.

- In the 4th quintile (or upper-middle segment) of retiree households in the HES 2017/18, spending is about $1,130 per month.

- The recent Lee Kuan Yew School of Public Policy (LKYSPP) study among 100 focus group participants, most of which were aged 55 and above, across a diverse range of backgrounds found out that a single elderly person would need $1,379 per month for their “basic needs”. By basic needs, it went beyond subsistence living to include also having enough to enable one to thrive in one’s golden years.

To find out what made the differences among the three estimates, let’s compare across the broad categories of goods and services. As per the table below, the categories that saw the largest variance are clothing and footwear, transport, recreation & culture, and others (which include holiday expenses). Understandably, to lead a more meaningful retirement, focus group participants in the LKYSPP study agreed that more money would be needed to support participation in social and recreational activities.

However, when we compare how much a single retiree in the upper-middle household (which represents the 60 – 80th percentile of our retirees) spent in retirement, about $1,150 per month, I can’t help but wonder if there is indeed a gulf between expectations and reality. It appears that while there are aspirations to socialise and participate in recreational activities, most retirees end up spending more on telecommunications (why travel when I have the world at my fingertips?) and on healthcare, underscoring the fact that while Singaporeans are living longer, they are not necessarily living healthily.

Multiple Layers of Retirement Income

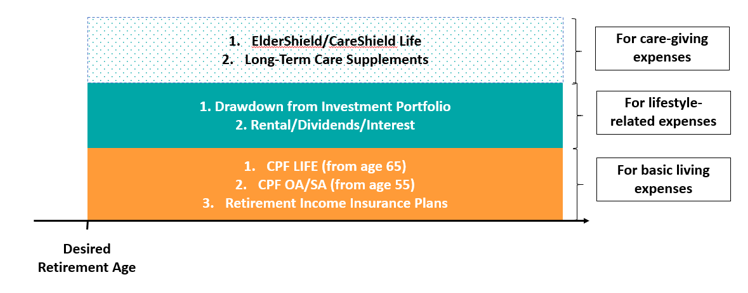

Amidst the complexities surrounding how much one needs for retirement income, it is probably useful to create multiple streams of income to address different needs in retirement much like a kueh lapis. Each layer of income has features to cater to your expenditure patterns in retirement and correspondingly will be supported by suitable financial instruments in the market.

Unlike an accumulator, a retiree faces a complex set of risks. As the retiree no longer has an income flow, it is crucial to guard against excessive spending in the early years of retirement that could lead to savings depleting prematurely especially as we are living longer. With retirement stretching over a 20 to the 30-year period, simply leaving assets in the bank will not do as wealth is being eroded by inflation, hence there is a need to invest to keep pace with inflation. However, this comes with investing risk as the retiree will need to deal with the ups and downs of the market. Lastly, as one grows older, poor health may cause retirement funds to be depleted even faster.

A simple yet effective design of future income stream to address all these issues would be made up of three parts – i) the safe retirement income floor to cater for your basic living expenses, ii) a secondary layer of income to cater for more lifestyle-related expenses, and iii) a third layer of income that covers your caregiving expenses in the event of severe disability.

Layer 1 – Safe Retirement Income Floor from your CPF Nest Egg and Retirement Income Insurance Plans

The first layer of retirement income is for your basic expenses. This would refer to how much you minimally need for basic food, transport, utilities and healthcare. In planning, this would be called the safe retirement income floor and forms the base of your retirement income. As this is meant to sustain the day to day living in your retirement, this layer of income needs to be regular, stable and last for life. A lifelong income stream guards you from outliving your savings.

Referring to the surveys above, the average safe retirement income floor for most retirees would be somewhere between $700 to $1,500 per month today. Now if this number sounds familiar to you, it should. It is how much payout CPF LIFE would provide for someone who has set aside a retirement sum between the Basic and Full Retirement Sum. Given that CPF LIFE provides a stream of stable lifelong income, it is the perfect candidate to form any retiree’s safe retirement income floor.

However, should you choose to retire before your CPF LIFE payouts start, your source of safe retirement income floor would be different.

For example, retiring before 55 years old would mean most of your income would come from your cash or near-cash instruments like Singapore Savings Bonds or fixed deposits. A post-55 retirement would mean being able to withdraw excess CPF savings in the Ordinary and Special Account after setting aside your retirement sum in the Retirement Account. Apart from the above, payouts from retirement income insurance plans can also form part of the safe retirement income floor. These instruments provide some guarantees in either capital, returns or payouts thus providing the certainty suitable for a safe retirement income floor.

Layer 2 – Additional Income for Lifestyle-Related Expenses from Investible Assets

The second layer would be made up of income from investments. Although not many people can afford investment properties for rental income, it is possible for many of us to save and invest regularly through a disciplined investment plan that will help us grow a second nest egg which we can draw on for additional income during retirement while protecting our wealth from being eroded by inflation.

The most important source of your retirement funds will come from your income, specifically your monthly cash surplus (i.e., savings after deducting expenses from monthly income). This means having the discipline of keeping to a budget or paying yourself first every month. If you have never budgeted or have no clue how much you can save, a quick rule of thumb would be at least 15% of your monthly salary plus 50% of your annual bonus.

What’s more, if you have been working for some time, you would have also accumulated some investible assets which could be sitting in your bank, low interest fixed deposits, endowment policies, bonds, shares, unit trusts, investment property(ies) and not forgetting your CPF accounts. All these form part of your investible assets which can be deployed for your retirement planning after setting aside resources for your children’s education, if any, and emergency funds (3 to 6 months in cash is recommended).

With the knowledge of your current financial situation, it is now a matter of using a reasonable rate of return to project how much these current assets and surplus would accumulate to by the time you reach your desired retirement age.

But that’s not the end of the story. The gap in retirement planning in Singapore today is that it is still largely catered to the demands of wealth accumulators. These solutions while suitable for building wealth leaves little ideas on how a retiree can decumulate their wealth to get a sustainable and reliable income stream when they finally decide to stop working.

While investments are an efficient way of providing an additional stream of income, investing in retirement is subject to a sequence of returns risk. Drawing too much income from your portfolio when the market is down could deplete your nest egg quickly; whereas for accumulators who do not draw down their portfolio, whether the market goes up or down in their investing journey does not matter, as long as overall the market goes up over their entire time horizon. We, therefore, need to have a sensible withdrawal rule or invest in a solution that is specially designed to give us an income stream in a simple fuss-free manner. With this in place, the investment component will provide the flexibility and growth needed to boost your income according to your lifestyle requirements.

Layer 3 – Contingency Income for Caregiving Expenses if Severely Disabled

The third layer of “contingency” income will come in handy if you need caregiving in your old age. While we hope that our golden years will be smooth sailing, statistics from the Ministry of Health tell us that 1 in 2 healthy Singaporeans aged 65 today are expected to be severely disabled in their lifetime. What this means is that there is a 50% chance that what you need for your retirement income could be even more to pay for caregiving expenses, such as for a family member to stay home to look after you; a trained domestic helper or long-term stay in a home-nursing facility. These costs could add up to more than $3,000 per month depending on the level of care required.

Because severe disability may not affect all of us, this third layer of income would be most efficiently addressed through national insurance schemes like ElderShield/CareShield Life and its accompanying supplements. Such plans provide a monthly income benefit if you are unable to perform more than 2/3 out of 6 Activities of Daily Living (i.e. eating, bathing, toileting, dressing, transferring and moving around).

Since October 2020, CareShield Life was rolled out to gradually replace ElderShield to provide a higher payout of $600 per month for life. The payout will also increase by 2% per year until the policyholder reaches 67 years old or makes his/her first claim. Singaporeans and Permanent Residents born 1980 or later were auto-enrolled into CareShield Life in 2020 or will be when they turn 30 years old from henceforth. For those born between 1970 and 1979, CareShield Life will be extended to you sometime end of 2021.

If you are concerned that there are still gaps in this area, you can also enhance the benefits through supplements offered by private insurers. The premiums of these plans can be paid through your MediSave, up to $600 per year. Besides, some retirement income insurance plans have also built-in such benefits into their income payout to help mitigate the healthcare risk faced by retirees.

Making wise decisions and making them easy

At MoneyOwl, we believe in the importance of living life to the fullest in the present as much as we believe in planning for the future. A wise plan is one that properly balances both. MoneyOwl exists to help our clients make that wise decision.

Having the retirement of your dreams takes planning, but this process can sometimes leave us overwhelmed with the multitude of options. With Fullerton MoneyOwl WiseIncome, we have specially designed a solution for you to build your stream of passive income to complement CPF LIFE. This way, we make wise decisions easy for everyone.

Lena Teng is the Lead, Solutions Team at MoneyOwl.