Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Find out how insurance protect us against the risk of losing our income

Risks are part of our daily lives. We risk waking up late for work, we risk contracting a virus when we’re out and about, we risk losing our jobs in a market downturn, we risk our marriage failing, we risk our children going astray, we risk losing our money in poor investments, we risk running out of money before we run out of breath…

The list goes on. But if we were to only focus on the risks we might face every moment of our lives, we would probably end up too scared to even get out of bed.

Ironically, even though we live through risky situations all the time, the only time we really think about this seriously is when we talk about insurance or investments. We buy insurance to protect us against the risk of losing our income if we are unable to work due to death, disability or illnesses. Lately, there has also been rising interest in insurance for retrenchment too.

We invest because we don’t want to risk not having enough money for our life goals, but even as we invest, we also risk losing our money if we choose poor investments, follow investment strategies that are not backed by robust research and go for get-quick-rich schemes. Hence, it becomes more important to think about the promised returns vis-à-vis the risk you bear on that investment.

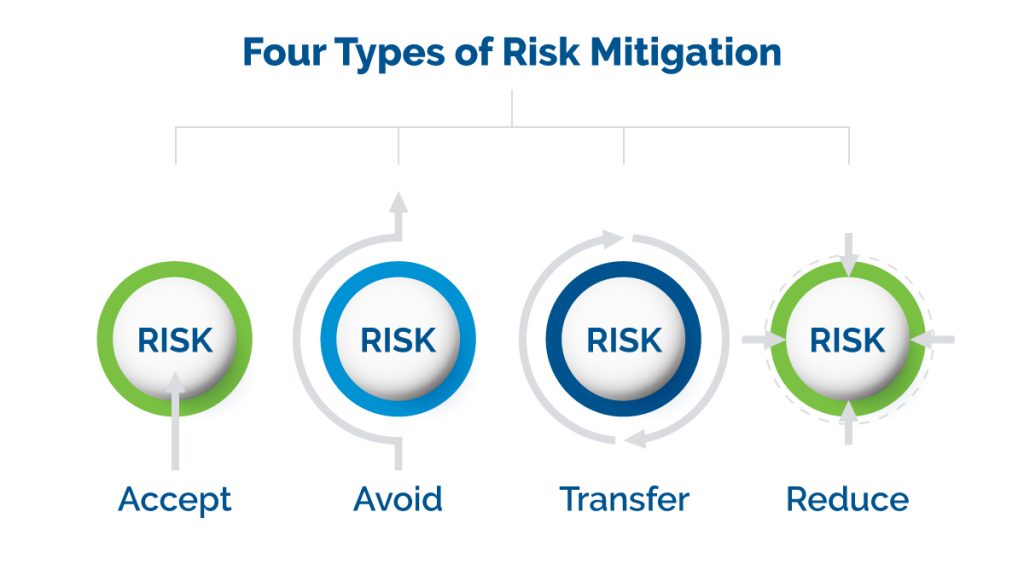

But if we were to go back to my introduction, you’d realise we bear a lot more risks in our lives which does not necessarily require either insurance or investment. In fact, in the scope of risk management, there are four approaches you can adopt to mitigate risks in your life.

Source: MHA Consulting (https://www.mha-it.com/2013/05/17/four-types-of-risk-mitigation/)

For some risks, you can choose to just accept it. In the case of waking up late for work, depending on the nature of your work, it is probably acceptable because you can always work later to make up for the time lost.

For some risks, you can choose to avoid it entirely. If the fear of catching a virus is too much for you, you can always avoid going out and just stay home. If you are afraid of being heart-broken from a failed marriage or seeing your children go astray, you can choose not to ever get married and form your own family.

For some risks, you can choose to transfer them to another entity. As Singaporeans are living longer and more people are concerned about outliving their savings, buying an annuity plan like CPF LIFE gives you the assurance of a lifelong income even when your underlying premiums have been paid out in full. Unfortunately, you cannot transfer the risks of making poor investment decisions to someone else. If you don’t want any risks on your investments, you usually pay the price of having lower returns and risk losing purchasing power to inflation.

For most risks, you can choose to reduce them through conscious effort on your part.

- Sleep early and set an alarm to reduce the risk of waking up late

- Wear a mask when you go out to reduce the risk of contracting viruses

- Set aside sufficient emergency funds in good times to reduce the risk of bankruptcy should you lose your job

- Spend quality time with your loved ones to reduce the risk of failed relationships

- Follow the principles for successful investing to reduce the risk of losing money through investments

- Integrate CPF LIFE as part of your retirement plan to reduce the risk of outliving your retirement savings

At MoneyOwl, we do more than just advise our clients about what types of insurance to buy or how they can maximise their investment returns (we don’t!). We help our clients live their life meaningfully by balancing between what matters to them and keeping a watch out on what could go wrong with their plans.

This underlies how we approach solutioning for our clients by looking at both sides of the coin.

- We recommend a salary-based model for our advisers because we do not want to risk commissions getting in the way of conflict-free advice.

- We recommend low cost term insurance because we do not want you to risk being inadequately protected despite paying a lot for insurance.

- We recommend market-based investment strategies because we do not want to risk placing our bets on investment strategies that promise outperformance but are unable to consistently deliver in the long run.

- We recommend a lifestyle approach to comprehensive financial planning because we do not want to risk turning you away from acting because the recommendations are unrealistic.

I will always remember this conversation I had this with a young gentleman. I was sharing with him in the context of financial planning, that he should invest through our portfolios of low-cost globally diversified portfolios to make his money work harder for him or he might risk not meeting his goals.

He was adamant that he could not trust fund managers to manage his money and he would be better off investing the money in himself through his business. He had been relatively successful in his start-up thus far so there was certain bias in his thinking. As such, I didn’t try to debate his line of thought, instead I told him, “What you need then is not investment, but insurance.”

You see, what this man may not realise is that because he is the “key man” to the success of his investment, i.e. his business. If something bad were to happen to him, his investment may fail and his family suffers. He needs then to transfer this risk to the insurance company.

As your appointed financial adviser, we don’t preach the bells and whistles. We focus on giving our clients the confidence of knowing that we got your backs covered in everything we do.

Author: MoneyOwl’s Solutions Team