Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Hospitalisation insurance is one of the most important policies everyone should have. Without it, one could be easily saddled with huge medical bills that would cause havoc to his/her financial life. With the advancements in the medical industry, many conditions are now treatable with lesser side effects and provide a faster recovery. While all these developments are good, the medical bills may not be as appealing. Thankfully, having MediShield (Life) and the right Integrated Shield Plans (IPs), these large bills can be taken care of.

This article is a continuation from Part 3: Integrated Shield Plans – Uncovered Problems and Proposed Solutions.

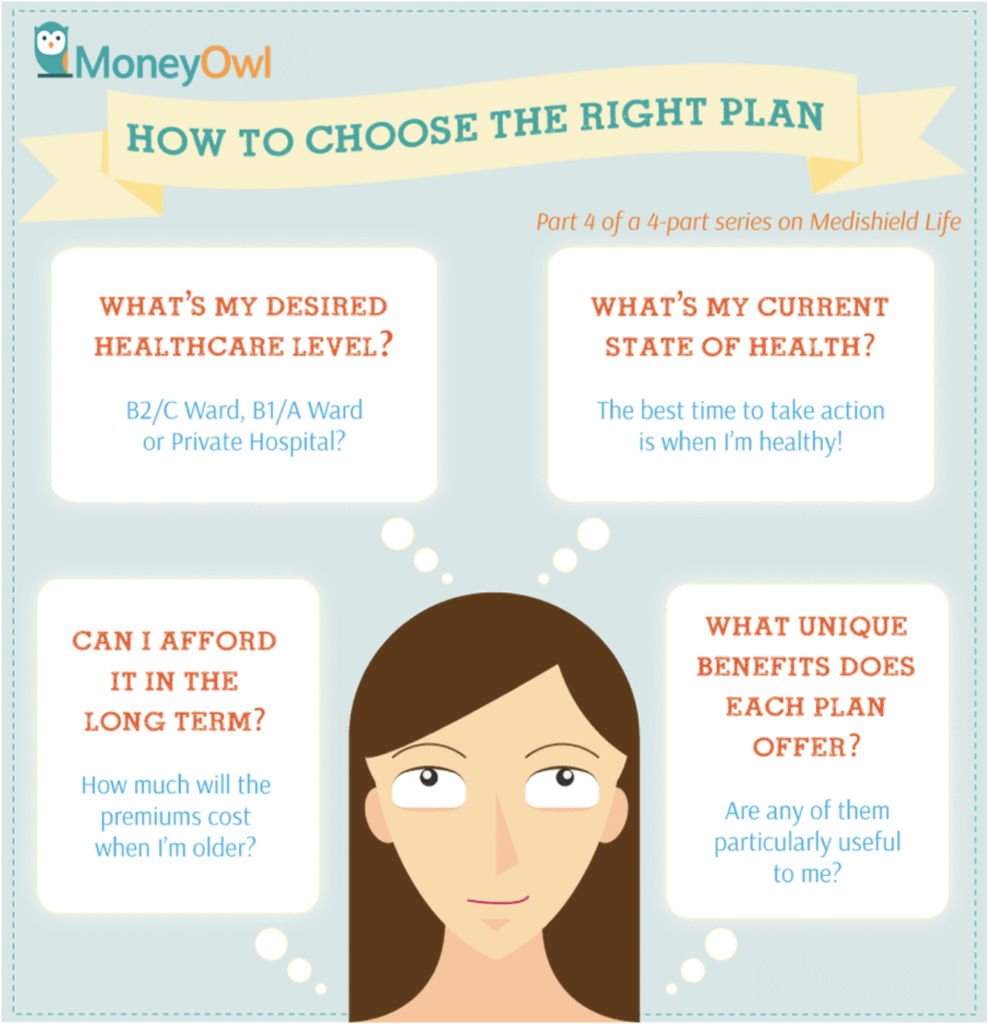

But how does one choose the right plan? There are no straightforward answers but the following provides you with 3 key considerations to use as a guide when choosing a plan that best suits you and your family’s needs.

Key Considerations:

1. Desired Level of Healthcare

In which ward class do you intend to be warded in the event of hospitalisation? Some do not mind subsidised wards (i.e. B2/C wards) while others prefer a more comfortable environment with more amenities such as air-conditioning, television and a personal bathroom in their wards (i.e. A/B1 wards). There are also those who do not mind buying pricier plans for private hospitals so they can receive treatment without the long wait and have the privilege of choosing their doctors in the private practice who are perceived to be better.

Having the right plan is important because you will end up paying much more if you stay in a ward class that is higher than your entitlement.

Based on the MediShield Life Review Committee Report, 70% of policyholders who have IPs for Class A wards actually end up staying in a ward of lower class than their entitlement while another 10% of policyholders end up staying in private hospitals (higher class ward). This could be because people prefer having options in the event that they must go to a private hospital.

2. Long Term Affordability

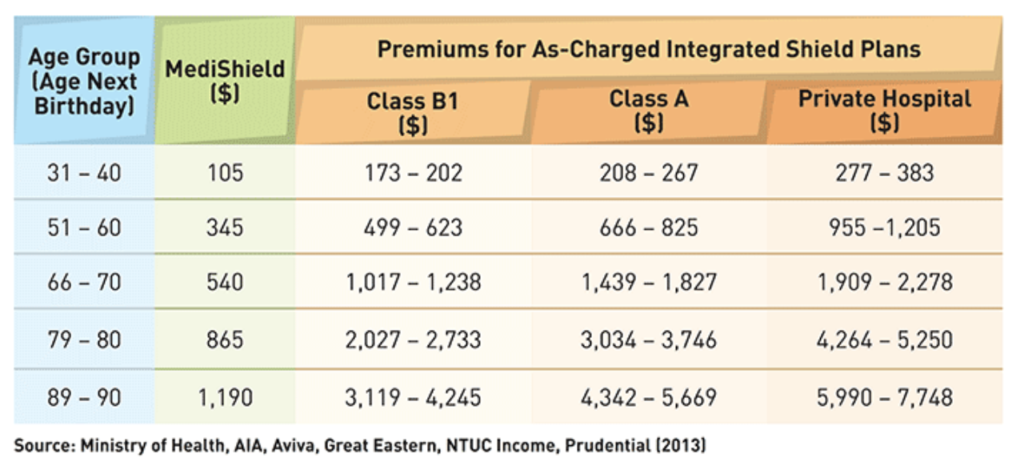

Because premiums for IPs are based on the age it was attained, therefore premiums increases with age (see table below). Do note that these premiums are not fixed and are subject to increase in the event of medical inflation and claim experience similar to 2008 and 2013.

Premiums may be affordable now, but one should really consider whether it would still be within his/her means when he/she reaches 60 – 90 years old.

However, having said that, the price difference between premiums for higher ward classes are not too significant when one is younger (especially below age 40) and can be paid via Medisave. Hence, it is understandable why people tend to over-insure themselves when at a younger age and downgrade their policies later on when it gets more expensive.

3. State of Health

MediShield and IPs are offered based on good health.

If one is in the pink of health, he/she has the option to choose between IPs and even switch plans across the approved insurers without any loss of coverage. However, if his/her current plan is below the desired level of healthcare, it is advisable not to delay a change for too long reason being that our health can take an unexpected turn due to unforeseen illnesses or accidents which would make applying for any insurance more challenging.

However, if one’s health factor is not as good, his/her options are more limited. Sticking with the current insurer would be advisable because one would be subject to fresh underwriting which may not be favorable to him/her when switching insurers. The advantage of downgrading within the same insurer is that any pre-existing conditions that are currently covered will remain the same under the new plan. Similarly, when upgrading within the same insurer, the pre-existing condition would be covered up to the benefit level of the previous plan.

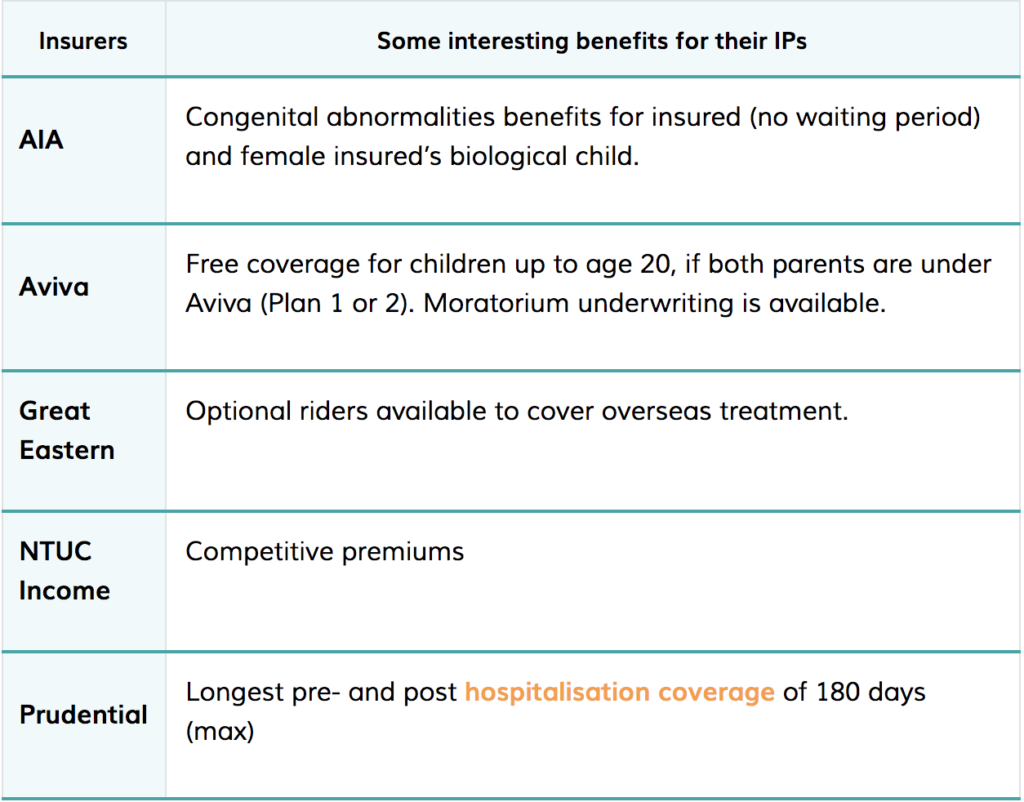

4. Unique Benefits

There are 6 private insurers that offer IPs of which each has its own unique proposition. By and large, their key benefits are similar with some additional benefits that may appeal to certain groups of people.