Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

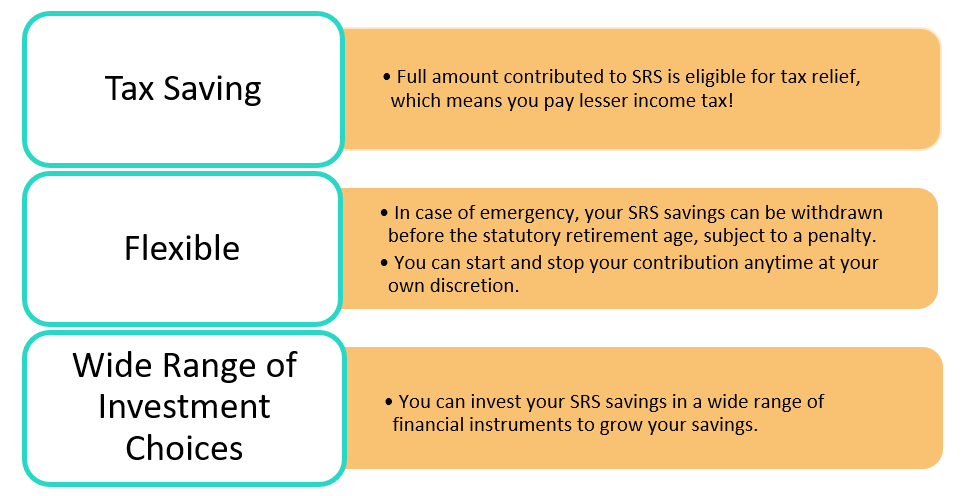

What is Supplementary Retirement Scheme (SRS)?

SRS is a voluntary scheme to encourage individuals to save for retirement, over and above their CPF savings. Contributions to SRS are eligible for tax relief and only 50% of the withdrawals from SRS are taxable at retirement. By spreading your SRS withdrawals over a period of 10 years, you can minimise or might not even need to pay any tax on your withdrawals. The amount of tax you can save depends on your annual taxable income:

| Annual Taxable Income | Tax payable WITHOUT SRS contribution | Tax payable AFTER $15,300 SRS contribution | Tax Savings |

|---|---|---|---|

| $40,000 | $550.00 | $94.00 | $456.00 |

| $80,000 | $3,350.00 | $2,279.00 | $1,071.00 |

| $120,000 | $7,950.00 | $6,190.50 | $1,759.50 |

| $160,000 | $13,950.00 | $11,655.00 | $2,295.00 |

For those new to SRS, it may be a bit hard to grasp. Not to worry, here is a summary with all the important information you need to know.

What’s the catch?

Penalty for early withdrawal

As its name suggests, SRS is a scheme to encourage saving for retirement. Therefore, for withdrawals made before the statutory retirement age, a 5% penalty based on the amount withdrawn will be imposed. In addition, the full amount withdrawn will be subject to tax. The statutory retirement age is currently being set at 62 years old and is expected to increase to 63 years old in 2022. Your statutory retirement age for penalty-free withdrawal is based on the statutory retirement age prevailing at the time of your first contribution.

Cap on SRS contribution and personal income tax relief

The maximum amount that you can contribute annually to your SRS is capped at $15,300 for Singapore Citizens and Permanent Residents and $35,700 for foreigners. However, do note that there is a total personal income tax relief cap of $80,000 per year. This means that if the total amount of your personal tax reliefs for the year is already more than $80,000 (including CPF relief, parents’ relief, working mother’s child relief), your contribution to SRS will not be eligible for further tax relief.

*Source: IRAS

What should you do with your SRS savings?

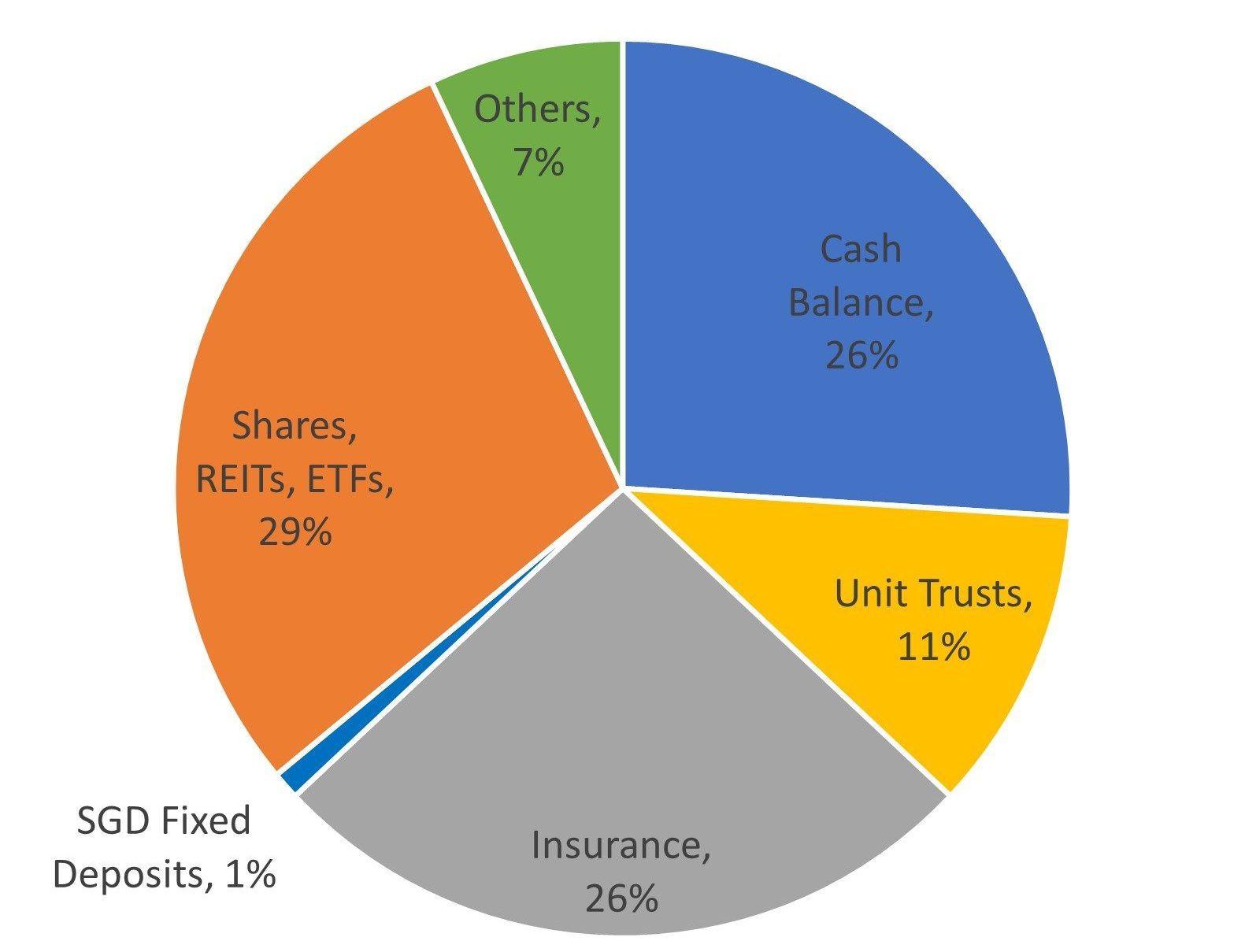

SRS is no doubt a useful tool to put aside extra money for your retirement as well as earn tax benefits. However, according to December 2020 data from Ministry of Finance (MOF), 26% of SRS funds stays as cash, a drop of 4% from the year before. It is good news that more people are learning to optimise their SRS savings, as should you.

What Do People Do With Their SRS Funds?

*Source: Ministry of Finance (MOF)

Did you know that monies parked in your SRS account as cash only earns 0.05% p.a. interest? Not only are the returns minimal, your savings may get eroded by inflation. If you’ll like to make your SRS money work harder for you, you can invest your SRS funds in a wide range of financial instruments such as unit trusts, insurance, fixed deposits, stocks, Singapore Saving Bonds and so on. For a novice investor, researching various financial instruments and committing your hard-earned money into investments can be time-consuming and intimidating. If sleepless nights are not what you are after, then these are two options that can help:

1) Retirement Income Insurance Plans – Generating fixed income stream for you

Picture this: You are retired and enjoying an extended holiday at your dream destination. At the same time, you’re getting a monthly “salary” just like when you were still working. How fantastic is it? Without having to worry about market ups and downs, rain or shine, retirement income plans are designed to pay out a stream of income (guaranteed + non-guaranteed portions) to you, so that you can pursue the comfortable retirement life you deserve. The table below shows 2 different retirement income plans approved under SRS: Profile: Male, aged 45

| SRS Products | NTUC Income Gro Retire Flex | Manulife RetireReady Plus III |

|---|---|---|

| Single Premium | $50,000 | $50,921 |

| Income Payout Begins at | Age 65 | Age 65 |

| Monthly Guaranteed Payout | $248.67 | $250.00 |

| Total Monthly Payout* | $669.15 | $650.08 |

| Payout Duration (Years) | 20 | 20 |

| Total Payout Benefits* | $160,596 | $156,019 |

| Yield at Maturity* | 3.92% | 3.74% |

*Non – guaranteed payouts and yield at maturity are based on illustrated yield of 4.25% p.a

Taking Manulife Retire Ready Plus III as an example, the plan allows you to receive an income stream that comprises both guaranteed and non-guaranteed components. As every individual has a unique set of needs, these plans are customisable to take into consideration your desired retirement age and how long you want your income to last.

2) Low-cost Investment Portfolios – Growing your retirement egg with Nobel Prize winning solutions

We all know the wisdom in not putting all our eggs in one basket. Having an investment portfolio that is diversified across different countries, sectors and even instruments can help you achieve the returns you need according to your risk appetite. You should also pay attention to the fees involved, as high sales charges, expensive management fees can eat away your returns. MoneyOwl is diligent at keeping cost low for clients and at the same time maintaining a broadly diversified global investment portfolio. Instead of constantly trying to time the market, which results in higher transaction costs, we recommend staying invested as a more reliable approach to achieve the desired returns – as validated by many empirical studies. Depending on your risk appetite and retirement planning needs, we will be able to recommend the right investment portfolio for you.

| Portfolio | MoneyOwl Balanced Portfolio | MoneyOwl Equity Portfolio |

|---|---|---|

| Risk/Return level | Mid Risk and Return | High Risk and Return |

| Asset Allocation | 60% Global Equities + 40% Global Bond | 100% Global Equities |

| Projected Annualised Return* (Net of fees#) | 5.6% | 6.7% |

If you are a 45-year-old and start a $20,000 investment in MoneyOwl Equity Portfolio today, by the time you turn 65, the projected value of your portfolio could be $73,167 (Based on 6.7% p.a. net-of-fees projected return).

*Projected returns are based on the historical indices returns of Dimensional Global Core Equity Index, Dimensional Emerging Markets Adjusted Large Caps Index & FTSE World Government Bond Index 1-5 Years (hedged to SGD) from January 1994 to December 2020. Please note that past performance is no guarantee of future results.

*Projected Annualised Returns are net of estimated total expense ratio (TER), custodian/platform fees, and advisory fees. For more information on MoneyOwl’s portfolios projected return and fees structure, please visit: https://www.moneyowl.com.sg/invest

Still feeling a bit lost? We’ve put together two simple infographics breaking down what is Supplementary Retirement Scheme (SRS) is all about.

Click the links below to find out more!

Or click here to get a recording of our webinar “Supplementary Retirement Scheme (SRS) – What You Need to Know and How to Maximise It”.