Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Find out more about Insurance Policies and The Impact of The Downward Revision in Financial Planning

On 2 June 2021, the Life Insurance Association of Singapore (LIA) announced that the cap for participating policy illustration will be lowered to 4.25% p.a. from its current 4.75% p.a. in view of the sustained low-interest-rate environment. These new rates will have to be implemented in participating policies sold from 1 July 2021. This is to give policyholders a more realistic view of the returns to expect when they buy a participating policy from an insurance company. If you currently hold a whole life, endowment, or retirement income policy or are thinking of getting one, you may wonder how this will affect you. Read on as we break down the details for you.

What are participating policies?

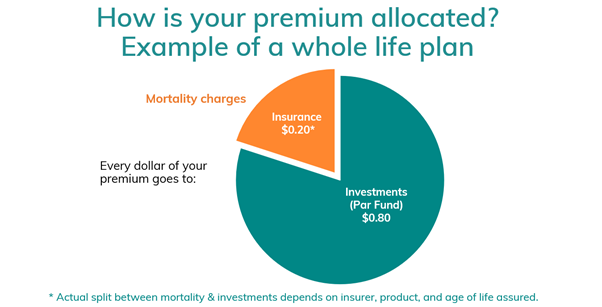

Participating policies are life insurance policies that allow policyholders to participate or share in the profits of the participating fund of the insurer. When you pay the premiums for your whole life, endowment, or retirement income plans, a small portion of your premiums will be set aside to cater for the protection benefits provided under the policy. The balance will then be pooled together with other policyholders in a participating fund (par fund for short).

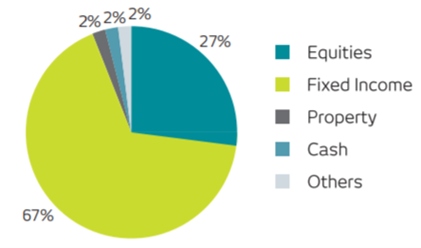

The par fund invests in a range of assets such as government and corporate bonds, equities, property, and cash to generate an investment return. Typically, insurance companies adopt a more conservative approach by allocating about 30% of the fund into equities and 70% into bonds. The returns you can expect to get is dependent on the investment return, claims experience, and level of expenses incurred by the fund. This return would typically be made up of a guaranteed and non-guaranteed component.

The non-guaranteed component in the form of bonuses is determined on an annual basis. Once these bonuses have been declared, they are considered ‘guaranteed’ thus the insurer cannot subsequently reduce or take them away upon the claim.

As a policyholder deciding whether to buy a participating policy, however, you will probably need some idea of how your investment will pan out over the long term. As such, illustrations that show how the cash value in your policy will grow and accumulate over time based on a set of standardised projected returns, upper and lower limit, was necessary.

How are these projected returns determined?

LIA reviews these caps annually to ensure its ongoing relevance and appropriateness after considering recent and future economic and market conditions, the typical asset class mix that par funds invest in and the projected long-term returns of each asset class. A revision will only be called for when the realistic range of projected investment returns have shifted materially. The last time the projected returns have changed was in 2013, when it was reduced from 5.25% p.a. to 4.75% p.a.

A typical asset allocation mix of a par fund

Source: Tokio Marine Participating Fund Update

Using the long-term historical returns of global indices MSCI AC World and Bloomberg Barclays Global Aggregate Bond to represent equities and bonds respectively, a portfolio with 30% equities and 70% bonds would have returned 4.2% p.a. after deduction for fund expenses between the period of 2007 to 2020 which covers the two major financial crises we have experienced. These projected returns are quite fair and realistic.

Nonetheless, LIA had stated categorically that these are just meant as illustrations and do NOT represent the actual upper and lower limits of the performance of the par fund. The annual bonuses declared will still be determined by the actual performance of the par fund year on year.

How do these illustrated returns compare to actual par fund performances?

Based on annual returns submitted to MAS, we were able to put together the following table that shows the actual par fund performance of the various insurance companies in Singapore over the last 5 years.

While the actual performances appear to have done better than the illustrated rates, insurance companies are hardly ever going to give you these exact returns year-on-year for the following reasons:

- Not all your premiums are invested as a portion is used to pay for mortality charges or the cost of insurance (see above).

- Shareholders of the insurance companies take a 10% cut of the profits, i.e. for every $1 that shareholders receive, at least $9 must be paid out as bonuses to policyholders, serving as some form of protection for you

- Reserves to be set aside to support solvency of the fund and future bonus payments. As markets do not move up in a straight line, reserves have to be created in good years so that insurance companies can continue to make good of their annual bonus regardless of market conditions. This is also known as bonus smoothing.

- Expenses are deducted from the par fund to pay for distribution costs (commissions paid to agents), administration costs, and investment management fees.

For example, based on a sample product illustration using the latest caps, a standard 20-year endowment/savings plan will give you a net projected return of 3.22% p.a. if the par fund returns 4.25% p.a. and 2.17% p.a. if the par fund returns 3% p.a. The guaranteed return at end of 20 years is 0.75% p.a. Perhaps it is time to change the notion that participating policies are good for guaranteed returns. You might be better off using Singapore Savings Bonds for stability without sacrificing flexibility.

This also underlies another trend. In today’s economic environment of sustained low-interest rates and greater regulatory requirements for insurance companies to match their commitments to their capital structure, it is time to rethink using insurance products for wealth accumulation. As our retirement years stretch due to increasing life expectancy and we face conflicting use of our financial resources, we will need higher expected returns to achieve our goals and sustain our retirement income. Having said that, insurance will always play a very important role in protecting us from the loss of income and thus forms the foundation of all our financial plans.

How will I be affected if I am an existing policyowner of a participating policy?

As mentioned by LIA, your actual returns are still determined by the actual performance of the par fund and is not represented by the illustrated returns. Insurers are likely to try and honour these bonus projections, especially in the short term. However, over time, to maintain solvency and overall sustainability of the par fund, they may start to gradually reduce bonuses during times of market stress as expectations are already being set at a lower level of return.

This is also why there is no need to rush to commit to a participating policy before 1 July 2021 if you have not decided to do so. Whether you are committed to a policy with higher or lower illustrated par fund returns, all policyholders’ realised return will be dependent on the par funds’ level of sustainable return and solvency considerations.

If you still have concerns about this change, we encourage you to speak to our fully salaried client advisers who will be able to advise you on whether your current policies still play a role in your financial plans and whether it makes sense to streamline them to give you higher returns. You can also watch our webinar on par insurance policies through filling up the form below!