Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

While there are many ways to plan for your retirement, examine whether replacing CPF LIFE with an insurance retirement plan is a good idea

If you have been searching for ways to plan for your retirement, you would probably have come across many insurers promoting their retirement income or annuity plans. With such plans, you either fork up a lump-sum or pay regular premiums over a period of time, in return for monthly payouts over a fixed number of years or for a lifetime.

Often touted as having more features and flexibility, some feel that such insurance retirement income plans are better options than sticking to the CPF LIFE annuity scheme. As a result, some of us might have considered using our existing insurance retirement income plan or purchasing a new one to replace CPF LIFE by applying for an exemption from setting aside the applicable retirement sum when we turn 55 years old.

This means that instead of receiving payouts from CPF LIFE using our retirement sum as premiums, we are opting to use our cash or CPF savings through CPFIS savings to get lifetime payouts from our private insurance retirement plans.

But are retirement plans from private insurers really a better deal than our national annuity scheme? In this article, we will examine whether replacing CPF LIFE with an insurance retirement plan is a good idea based on these three criteria:

- Returns

- Insurance Benefits

- Flexibility and Control

Returns

In this test, we pit the returns of an insurance retirement plan (Aviva MyLifeIncome II), one of the more popular retirement income plans in the market, against that of CPF LIFE, to see which gives us the most out of every dollar we have saved.

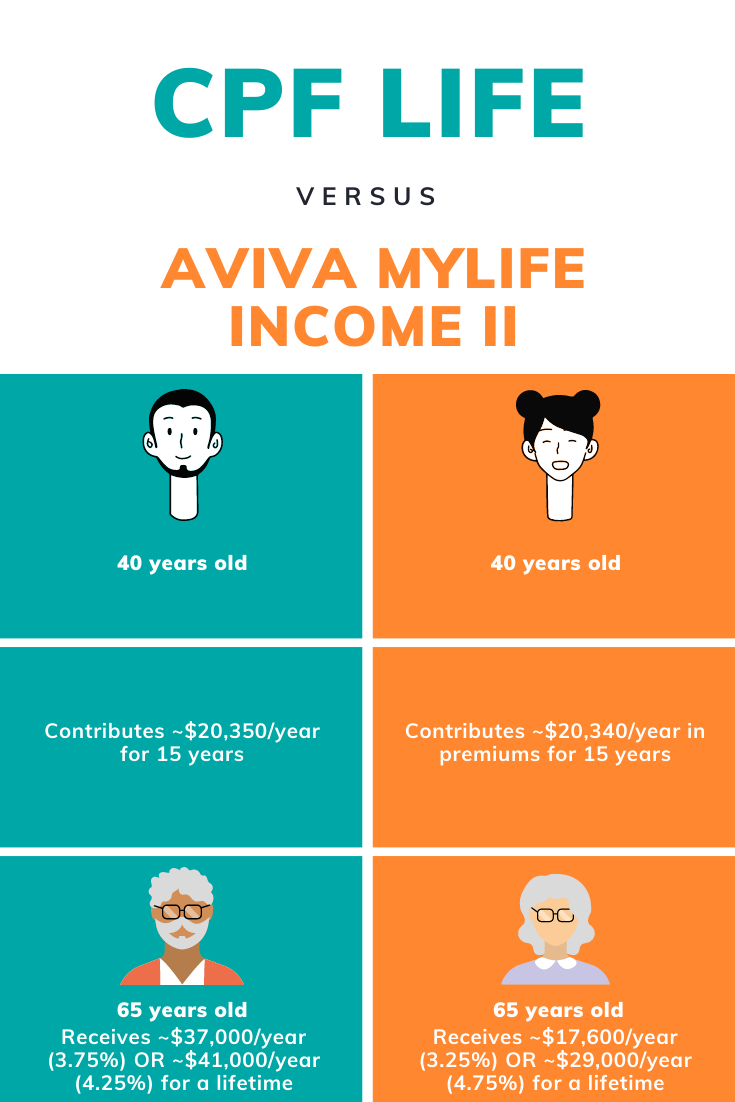

For the purpose of comparison, we use the example of a 40-year-old male, who will set aside $422,988 (estimated ERS amount 15 years later [1]) in his Retirement Sum account by the time he is 55.

To reach this amount, he contributes about $20,350 every year for 15 years into his CPF Special Account which grows at an average of 4.5% p.a. factoring in extra interest earned on the first $60,000.

Using the CPF LIFE Estimator on CPF’s website [2], it is estimated that he would receive around $37,000 a year assuming an interest rate of 3.75%, and around $41,000 assuming an interest rate of 4.25% from he is 65 years old.

Now let’s compare how these numbers will look like if the same person opts to receive his retirement income through Aviva MyLifeIncome II:

In this case, he would have to fork up $20,340 in premiums every year for 15 years, which would then accumulate over the years to pay out around $17,600 a year from age 65, assuming the par fund returns 3.25% p.a., and around $29,000 assuming the par fund returns 4.75% p.a. Of the yearly payout amount, only $4,350 is guaranteed.

Although there is a slight difference in premiums, we can clearly see that CPF LIFE gives a higher amount of payout for each dollar of premium and that the range is smaller for CPF’s projected payouts than that of the insurance plan.

This is because CPF monies are invested in Special Singapore Government Securities (SSGS) which are guaranteed by the Singapore government and have coupon rates that match the interest rates that CPF members receive (currently floored at 4%). With insurance plans, however, your monies are invested in mainly low-risk government and corporate bonds, and short-term liquid investments which do not guarantee a certain rate of return.

Insurance Benefits

Next, we take a closer look at some other benefits insurance plans provide compared to CPF LIFE using Aviva MyLifeIncome II as an example.

| Retirement Plan | Aviva MyLifeIncome II | CPF LIFE |

|---|---|---|

| Unique benefits/features | All future premiums are waived in event of Major Cancer diagnosis. Lump-sum cash payment of up to 5 times basic plan’s annual premium in the event of death, terminal illness, or total permanent disability. | Though not tied to CPF LIFE specifically, one can claim for insurance benefits through ElderShield/ CareShield Life in the event of loss of independence. |

Upon death, CPF LIFE will pay your beneficiaries any CPF LIFE premium balance not already paid out. This is because CPF LIFE is structured to draw down from the premiums you have paid to fund your payouts and is also how it is able to provide very competitive payout rates compared to the industry.

On the other hand, insurance retirement plans come with additional insurance coverage, ranging from premium waivers to additional guaranteed payouts upon death or loss of independence. For example, MyLifeIncome II provides you with monthly payouts while retaining your capital invested upon death.

Using the same illustration of the 40-year-old man above, the death benefit payout could be as high as $500,000, of which $320,000 is guaranteed, even after the plan has paid out the yearly retirement income for 25 years.

Some other interesting features of retirement income plans include retrenchment benefits. If the recent pandemic has made you anxious about job stability, a retirement plan like Manulife RetireReady Plus II pays you a lump sum benefit to help you tide through in the event you are retrenched.

Flexibility and Control

Lastly, let’s compare these retirement income plans with CPF LIFE in terms of flexibility and control.

| Retirement Plan | Aviva MyLifeIncome II | CPF LIFE |

|---|---|---|

| Premium Payment Term | Single Premium, 3, 5, 10, 15, 20 and 25 years. | Accumulates over time through monthly contributions from the day one starts working. At age 55, the retirement sum is set aside in your Retirement Account. The retirement sum is equivalent to a lump sum premium used to join CPF LIFE. Choice to top up “premiums” through Retirement Sum Topping-up (RSTU) Scheme. |

| Income Payout age | 0 to 20 years after premium payment term | 65, 66, 67, 68, 69, or 70 years old |

| Income Payout Period | Lifetime only | Lifetime only |

| Flexible Options | Option to withdraw yearly income and booster bonus or reinvest them with the insurer Aviva at the prevailing non-guaranteed interest rate. | Option to choose from Standard, Basic plan (lower payouts in exchange for higher premium balance) and Escalating plan (payouts that increase yearly to manage inflation). |

From the above information, one obvious benefit of Insurance retirement plans over CPF LIFE is that they give you the choice to receive payouts from an earlier age. MyLifeIncome II allows you to receive payouts as soon as we have finished paying our premiums, and some plans such as AXA Retire Happy Plus II start payouts from as early as age 50. In contrast, we can only receive payouts from 65 years old or later under CPF LIFE.

Besides, while we have full control of our payout age under an insurance retirement plan, our selected pay out age under CPF LIFE is not guaranteed in that it might be shifted based on changes in government policies.

Under CPF LIFE, we have choices on how payouts are received, such as allowing our payouts to increase over the years to adjust for inflation (Escalating plan), or choosing between higher payouts (Standard plan) or higher premium balances (Basic plan).

Nonetheless, in general, insurance retirement income plans are more flexible and give greater control over how we receive our income payouts.

Conclusion

In this article, we have seen that both insurance retirement income plans and CPF LIFE have their own advantages to help us reach our retirement goals. In evaluating whether to give up on CPF LIFE in favour of an insurance retirement plan, it is important to know the trade-offs in this decision. Are you willing to give up higher, stable returns in favour of capital preservation and flexibility?

For most of us planning for retirement, being able to get the highest guaranteed payouts for every dollar premium should be our topmost priority due to limited resources. After we have taken care of the basics, we can then start to think about capital preservation for our loved ones or the luxury of flexibility and control.

Perhaps the easiest way to look at this is to allow CPF LIFE to do exactly what it is meant to do, provide us with the best safe retirement income floor in the market, and then complement it with insurance retirement plans so that we can have the choice to achieve financial independence earlier.

[1] Assuming BRS grows at 3% p.a. and ERS is 3X of BRS.

[2] CPF LIFE Estimator: https://www.cpf.gov.sg/eSvc/Web/Schemes/LifeEstimator/GetLifeEstimatorResults