Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Financial planning insurance is about getting suitable risk protection according to your needs.

In November 2004, when I wrote in this column on why one should use term insurances instead of whole life plans, I never expected it to create such a great interest. Over the last 2 months, I received letters, emails, forum threads and phone calls expressing their opinions. Many advisers also wrote articles on the same topic to express their views. While some financial advisers wished Providend would somehow disappear from the face of this earth for rocking the boat, many clients, members of the public (from as far as the US) and people from the financial fraternity expressed their appreciation of our opinions. And since we were the ones who started the topic, I thought it would only be appropriate for us to clarify some misconceptions, which have surfaced as a result of our article.

Limited Resources, Unlimited Needs

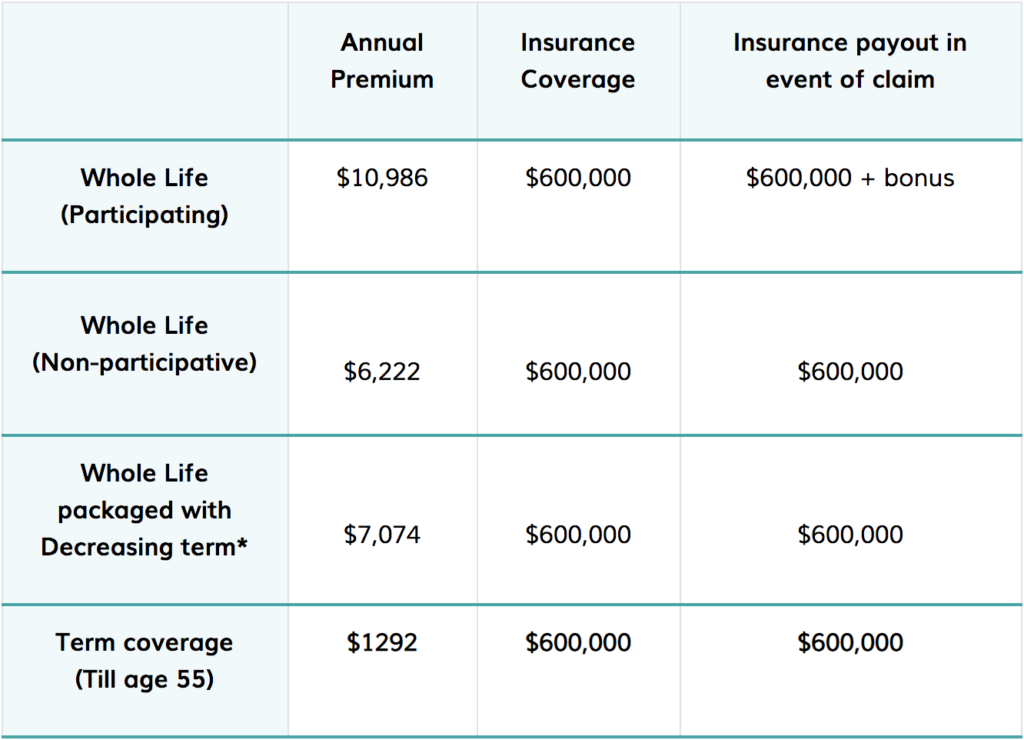

All of us have plenty of financial needs. Insurance for protection, investments for our retirement & kid’s education, paying our mortgages, car loans and so on. But our resources are limited. If you are a male aged 35 and need to provide your family with a monthly income of $3,000 for 20 years in the event of your unfortunate demise, you will need about 600,000 cover. If you intend to retire at age 55, Table 1 shows the comparison of the various types of plans.

The truth is, how many can afford to pay more than $6,000 or $10,000 per year, just to cover his individual death needs? In the above example, we haven’t even considered his medical, his spouse, and his children insurance needs yet. We can discuss all the merits of whole life with cash values and so on, but if we cannot even fully cover our needs, what’s the point?

TABLE 1: Types of insurance plans

About Temporary And Permanent Needs

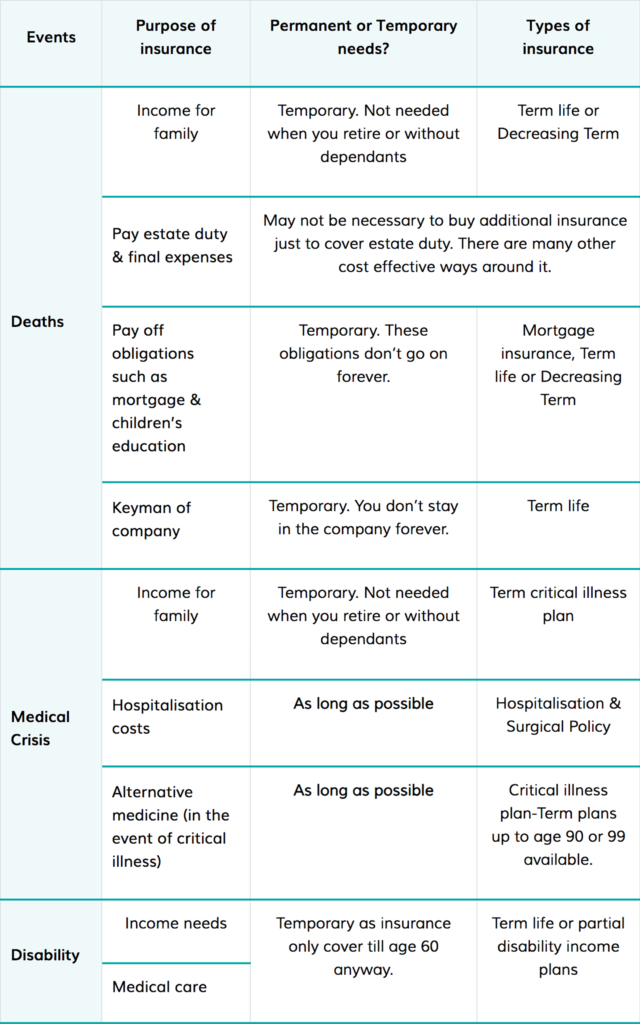

“But term plans are temporary. It will cease after a certain period. So when you need insurance most, you don’t have it” So say the proponents of whole life plans. Let’s look at some of the common protection needs and whether they are permanent or temporary (Table 2):

When one buys a non-par plan, is he buying it to protect a permanent need or temporary need?

From table 2, it becomes clear that most of our protection needs are temporary, except providing for hospitalisation costs and maybe say, alternative medicine. Insuring against high hospitalisation cost can be done effectively using a good hospitalisation & surgical plan that pays the first dollar that you incur. To provide for the need for alternative medicine in the event of a critical illness, you can buy a small term plan that covers critical illness till age 90 or 99.

About Level Premiums

In the letters to the BT from directors of 2 financial advisory companies after our article on term insurance was published, It was interesting to note that the both their understanding of premiums concerning whole life and term plans contradict each other.

TABLE 2: Permanent or temporary needs?

With term plans, we can afford to fully cover our needs. Use insurance for the right purpose, protection.

One said that when you buy whole life plans, there is this need for cash values because it acts as ‘excess’ premium required to keep the premium constant during the lifetime of the insured. The other however said that for term policies (though there are no cash values), it is also possible to keep premiums constant as there is pre-funding where the “excess” premiums are invested so that this reserve can be used to fund higher premiums in later years. Let me help clarify that it is not important to know how the insurance companies keep their premiums level, but rather for readers, it is enough to know that whether whole life (par or non-par) or term policies, premiums are kept constant during the period of cover.

About Whole-life (Non-Par) Plans

Whole life (non-par) plans, like term plans, are insurance that gives you a fixed cover of say, $600,000 (without bonus) for your period of cover. However, if you surrender the policy at a certain point in time, you get back your premiums plus certain guaranteed returns. Of course, nothing is for free; the premiums are a lot higher than term plans (see table 1).

Although it is tempting to get something back if we surrender a policy, buying it for this purpose commit 2 fundamental errors that we have discussed:

- You may never be able to cover your whole family with that kind of premiums. Even if you can, you leave very little for your other financial needs.

- If most of your needs are temporary, why commit to whole life?

There is also something ironic about non-par plans. When one buys such a plan, is he buying it to protect a permanent need or temporary need? If he has been convinced that he has a permanent need, and will not surrender the plan, when he makes a claim, he loses all cash values and only gets the fixed cover. So he pays more but gets the same benefits as term plans. However, if his needs are temporary and he intends to surrender it at some point in time, why did he pay so much for a whole life plan in the first place, when he can get the same cover at lower cost by using a term plan? The very reason why you bought an insurance plan becomes the reason that disadvantages you. Ironic? I think so too.

About Insurance Being A Low-Risk Instrument For Investing

Most insurance companies use 5.25% as the projected returns; it is also stated in the benefit illustration of whole life plans that the projected yield could be 6.75%. As such, insurance companies may take a much higher risk to achieve the returns for policyholders. However, after deducting for distribution cost, the actual return, depending on when you surrender the policy, can be as low as 1% p.a or an average of 3-4% p.a. The low return may give the perception that it is a low-risk vehicle where in fact it is caused by the cost of distribution.

In the past, portions of the cash values come with a certain guarantee, as it is regulatory requirements to do so. However, with the ushering in of the new risk-based capital regime, this requirement has been cancelled. What this means is that we may increasingly see traditional plans with no guaranteed cash values, which will put it in equal footing with all investment instruments.

People should know that the advantage of insurance lies not in the returns but in the protection it gives for a relatively small premium. It is encouraging to see that the insurance companies that Providend represents are continuously developing excellent term plans for our clients. Companies such as Asia Life, HSBC, NTUC & UOB have excellent term life. AXA, Manulife has got one of the best hospitalisation plans in Singapore. This signals their belief in being an institution that truly wants to care for the protection needs of their policyholders.

The last 2 months have not been easy for us as we sing a different tune and receive all sorts of unkind comments. But as long as readers get the financial education that is so badly needed, and as long as we can help you consider these issues before you buy your next insurance, we will continue to toil on.

The edited copy appeared in The Business Times in January 2005. The spirit and principle of the article remain relevant although some products are no longer available. Please seek our advice if you are interested in certain products.

If you need more information about insurance plans, feel free to reach out to friendly Client Advisers here.

Announcement: With effect from 1 June 2022, MoneyOwl is a 100% NTUC Enterprise (NE)-owned company.