Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Weigh the pros and cons of “SA Shielding” to see if it’s the right strategy for your retirement planning.

If you are a CPF member who will be turning 55 years old, you may have heard your friends or your financial adviser speaking to you about SA Shielding. It could have left you with doubts about the legitimacy of such a manoeuvre, the benefits of doing so, and most importantly whether you will lose out by not shielding your Special Account.

What is SA Shielding?

This is a process which “shields” your Special Account savings from being transferred to your Retirement Account when you turn 55 years old to form your retirement sum. To appreciate this process, let me first explain what happens to your CPF accounts the second you turn 55 years old.

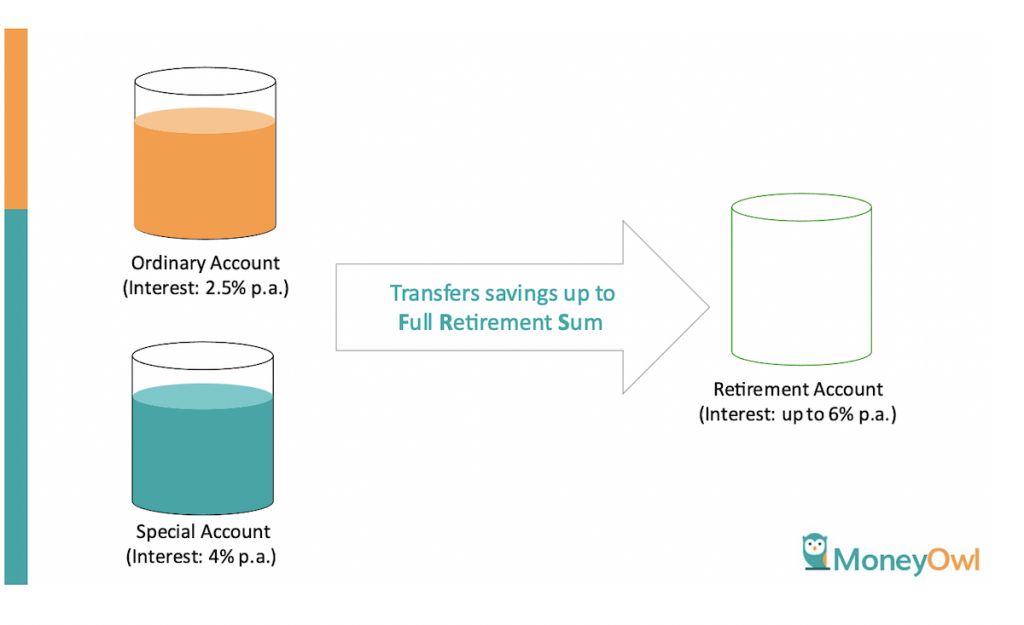

Prior to turning 55, you have three CPF Accounts, i.e. Ordinary, Special, and MediSave. Upon turning 55, CPF Board will create a fourth account called the Retirement Account, which will be used to set aside a retirement sum. This retirement sum will be used to join CPF LIFE, which will give you a stream of stable lifelong income from age 65. This retirement sum is formed by taking savings from your Special and Ordinary Account.

Which account would you like to use to make up your retirement sum in the Retirement Account? Perhaps you may have chosen Ordinary Account because this process would have easily helped you earned up to 3.5% p.a. more interest on your savings. Or perhaps you may have said it doesn’t matter if you are not sensitive to the interests earned on your savings. After all, the focus is on making sure you have set aside a sufficient sum of money for your CPF LIFE payouts.

By default, CPF Board will transfer the savings from your Special Account first to your Retirement Account because savings in your Special Account were designed specifically to help you save for retirement. The amount transferred is up to the Full Retirement Sum (FRS) of your cohort, which is estimated to provide you with a CPF LIFE payout sufficient for basic expenses. If you are turning 55 this year, the FRS is $186,000. If there are insufficient balances in your Special Account, balances from your Ordinary Account will be transferred as well.

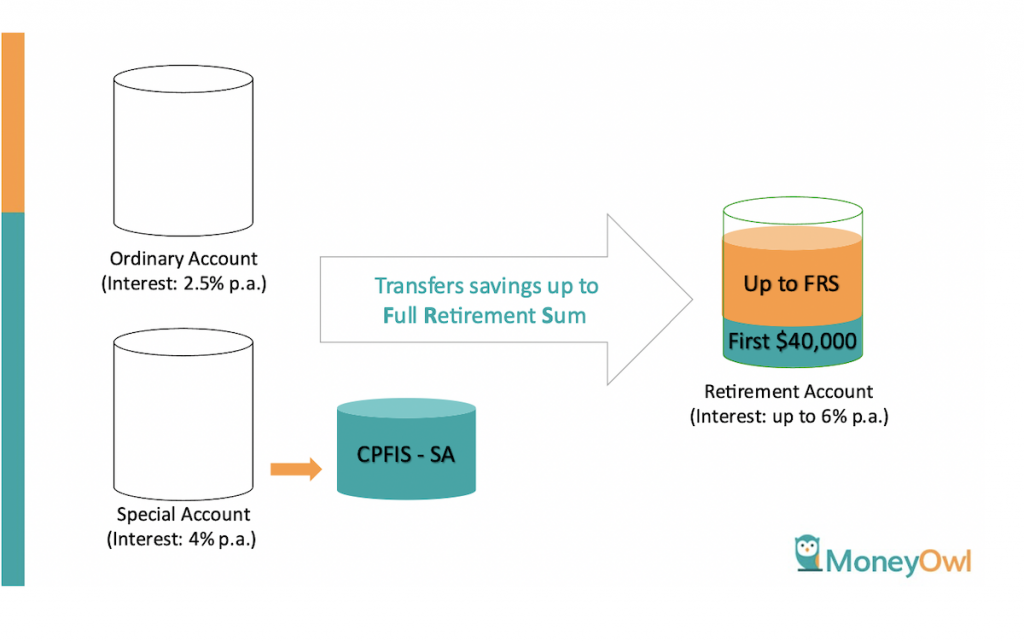

Over the last five years or so, a few savvy individuals have found a way to circumvent this process by using one of the existing CPF schemes. Under the CPF Investment Scheme, you can invest both your Ordinary and Special Account savings except for the first $20,000 in your Ordinary Account and the first $40,000 in your Special Account. CPF savings that are invested will not be transferred to your Retirement Account. In other words, if you invested your Special Account savings above the first $40,000, those savings will not be transferred to the Retirement Account. As $40,000 is insufficient to make the FRS, CPF Board will then pull the balances from your Ordinary Account instead. Voila!

Benefit of SA Shielding

Through this, you have increased the effective interest earned on your combined CPF savings. But that’s not all. When you subsequently liquidate your CPF investments, the savings will be returned to your Special Account. As you have already satisfied the FRS, these savings in your Special Account can be withdrawn anytime, whilst earning the 4% p.a. interest, thus creating your very own high-interest savings account.

For even more enterprising clients, they can also consider doing both an Ordinary and Special Account Shield by investing all their CPF savings above the respective limits. As the remaining Ordinary and Special Account savings would be insufficient to meet the FRS, they can also use cash that is sitting idle in the bank to top up their Retirement Account, effectively earning high risk-free interest on their cash savings.

As you can see, SA Shielding is legitimate as it uses existing CPF schemes to achieve an outcome that while slightly different from the default, nonetheless satisfies the policy intent of ensuring that you have sufficient retirement income through CPF LIFE while optimising your savings. However, as with all things, there is always the danger of misusing such hacks, which you will need to watch out for.

What to watch out for

As you will need to invest your Special Account savings, there is a potential danger of mis-selling. You may be recommended an expensive or higher-risk investment instrument without understanding the risks or costs involved in them. This could lead to potential investment losses that outweigh the benefit of SA Shielding. Our recommendation is to either invest in short-term Singapore treasury bills or government bonds through your bank or invest in a short-term bond fund such as Nikko AM Shenton Short Term Bond Fund. The choice should be focused on low costs and safety rather than returns as the intent is to return the savings to your Special Account within a month or two.

In conclusion, SA Shielding can be used to help you optimise your CPF savings to earn higher returns on your cash or CPF. While it’s great to reach for higher returns, don’t forget that ultimately CPF is meant to provide you with a steady stream of income during retirement so make sure your end outcome is having enough in your RA for your CPF LIFE payouts.

For greater clarity, speak to our client advisers who are well versed in national schemes like CPF to understand SA Shielding better and whether it is right for you.

MoneyOwl is on Telegram! Join us for awesome content on investments, insurance and financial planning.