Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

The story of three workers and how they represent the role of different assets classes in our investment portfolio.

Imagine a company that has three employees.

The first employee, Stuart, is your typical go-getter, strategic and smart. He is always ahead of the curve in innovation and brings a lot of value to your company, driving growth and delivering outcomes. However, Stuart is prone to periods of emotional highs and lows, and during episodes when he lacks motivation or inspiration, he may not turn up in the office at all. Nevertheless, over the years, Stuart has delivered a lot of positive value to the company.

The second employee, Bob, is your typical dedicated, loyal staffer. You can always count on him to get the job done, rain or shine, delivering consistent value to the team. When Stuart isn’t performing, Bob is usually there to keep operations running. However, Bob’s focus is on doing a good job, giving you exactly what he promises to give you, nothing more, nothing less.

The third employee, Gerald, is the office flower. He is your typical good looker, dresses immaculately, speaks eloquently, and almost always gets the attention of the office ladies. However, Gerald does absolutely no work at all, his only contribution appears to be shuffling papers across the table, preening in front of the mirror, and turning up for work every single day.

Lately, you noticed that Stuart’s mood swings have become even more rampant and this has been causing you some unease. He had even stormed out of a meeting room while everyone was still discussing work and didn’t come back to the office for several days. Bob, due to a family crisis at home, had to take leave from work for an extended period. Though he did assure you that he will still try to cover the bases, you told him to focus on his family instead. So that leaves you with piles of work to be done and only one employee who is still turning up in the office every day.

You decide to reallocate some of the work to Gerald as you are concerned with Stuart’s emotional outburst and Bob’s extended absence. Gerald looks up at you in shock. You usually don’t give him any work to do and he is suddenly very aware that he is the only one in office. In fact, your business partners and customers are curious about the sudden mention of Gerald in every email correspondence. News has also spread that he is quite the charmer creating unprecedented levels of hype. It even appears that business is booming with all the traffic.

However, while you are benefiting from having Gerald be the accidental face of your company, you wonder when he is going to submit the business proposal you’ve asked him to work on two weeks ago.

I wonder how many of you might relate to the story above in your day-to-day work environment. I’m sure we all have our fair share. But this story isn’t about our colleagues and how to deal with them, it is an analogy describing the role of the different asset classes in our investment portfolio.

At this point, you would probably have guessed that Stuart represents the role of stocks in your portfolio. It drives the growth of your portfolio but does forgive its tendency for short-term volatility. Bob represents the role of bonds in your portfolio. It is primarily meant to provide stability and to a lesser extent growth. Now, what then does Gerald represent? You might even wonder why you need a Gerald in your portfolio?

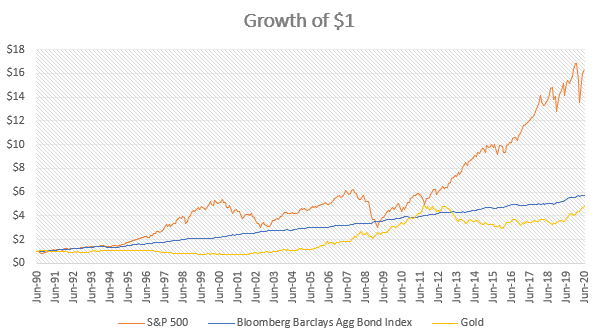

Gerald represents gold. Gold, as a precious metal, has traditionally been associated with all things that glitter and is highly prized for its intrinsic value as a statement of wealth or in fashion. However, like Gerald, gold as an asset class does not produce any growth. Yet, in recent headlines, we are seeing gold prices trading at an all-time high of more than US$2,000 per ounce.

What is driving the upward in prices, is not because gold is suddenly producing value, it is mainly because investors are drawn to it as a hedge against the volatility in the stock markets (Stuart on one of his mood swings). This is coupled with bonds yields which are currently deflated to all-time lows due to central bank actions of injecting liquidity to stabilise the financial markets in this post-COVID world (Bob dealing with a family crisis at home). Investors suddenly feel that the non-income producing gold actually looks relatively more attractive (Gerald looking up from his workstation, saying, ‘Who me?’).

Because many people think that the US Federal Reserve will continue to keep interest rates low while the US government wants inflation to happen via multiple stimulus packages, real bond yields will remain negative for a long time to come. This creates speculative interest in gold as a better asset as an equity hedge compared to bonds.

Whether this will come to pass, nobody knows. What we do know is that based on history, gold has had a patchier negative correlation with stocks, than bonds. And while you may be attracted by the 33% year-to-date growth in gold prices, don’t forget that gold has also seen extended periods of non-performance, i.e. -1.4% p.a. between 2013 and 2019, and 0.8% p.a. between 1991 and 2005.

Now, if you were the owner of the company, how would you allocate your HR budget across your three employees?

================

To learn more about why MoneyOwl does not have gold exposure in our portfolio, read our letter from our CIO.

This article is written by MoneyOwl’s Solutions Team.