Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

What is SRS?

The SRS – or Supplementary Retirement Scheme – complements the CPF so that we can save more for our retirement.

The SRS is voluntary but offers tax benefits. There is a yearly contribution cap of $15,300 for Singapore citizens and Permanent Residents, while the maximum foreigners can contribute annually is $35,700. These contributions are eligible for tax relief.

After you set up your SRS account with one of the three local banks, you can invest your SRS savings to get potentially higher returns.

The investment returns are accumulated tax-free, and only 50% of withdrawals from SRS are taxable at retirement and you can spread out your withdrawals over 10 years.

What can I use my SRS money for?

You can invest your SRS savings in a wide range of financial instruments such as unit trusts, insurance, fixed deposits (FDs), stocks, Singapore Saving Bonds and so on, to grow your retirement savings. However, leaving your contributions as cash in the SRS will earn only 0.05% each year.

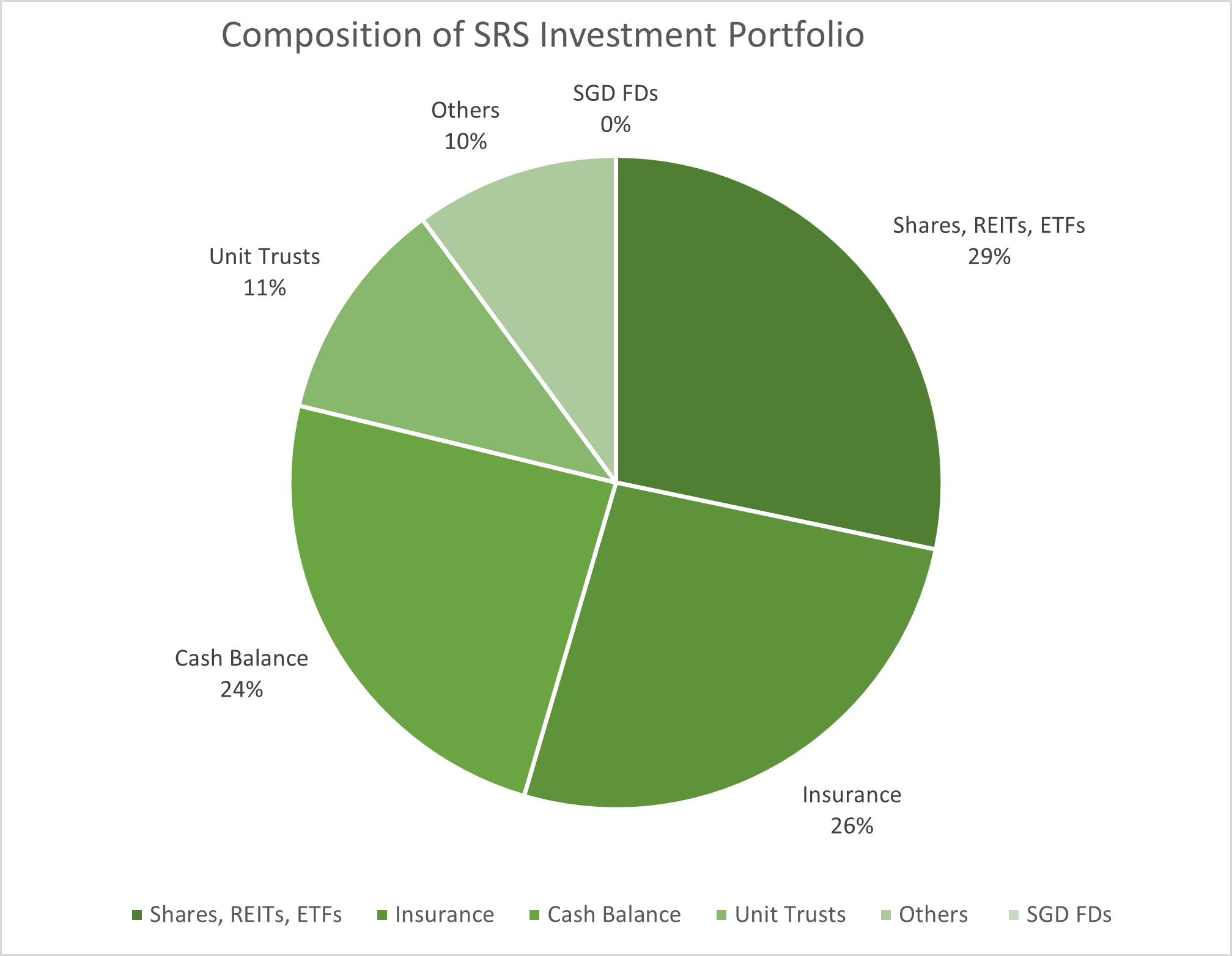

According to statistics from the Ministry of Finance, as of the end of 2021, SRS contributions were invested in the following products:

A caveat is that the DFA Equity Portfolio may not suit everyone. By going through MoneyOwl’s online investment journey, you get to assess your investment horizon, risk ability and willingness to take risks. A suitable portfolio that best fits will then be recommended to you based on your input. Alternatively, speak to our client advisers who will help you understand the investment solutions available, and get your risk profile done to have a suitable portfolio matched to your needs.

What happens if I withdraw my SRS earlier?

You can withdraw from the SRS before the statutory retirement age, but the total amount withdrawn will be subject to tax. In addition, a 5% penalty will be imposed unless it is made under exceptional circumstances such as death or on medical grounds.

How do I know if I am suitable to contribute to SRS?

You can consider contributing to your SRS if you wish to save over and above your CPF for your retirement and if you wish to lower your taxes.

As SRS is meant to supplement your CPF savings, you can consider topping up your CPF first. The CPF Special Account pays risk-free interest of up to 5% and you can also enjoy tax relief. The CPF top-up limit for tax relief is $192,000. However, unlike for SRS where you can withdraw subject to a penalty, CPF top-up monies cannot be withdrawn in a lump sum, but will instead be paid out as higher monthly payouts from age 65.

Another consideration is when you can start to withdraw your SRS savings. The age when you can start to withdraw your SRS savings, is the statutory retirement age at the point when you make your first SRS contribution. The current retirement age is 63, but the Government intends to raise it to 65 by 2030. So if you intend to save through the SRS and want to have the option to start withdrawing as early as possible, you can consider making your first SRS contribution now, before the retirement age is raised further.

Disclaimer:

Additional Notes to Illustration

Total invested considers the amount of initial investment as well as the total monthly investments over your selected investment period. Total gain refers to the difference between the combined amount of payouts received and portfolio value, and total amount invested over your selected investment period. Total invested considers the amount of initial investment as well as the total monthly investments over your selected investment period.

It is assumed that the DFA Equity Portfolio grows at a constant rate of 6.7% p.a. Returns are projected long-term returns using average 20-year rolling returns (rolled monthly) of comparative indices from 1994 to 2020. Returns are net of fund level fees (0.25% p.a. to 0.27% p.a.) and net of advisory fees (assumed 0.60% p.a.). It is assumed that re-balancing is performed half yearly. This graph is only for illustration purposes, and does not represent actual investor performance. All investments carry risk. Actual performance will vary due to changes in market conditions, differences in fees and actual portfolio rebalancing. Past performance is not indicative of future performance.

While every reasonable care is taken to ensure the accuracy of the information provided, no responsibility can be accepted for any loss or inconvenience caused by any error or omission. The information and opinions expressed herein are made in good faith and are based on sources believed to be reliable but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. The author and publisher shall have no liability for any loss or expense whatsoever relating to investment decisions made by the reader.