Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Your SRS funds can be used to create a passive income stream for retirement planning. Use this 3-step selection to decide where to use your funds.

This article is a continuation of our earlier piece on how to save on taxes using SRS.

Funds in the Supplementary Retirement Scheme (SRS) can be invested into a wide range of instruments such as shares, unit trusts, insurance, bonds and fixed deposits. Or you can simply leave your SRS monies in cash, which is not a wise financial decision due to the current low-interest rates of 0.05% offered by the banks.

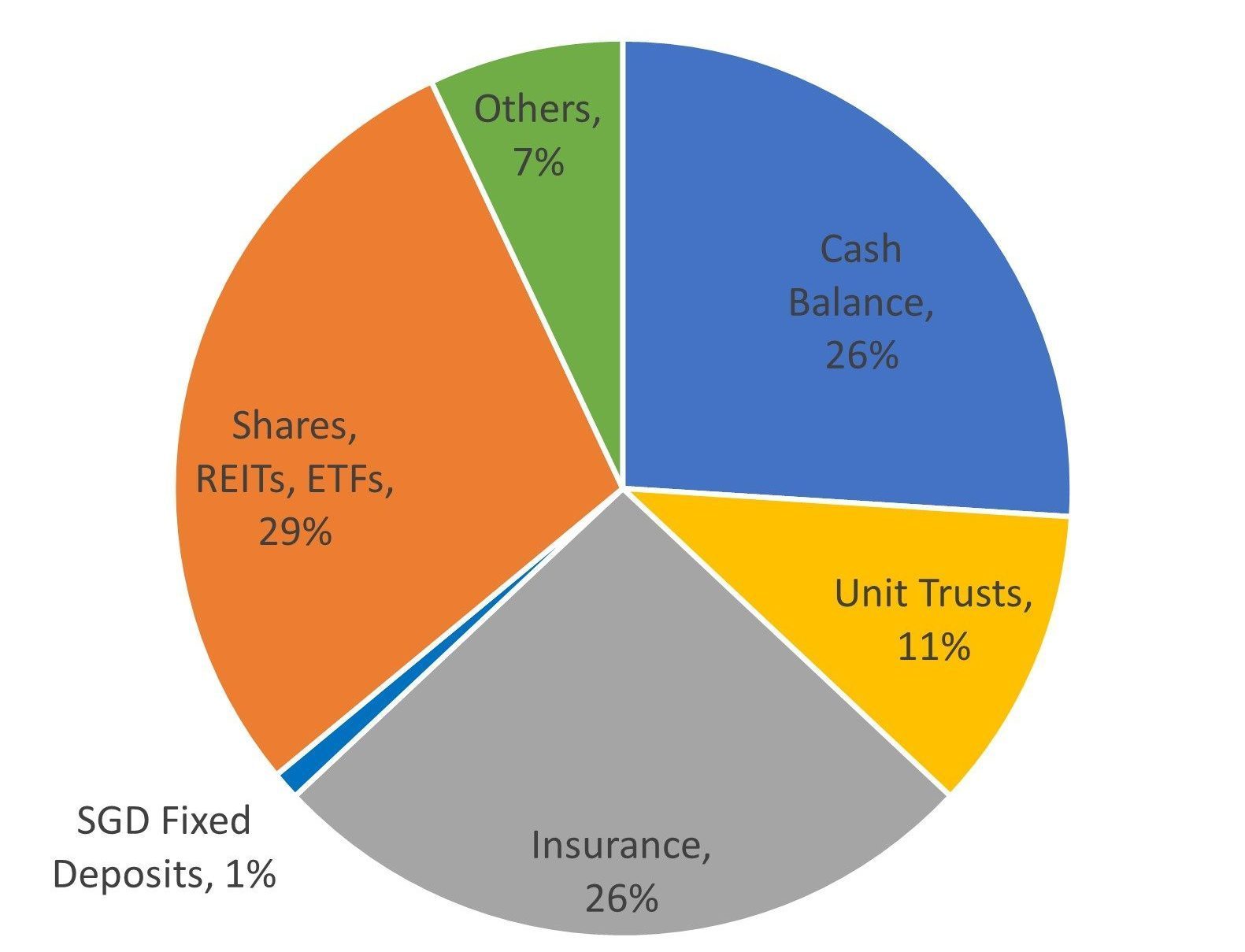

What Do People Do With Their SRS Funds?

*Source: Ministry of Finance (MOF)

On top of enjoying tax savings with SRS, it is important to look at how you can grow your SRS funds. As of December 2020 data from the Ministry of Finance (MOF), 26% of SRS funds stays as cash, a drop of 4% from the year before. It is good news that more people are learning to optimise their SRS savings, as should you. Since you are likely to only withdraw your SRS after retirement age to avoid penalties, you should make your SRS funds work harder since you have the benefit of time

The Power of Compounding

Illustrating using a table below, we project the amount of SRS you will have at age 62 assuming you have $30,000 in SRS and have 25 more years before reaching age 62. Depending on the returns you receive (Eg. 0.05%, 2% or 4% per annum), the projected amount which you can get at age 62 is vastly different.

| Product A | Product B | Product C | |

|---|---|---|---|

| Lump sum | $30,000 | $30,000 | $30,000 |

| No. of years before reaching age 62 | 25 years | 25 years | 25 years |

| Interest P.A / Return | 0.05% | 2.0% | 4.0% |

| Projected amount after 25 years | $30,377 | $49,218 | $79,975 |

| Gain % | 1.26% | 64.06% | 166.58% |

If $30,000 of SRS is left in cash and assuming an interest of 0.05% p.a., you can expect your SRS funds to grow to only about $30,377 after 25 years. But if you can obtain a higher rate of return of 4%, the end result will be around $80,000. Of course, these returns are not guaranteed. However, some insurance products do provide some form of guarantee on their projection.

Whilst you can invest your SRS in various instruments, the focus of this article is on SRS-approved insurance policies and how you can use them to build up your retirement nest egg.

Using SRS To Generate Income Stream For Retirement

When you have stopped working and are in retirement, how would you fund your living expenses?

For many people, it could be either:

- Withdrawing from your bank account. This can cause undue worry when you notice how your bank balance decreases with each withdrawal. The current low-interest-rate environment does not help to counter the increases in the cost of living either.

- Cashing out from your investments e.g. shares, to fund your living expenses. This can be worrying especially during a market downturn. Your investment value may have suffered a significant loss and any cashing out further will shrink your investment holdings further.

- Receiving a stream of income payout from investment instruments. Examples like dividends, rental income and insurance-based retirement income products.

[Note: You should probably use all of the 3 components above in an integrated and balanced approach for retirement planning. In this article, we focus on the importance of a recurring income payout which, in my opinion, is understated in retirement planning.]

During retirement, having a stream of income (“pay-check”) is ideal as it helps to fund our retirement lifestyle. Most Singaporeans would have their CPF LIFE as their first layer of recurring income. CPF LIFE is a good scheme which people should maximise first. However, if CPF Life is not sufficient for you, you can increase your stream of income payout further with retirement income products.

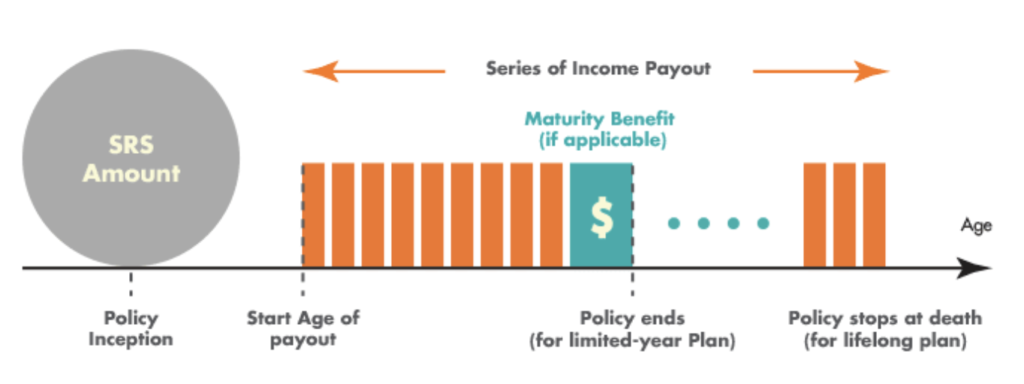

How Do Retirement-Income Products Work?

You first commit a lump-sum amount. At a specified age (e.g. age 62), the policy will pay a series of income payout either for a fixed number of years (e.g. 10 or 15 years) or for life. For some plans, there is an additional payout when the policy ends (at maturity).

There are many SRS-approved insurance products in the market and it can be confusing. Every product has different features and you are more likely to have more questions than answers about them.

At MoneyOwl, we understand your concerns. And we make things easier for you. The following is a 3-step guide to help you select a suitable retirement income product that meets your needs.

3-Step Selection Guide

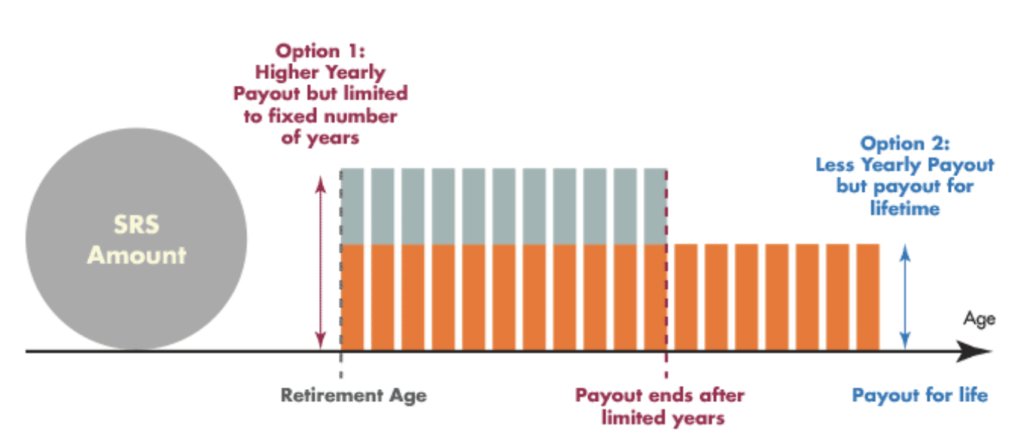

Step 1: Do you need an income stream that pays for life or only for limited years?

Lifelong income takes away the fear of outliving your assets. Naturally, a plan that pays lifelong income would cost more than one than pays only for a fixed number of years.

With the same SRS amount, the shorter the payout duration (e.g. for 10 or 15 years), the higher is the yearly payout. Generally, if you plan to have multiple sources of lifelong retirement income such as dividends and rental income, you may not need to be too concerned with getting another policy for an additional lifelong income. A plan which pays for a fixed number of years and with a higher recurring payout may suffice.

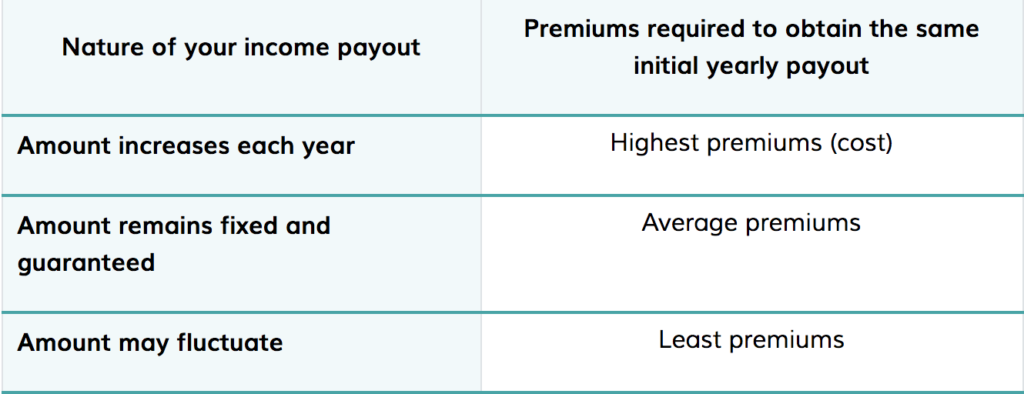

Step 2: Do you require your recurring income amount to be fixed (guaranteed), variable (fluctuating), or increasing?

Generally, if you like your income payout to increase every year to combat inflation, there is a higher cost (greater premiums). On the other hand, it will cost lesser if you prefer your income payout to remain the same (fixed amount). The premiums (cost) may be even lesser if you do not mind that your payout fluctuates, i.e. your payout is lower if the insurer doesn’t do so well (although there is some guaranteed portion).

Besides, there are further considerations that are a bit trickier for you to consider such as your risk tolerance, the size of your retirement goal relative to your resources, and your other sources of retirement income. Since your SRS funds are usually a small component of your overall nest egg, a quick way is to consider based on your preference on the nature of income payout.

Step 3: Compare the Products

Hopefully, with Steps 1 & 2, you have a better understanding of the features you are looking for. Now is the time to look for suitable products. You may wish to find out more about some SRS-approved Single Premium Retirement Income plans here.

Please contact us at enquiries@moneyowl.com.sg if you have any questions, our Client Advisers will compare and recommend the best SRS-approved retirement plan that fits your needs.

This article was first published in December 2018 and was updated in October 2021.